Most of us are certainly getting tired of continuing to hear and read about COVID-19. Daily statistics about infections, mortality rates, and rolling averages of both can really wear on even the most patient person. The truth, of course is that this isn’t something that is going to go away – not as long as infections continue to spread throughout the U.S. and almost certainly not until vaccines and practical anti-viral treatments have been made widely available, on a global scale.

That reality is why news over the weekend that the U.S. government had signed a $2.1 billion agreement with two European pharmaceutical companies, British GlaxoSmithKline PLC (GSK) and French Sanofi to accelerate development and manufacturing of a recombinant protein-based vaccine candidate being produced by a partnership between the two companies. The vaccine is expected to begin move into Phase 2 trials next month, and the agreement calls for delivery (upon accelerated, expected FDA approval under the government’s Operation Warp Speed) of 100 million doses, with a long-term option for up to 500 million doses.

For GSK, the agreement is interesting, and certainly helps to call attention to their efforts to help combat the spread of the virus on a global basis; but the truth is that the deal will probably have a limited benefit to the company’s bottom line. GSK’s statement makes it clear the company is not expecting to profit from any COVID-19 vaccine as long as the pandemic persists; in fact, any short-term profit they may realize is planned to be invested in further coronavirus-related research and long-term pandemic preparedness.

From my perspective as a value-oriented investor, the announcement is most useful simply because it gave me a reason to take a deeper look into GSK’s fundamental and value profile. This is a company with a broad, global product portfolio, with a number of over-the-counter brands that you and I are likely to recognize during a typical run through the grocery store. That means that, pandemic aside, the company is already well-positioned to benefit in the broadest sense from increased public awareness about health in general. In fact, the numbers reported by management during the pandemic have been encouraging; while it isn’t surprising that recessionary global conditions have led to declines in revenues, other important measurements, including Free Cash Flow and Net Income, have improved, pointing to a management team that is putting a lot of attention on managing costs and maximizing operations. The stock price has generally underperformed after surging initially from a bear market low in March to about $43 in April, having generally moved sideways from that point. That actually sets up an interesting opportunity to think about a company with a healthy balance sheet and a nice value proposition.

Fundamental and Value Profile

GlaxoSmithKline PLC is a global healthcare company. The Company operates through two segments: Pharmaceuticals and Vaccines. The Company focuses on its research across six areas: Respiratory diseases, human immunodeficiency virus (HIV)/infectious diseases, Vaccines, Immuno-inflammation, Oncology and Rare diseases. The Company makes a range of prescription medicines and vaccines products. The Pharmaceuticals business discovers, develops and commercializes medicines to treat a range of acute and chronic diseases. The Vaccines business provides vaccines for people of all ages from babies and adolescents to adults and older people. It has a portfolio of medicines in respiratory and HIV. Its Pharmaceuticals business includes Respiratory, HIV, Specialty products, and Classic and Established products. Its Vaccines business has a portfolio of over 40 pediatric, adolescent, adult, older people and travel vaccines. GSK has a current market cap of $104 billion.

Earnings and Sales Growth: Over the last twelve months, earnings declined by nearly -38.5%, while sales dropped -5.76%. In the last quarter, earnings dropped -50.5% while Revenues decreased almost -18.75%. GSK’s Net Income versus Revenue, which was already healthy, has actually improved despite the negative earnings and revenue pattern; over the last twelve months, Net Income was 19.03% of Revenues and strengthened in the last quarter to nearly 30%. That is a strong sign of the company’s focus on profitability and efficiency that earnings alone doesn’t demonstrate.

Free Cash Flow: GSK’s Free Cash Flow remains healthy, at a little more than $10.77 billion. This does mark a useful increase from the last quarter, when Free Cash Flow was $9.1 billion, and translates to a Free Cash Flow Yield of 10.66%.

Debt to Equity: GSK has a debt/equity ratio of 1.27, which is generally high, but also not unusual for companies in the Pharmaceutical industry.. Their balance sheet shows a little over $8.2 billion in cash and liquid assets against $25.7 billion in long-term debt. Servicing their debt is not a concern.

Dividend: GSK pays an annual dividend of $2.50 per share, which at its current price translates to an impressive yield of 6.2%.

Price/Book Ratio: there are a lot of ways to measure how much a stock should be worth; but I like to work with a combination of Price/Book and Price/Cash Flow analysis. Together, these measurements provide a long-term, fair value target around $74.50 per share. That means that GSK is significantly undervalued, with about 80% upside from its current price.

Technical Profile

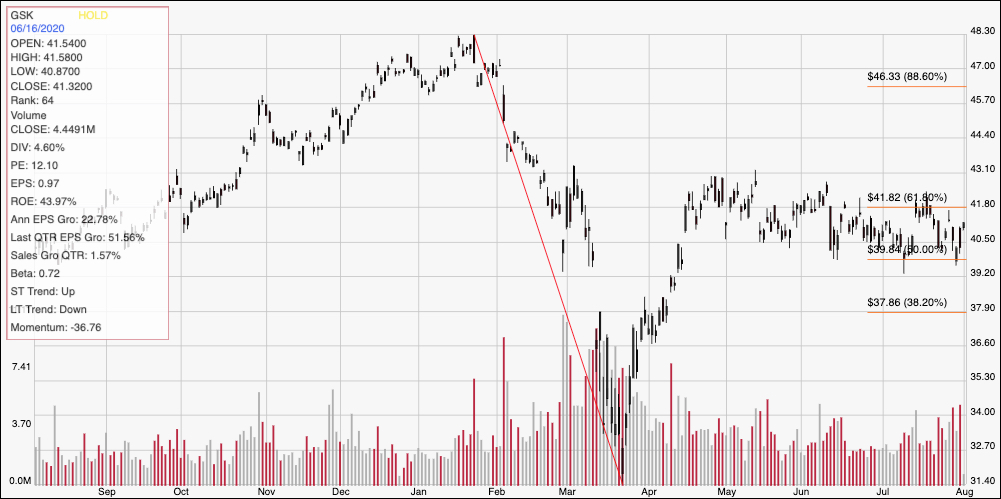

Here’s a look at the stock’s latest technical chart.

Current Price Action/Trends and Pivots: The red diagonal line defines the stock’s downward trend from a January high at around $48 to is bear market low around $31.50 in March. It also provides the baseline for the Fibonacci retracement lines shown on the right side of the chart. After rallying to about $43 by mid-April, the stock began to drift mostly sideways, but following a gradual downward trend that has seen the stock establish a narrow trading range, with resistance right around the 61.8% retracement line, near $42, and support around $40, roughly in line with the 50% line. A break above $42 may need to see the stock push past its April high around $43 to validate a bullish signal, but offers initial upside to about $46 where the 88.6% retracement line sits. A drop below $40 should see the stock fall to about $38, where the 38.2% retracement line rests before finding next support.

Near-term Keys: GSK’s balance sheet strength, along with improvement in Net Income and Free Cash Flow are strong indications of the company’s overall fundamental strength. The fact that the stock is trading at a significant discount is also a very positive sign that could make the stock one to watch and to take seriously as a useful, long-term value opportunity. If you prefer to work with short-term trading strategies, you could use a break above $42 as a signal to buy the stock or work with call options, using $46 as a useful bullish profit target; but keep in mind that a break above $43 would act as a higher-probability signal. If the stock falls below $40, you could also consider shorting the stock or buying put options, using the 38.2% retracement line at around $38 as an early, quick-hit bearish profit target.