Over the last couple of days, I’ve focused my attention in this space on stocks in the Beverages industry of the Consumer Staples sector as defensive-oriented stocks that smart investors might want to think about working with under current market conditions. Volatility has been the word of the past month or so, with the market swinging between highs and lows quickly, sometimes in just a single day on nothing more than a single tweet or rumor about trade. To me, that volatility is an indication of the precarious state the market is in, as investors try to find any kind of useful foothold to indicate whether the economy in the U.S. will continue to grow.

Trade isn’t the only issue the market has to deal with right now, of course, but when you consider all of the different elements contributing to the market’s volatility right now, I think it makes sense to start thinking about ways to make your portfolio more conservative. Stocks in the Consumer Staples sector are generally a good way to do that, even if the stocks you’re thinking about working with don’t necessarily translate to a good value. The caveat, I believe is that those stocks have to also carry a significant level of strength in their fundamental profile. That is a critical piece of the puzzle, because without solid fundamentals, a stock trading at or near historical lows is probably just a cheap stock, with little in the way of a substantive reason to suggest it should be higher.

Cal-Main Foods, Inc. (CALM) is an interesting example that by most considerations should look attractive right now as a bargain-priced investment. The stock is down almost -15% in just the last couple of weeks since its last earnings report, and about – 22% from the 52-week high it last reached in November of last year. From a strictly value-based evaluation perspective, that means the stock is trading at a major discount to its historical value metrics; but really important piece of the puzzle is the fundamental data that the last earnings report made clear. This is a stock in an industry, Food Products, and sector that I think is a good place to focus on right now, but that is showing some troubling signs of deteriorating fundamentals that means this is a stock to be very careful about working with. Let’s look at why.

Fundamental and Value Profile

Cal-Maine Foods, Inc. is a producer and marketer of shell eggs in the United States. The Company operates through the segment of production, grading, packaging, marketing and distribution of shell eggs. It offers shell eggs, including specialty and non-specialty eggs. It classifies cage free, organic and brown eggs as specialty products. It classifies all other shell eggs as non-specialty products. The Company markets its specialty shell eggs under the brands, including Egg-Land’s Best, Land O’ Lakes, Farmhouse and 4-Grain. The Company, through Egg-Land’s Best, Inc. (EB), produces, markets and distributes Egg-Land’s Best and Land O’ Lakes branded eggs. It markets cage-free eggs under its Farmhouse brand and distributes them throughout southeast and southwest regions of the United States. It markets organic, wholesome, cage-free, vegetarian and omega-3 eggs under its 4-Grain brand. It also produces, markets and distributes private label specialty shell eggs to customers. CALM has a current market cap of about $1.9 billion.

Earnings and Sales Growth: Over the last twelve months, earnings declined significantly, by more than -438%, while revenues dropped by a little more than -29%. The picture isn’t really better in the last quarter, as earnings dropped by -114% while sales decreased by nearly -14%. The company’s margin profile is a major red flag and reflecting the deterioration I referred to, with Net Income as a percentage of Revenues in the last quarter at -18.9% versus -0.3% over the last twelve months.

Free Cash Flow: CALM’s free cash flow is negative, at -$46.37 million. That confirms the troubling signs from the stock’s Net Income; a year ago, Free Cash Flow was healthy, at almost $222 million.

Debt to Equity: CALM’s debt to equity is .0, which in this case doesn’t mean CALM has no debt, only that it is so small that it’s easier to leave the ratio at zero. Long-term debt was just $1.42 million in the last quarter, versus $236.09 million in cash and liquid assets. CALM has plenty of liquidity, but its declining operating profile means that it is also burning cash; at the beginning of 2019, their balance sheet showed $341.85 million in cash.

Dividend: CALM’s annual divided is $.85 per share, which translates to a yield of a little over 2.2% at the stock’s current price. For now, the company is being forced to draw from cash to maintain its dividend, which could call the safety of that dividend into question.

Price/Book Ratio: CALM’s Book Value is $19.38, which marks a decline from $20.70 at the beginning of the year. That means that the stock’s Price/Book ratio is 2.02 versus their historical Price/Book ratio of 2.55, which suggests that the stock is undervalued by about about 26.3% right now.

Technical Profile

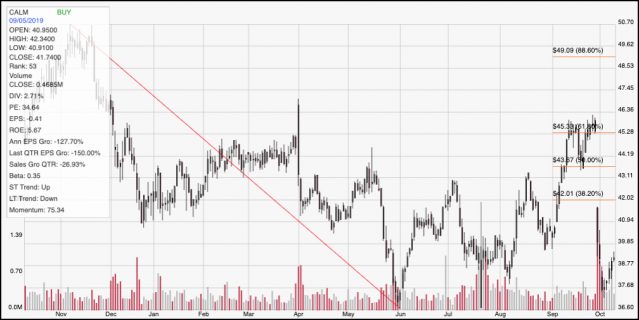

Here’s a look at the stock’s latest technical chart.

Current Price Action/Trends and Pivots: The diagonal red line traces the stock’s downward trend from November 2018 to June of this year, and provides the reference for calculating the Fibonacci retracement levels indicated by the horizontal red lines on the right side of the chart. The stock began to develop a nice upward trend in June on the back of a value profile that at the time was also backed by a generally favorable set of fundamental metrics; that puts the stock’s decline since late September into even sharper relief, as the market punished the stock severely following its earnings report. The stock finally found support not far from its 52-week and trend low point at around $36.50. Near-term resistance is around $40, with $42 as shown by the 38.2% Fibonacci retracement line acting as a secondary level beyond that point. If the stock breaks below its current support at around $36.50, its next support is probably around $34 based on lows last seen at the beginning of 2015; beyond that, it could drop even more, to levels around $24 or $25 not seen since mid-2013.

Near-term Keys: The stock’s momentum is sharply bearish right now, with little basis to give investors a reason to bet on long-term strength in this stock. Even if you’re willing to be aggressive, using call options to bet on a short-term bounce to anywhere near the $42 level is sheer speculation, with a high likelihood of failure. If the stock drops below $36.50, take as a sign to short the stock or to work with put options, with a target in the near-term at around $34, but keeping an eye on even more downside beyond that point if the market keeps beating the stock lower from that point.