One of the big headlines to start the week has been the long-anticipated FDA approval of the first coronavirus vaccine in the United States. News media were all over shipping companies in the early hours of market trading today outlining in detail how the vaccine was being distributed on a nationwide basis. The scrutiny and attention isn’t all that surprising given the way the virus has persisted throughout the year and the hope that this and other vaccines will finally bring the pandemic to a resolution in 2021 that translates to a return of some kind of normalcy.

For corporate America, I think it is going to be interesting to see what a “return to normal” is really going to look like. The virus forced most companies to shift their office workforces into remote, work-from-home arrangements that most reports indicate worked pretty well in keeping business going and help keep historically high unemployment numbers early in the year from being even higher. Will 2021 mean that companies start bringing those employees back into traditional, in-office working operations, or will the forced shift to remote workforce solutions become a permanent arrangement for many of these organizations?

My guess is that the answer will lie somewhere in the middle. Most managers seem to agree that while remote arrangements worked better than expected, there is an implicit, if unquantifiable value in face-to-face interactions that companies have been forced to make do without this year. I think any return to previous working arrangements – or even a modified form of them – is a project that will take into the latter part of the next year to be completed. It won’t be the kind of immediate shift to remote work that many companies had to figure out on the fly. I also believe that many companies will choose to settle into a blended mode of operation, with some combination of remote and in-office work integrated into their operating model moving forward.

2020 also meant that the companies that provide commercial services – office equipment, supplies, and so on – have been challenged on their own, as overall demand for their goods and services saw a natural resulting drop. The shift back to in-office work means that many of these companies should see an increase in demand next year, and I think that will be true no matter whether a company chooses a blended form of operation or a complete return to office work.

Steelcase Inc. (SCS) is an example of the kind of company that I think is in a good position for whatever form business operations take in 2021. This is a small-cap company that holds a relatively large market share in the Office Service and Supplies industry. 2021 holds opportunity, but also uncertainty in the commercial space for this industry, which is why one of this company’s strengths is its exposure to other markets that should be more stable, including health care and education, in 2021. This is a company, that like everybody else this year, had to take strong measures to bolster its balance sheet and endure the difficulties imposed by the pandemic, including layoffs, salary reductions, and a reduction (but not elimination or suspension) of its dividend; but their fundamental profile also shows a manageable level of debt, healthy free cash flow and liquidity, and an operating profile that has strengthened in the most recent quarter. Along with a very interesting value proposition, this could mean that SCS is a stock you should be paying attention right now.

Fundamental and Value Profile

Steelcase Inc. provides an integrated portfolio of furniture settings, user-centered technologies and interior architectural products. The Company’s segments include Americas, EMEA and Other Category. The Company’s furniture portfolio includes panel-based and freestanding furniture systems and complementary products, such as storage, tables and ergonomic worktools. Its seating products include task chairs, which are ergonomic seating that can be used in collaborative or casual settings and specialty seating for specific vertical markets, such as healthcare and education. Its technology solutions support group collaboration by integrating furniture and technology. Its interior architectural products include full and partial height walls and doors. It also offers services, which include workplace strategy consulting, lease origination services, furniture and asset management and hosted spaces. Its family of brands includes Steelcase, Coalesse, Designtex, PolyVision and Turnstone. SCS has a current market cap of $1.5 billion.

Earnings and Sales Growth: Over the last twelve months, earnings increased 10%, while sales were about -18% lower. In the last quarter, the picture improved significantly, with earnings increasing 405% and sales moving 69.5% higher. SCS operates with relatively narrow margin profile, with Net Income running at 4.33% of Revenues over the last year. That profile strengthened in the last quarter as Net Income increased to 6.78% of revenues.

Free Cash Flow: SCS’ Free Cash Flow can be pretty cyclical, but management has been able to manage this element of fundamental effectively throughout the year. In the last twelve months, SCS reported almost $313 million in Free Cash Flow, which translates to a Free Cash Flow Yield of almost 22%. It also marks a modest improvement from $289 million at the beginning of the year.

