In the early stages of the arrival and spread of COVID-19 in the United States, I wrote in this space about my belief that one of the best places a smart investor should focus their attention is on healthcare stocks, including companies in the pharmacy space. This week has seen the pandemic take center stage, even pushing political commentary about the upcoming election. Increasing infections moving into winter aren’t just being seen in the U.S. but in Europe as well, have a lot of people back on edge, which means that volatility is likely to continue to be a big theme in the market.

In the U.S., investors have been looking to Washington throughout the year to calm fears that the pandemic will incur unrecoverable economic damage. That theme isn’t likely to change, but the reality that Congress isn’t likely to even begin to approach the question again until after the election has a lot of economists warning that evictions and mortgage defaults across the country could start to rise at during the coldest portion of the year, which of course is only adding fuel to the bearish fire this week.

Continued uncertainty that starts with the health crisis, how long it will last, and how quickly any kind of realistic treatments of vaccines will be made available are our loved ones means, at least in part, that I believe pharmacies are going to continue to be the smartest investments to make through the rest of the year. On a local level, much of the localized testing that is available for COVID-19 will come from pharmacies like Walgreens Boots Alliance (WBA) and CVS Corp (CVS), to name just a couple. Along with that is the still, ever-present need to deal with everyday ailments and conditions. It’s pretty safe to say that if the pharmacy isn’t already a regular part of your daily life, it will be in the months ahead in one form or another.

CVS is a stock I’ve kept in my watchlist for years, and that performed well into the summer months after hitting a bear market low in March around $52 per share. Much of that increase came as part of broad-based market momentum into the beginning of June, when the stock hit a high point at around $70 per share before dropping back and consolidating in July between $65 and $62 per share. The beginning of September saw the stock drop below that range, with the last few days providing a new bearish push to put the stock just a few dollars above its bearish low. Current momentum is clearly being driven by broader market sentiment – but the truth is that these lower prices are just making the stock’s value proposition look better and better all the time. The company is uniquely positioned for the current environment, with what I think is a big competitive advantage from its 2018 merger with insurer Aetna. If this stock isn’t already on your radar, it really should be.

Fundamental and Value Profile

CVS Health Corporation, together with its subsidiaries, is an integrated pharmacy healthcare company. The Company provides pharmacy care for the senior community through Omnicare, Inc. (Omnicare) and Omnicare’s long-term care (LTC) operations, which include distribution of pharmaceuticals, related pharmacy consulting and other ancillary services to chronic care facilities and other care settings. It operates through three segments: Pharmacy Services, Retail/LTC and Corporate. The Pharmacy Services Segment provides a range of pharmacy benefit management (PBM) solutions to its clients. As of December 31, 2016, the Retail/LTC Segment included 9,709 retail locations (of which 7,980 were its stores that operated a pharmacy and 1,674 were its pharmacies located within Target Corporation (Target) stores), its online retail pharmacy Websites, CVS.com, Navarro.com and Onofre.com.br, 38 onsite pharmacy stores, its long-term care pharmacy operations and its retail healthcare clinics. CVS has a market cap of $81 billion. Aetna Inc. is a diversified healthcare benefits company. The Company operates through three segments: Health Care, Group Insurance and Large Case Pensions. It offers a range of traditional, voluntary and consumer-directed health insurance products and related services, including medical, pharmacy, dental, behavioral health, group life and disability plans, medical management capabilities, Medicaid healthcare management services, Medicare Advantage and Medicare Supplement plans, workers’ compensation administrative services and health information technology (HIT) products and services. The Health Care segment consists of medical, pharmacy benefit management services, dental, behavioral health and vision plans offered on both an Insured basis and an employer-funded basis, and emerging businesses products and services. The Group Insurance segment includes group life insurance and group disability products. Its products are offered on an Insured basis. CVS has a market cap of $74.4 billion.

Earnings and Sales Growth: Over the last twelve months, earnings for CVS improved by almost 40%, while sales growth was narrower, but rose 3%. In the last quarter, earnings were about 38% higher, while sales were somewhat negative, by -2.12%. CVS’ margin profile is narrow, but also gradually improving; over the trailing twelve months, Net Income as a percentage of Revenues was 3.13% (versus 2.76% for the same period a quarter ago), and 4.55% in the last quarter (versus 3.01% in the quarter prior).

Free Cash Flow: CVS’s free cash flow is healthy and continues to improve; over the trailing twelve month period this number was $13.6 billion – an increase from $11.7 billion for the same period in the quarter prior and $8.4 billion in April of 2019. The current figure translates to a Free Cash Flow Yield of 17.52% – a significant improvement from early 2019 when it was 7.28%.