Debt to Equity: SCS has a debt/equity ratio of .51, which is pretty conservative. Their operating profits are adequate to service their debt, with $515.9 million in cash and liquid assets versus $480.7 million in long-term debt..

Dividend: SCS pays an annual dividend of $.40 per share – reduced earlier this year from $.54 – which at its current price translates to a dividend yield of 3.2%.

Value Proposition: there are a lot of ways to measure how much a stock should be worth; but I like to worth with a combination of Price/Book and Price/Cash Flow analysis. Together, these measurements provide a long-term target at about $19 per share. That suggests that SCS is very undervalued, by about 48%.

Technical Profile

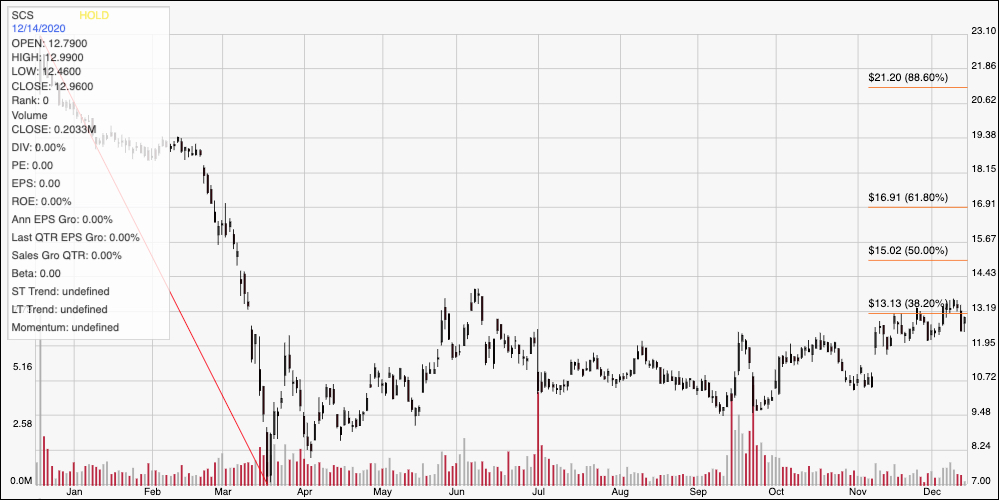

Here’s a look at the stock’s latest technical chart.

Current Price Action/Trends and Pivots: The chart above displays the last year of price activity; the red diagonal line traces the stock’s downward trend from late 2019 at a high around $23 to its bear market low around $7 per share. It also provides the baseline for the Fibonacci retracement lines shown on the right side of the chart. The stock rallied in June to about $14 before dropping back and settling into a range between $9.50 and $12 until early November. The stock broke above that range at that point and has been testing resistance a little above $13 for most of the past month. A move to about $13.50 would mark a significant new resistance break, with upside to the $15 mark where the 50% retracement line sits, or possibly $17, inline with the 61.8% line if bullish sentiment strengthens. Current support is at $12; a drop below that point should see the stock find next support somewhere between $11 and $10 based previous pivots in that range.

Near-term Keys: SCS is an interesting company in an industry that I think is going to see better days in the year ahead. Their ability to manage their balance sheet effectively this year despite the pressures associated with the pandemic is a testament to management’s ability and discipline. The value proposition is very interesting, which is why I think this is a smart stock to pay attention to in the months ahead. If you prefer to focus on short-term strategies, you could use a break above resistance to $13.50 as a signal to think about buying the stock or working with call options, using $15 to $17 as profitable short-term exit points. A drop below $12 offers little in the way downside to make a bearish trade attractive. The exception to that rule would be in the case of a drop below $9.50; in that case, you could consider shorting the stock or buying put options with target price at around $7 per share.