Debt to Equity: CVS has a debt/equity ratio of .93. This is number that is primarily attributable to the massive increase in debt the company preemptively took on at the end of 2018 when its merger with insurer Aetna was first announced. CVS also took on additional, incremental debt at the beginning of the current pandemic to shore up its cash reserves. Total long-term debt is about $63.4 billion, while cash and liquid assets are about $17.4 billion (versus $12.7 billion in the last quarter, and 6.5 billion in March of 2019). By standard measurements, the company’s liquidity comes into question; however CVS has also laid out an aggressive debt reduction program that they expect will lower the total debt the combined company will be working with to much more conservative levels by 2022. Management has also suspended dividend increases and share repurchase programs for the time being while they work on debt reduction. Along with indications that integration efforts associated with combining two very distinct enterprises with each other are gaining traction, I believe it is safe to say that the company should have no problem servicing their debt.

Dividend: CVS pays an annual dividend of $2.00 per share. At the stock’s current price, that translates to a dividend yield of about 3.44%. It is also noteworthy that, while dividend increases have been suspended, management has maintained the dividend at current levels.

Price/Book Ratio: there are a lot of ways to measure how much a stock should be worth; but I like to work with a combination of Price/Book and Price/Cash Flow analysis. Together, these measurements provide a long-term, fair value target around $102.50 per share. It’s worth mentioning that just a quarter ago, my Fair Value target was just a little below $95 per share. That means the stock is trading at a massive discount, with 81% upside from the stock’s current price.

Technical Profile

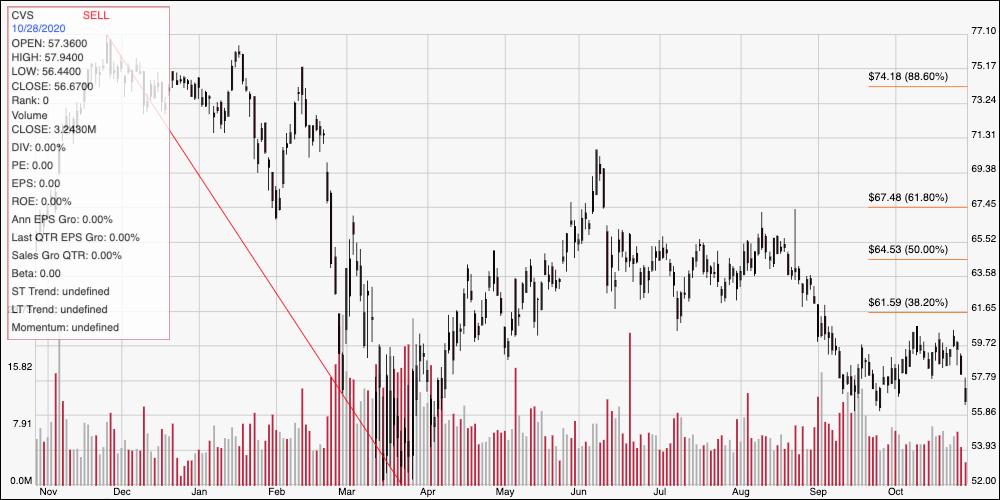

Here’s a look at CVS’ latest technical chart.

Current Price Action/Trends and Pivots: The diagonal red line marks the stock’s downward trend from November 2019 to March of this year. It also provides the baseline for the Fibonacci retracement lines shown on the right side of the chart. Throughout July, the stock hovered in a range between the 38.2% and 50% retracement lines before breaking above resistance at around $64.53 at the beginning of August. From that point, the stock set a consolidation range between $62 and $65, but broke below that level at the beginning of September. The stock’s new, immediate support is around $56, with the stock coming close to that level now. A push below that level could see the stock revisit its bear market low around $52. Immediate resistance it at $60, which means a bounce off support at around $56 has about $4 of immediate, range-based upside, with additional room to between $61.50 where the 38.2% retracement line rests and $62.

Near-term Keys: If you prefer to work with short-term trading strategies, the best opportunity on the bullish side would come from a bounce off of support at $56; that would be a good signal to buy the stock or work with call options with an eye on $60 as a near-term target and additional upside to about $61.50 if bullish momentum accelerates. A bearish signal would come from a drop below $56; in that case you could consider shorting the stock or buying put options, using $52 as a good bearish profit target. The stock’s value proposition is extremely attractive, and from a long-term perspective, I think continues to offer one of the best value opportunities in the stock market right now.