Uncertain economic conditions are often a good time to think about stocks that most people tend to overlook because they’re “boring.” These are stocks that also tend to operate in counter-cyclical fashion. They often make up segments of the economy that you and I rely on every day, but that don’t generate the same kind of buzz among market analysts and talking heads as sexier areas. A lot of good examples have been found in the last year in the Food Products industry, where pandemic-driven trends have had a big impact on demand. Over the last year, a lot of the stocks in this industry have shown a lot of resilience, with more tempered moderation during periods of increasing uncertainty while stocks in industries usually considered “trendier” are getting thumped.

In the early stages of the pandemic, Food Products stocks were the clear winners, as consumers clamored to stock up on basic home supplies and other packaged, non-perishable food products, like canned food, prepackaged meat, and so on. Most of the pandemic-induced fear drove that initial surge has faded, and is even being replaced by optimism about being able to resume some kind of “normal” level of activity later this year; however it is also worth nothing while broad economic pressure from still-historically high unemployment isn’t going to go away soon. The overall trend in unemployment numbers is still moving in the right direction, but both the Fed and the Treasury Department have been clear about their opinions about the need for continued accommodation from monetary and federal policy to support those who are still out of work. I think the continued need for vigilance and caution related on the COVID front, along with negative pressure from unemployment still provides two big reasons that economists continue to forecast steady demand for household goods, including pantry, fridge and freezer foods – which offers a headwind that makes this industry a natural fit for anybody that wants to find places to invest that could represent “safe havens” within the market that aren’t as sensitive to economic downturns and prolonged periods of uncertainty.

Prepackaged food stocks like Hormel Foods Corp (HRL), CPB, and KHC have all been facing significant challenges over the last couple of years related to changing consumer preferences. HRL occupies a somewhat different niche than some of these other stocks, however because its products fit nicely into that shift towards healthier choices, with a specific emphasis on proteins. That also fits into related reports regarding China, which is increasing protein imports to make up for domestic supply shortages from the swine flu pandemic a year or so ago that ravaged its pork capacity. HRL specifically noted increasing orders for SPAM for China. This is a company that is also taking advantage of opportunities to diversify its business, as its recently announced $2.8 billion acquisition of KHC’s Planters-branded snack business (expected to close sometime in the second quarter of this year) gives it a way to begin moderating some of the commodity-driven risk associated with its heavy emphasis on protein products.

A lot of prepackaged food companies have business segments dedicated to foodservice – primarily referring to supply to restaurants – and grocery. One of the interesting ways a number of companies in this industry were forced to adjust in 2020 was to de-emphasize foodservice channels, where forced shutdowns across the globe shuttered restaurants and social dining and focus more on grocery, where those same orders prompted an increase in food storage and consumption at home. The expected recovery of foodservice provides a good potential tailwind that could work in HRL’s favor in the second half of this year. A broad recovery in restaurant dining should benefit suppliers like HRL in a meaningful way. Despite those pressures over the past year, the company carries a very strong fundamental profile that includes a very healthy balance sheet. The stock is also currently consolidating in a harrow range just a few dollars above its 52-week low. Does that also mean the stock offers a good value for defensive-minded investors? Let’s take a look.

Fundamental and Value Profile

Hormel Foods Corporation is engaged in the production of a range of meat and food products. The Company operates through four segments: Grocery Products, which is engaged in the processing, marketing and sale of shelf-stable food products sold for the retail market and health and also consists of nutrition products, including Muscle Milk protein products.; Refrigerated Foods, which consists of the processing, marketing and sale of branded and unbranded pork, beef, chicken and turkey products for retail, foodservice and fresh product customers; Jennie-O Turkey Store (JOTS), which consists of the processing, marketing and sale of branded and unbranded turkey products for retail, foodservice and fresh product customers; and International & Other, which includes Hormel Foods International Corporation, which manufactures, markets and sells the Company products internationally. HRL’s market cap is about $25.9 billion.

Earnings and Sales Growth: Over the last twelve months, earnings declined -8.9%, while sales increased 3.22%. In the last quarter, earnings slid -4.65%, while sales were 1.7% higher. The company’s margin profile is healthy; over the last twelve months, Net Income was 9.16%, and moderated only slightly to 9.03% in the most recent quarter.

Free Cash Flow: HRL’s free cash flow was a little over $797.9 million over the past twelve months and translates to a modest Free Cash Flow Yield of 3.04%. It should be noted that Free Cash Flow was about $762 million in the last quarter, and $619.5 million at the end of 2019.

Dividend Yield: HRL’s dividend is $.98 per share, and translates to a yield of 2.03% at its current price. It is also noteworthy that HRL increased their dividend in 2020; it was $.84 per share on an annualized basis as recently as October of last year. HRL is on a select list of S&P 500 “dividend aristocrats,” having increased its dividend every year for the last 54 years.

Debt to Equity: HRL has a debt/equity ratio of .16. This is a very low number that is clearly representative of the company’s conservative use of leverage and its approach to debt management. In the last quarter, HRL’s balance sheet showed about $1.77 billion in cash and liquid assets against $1.04 billion in long-term debt.

Price/Book Ratio: there are a lot of ways to measure how much a stock should be worth; but I like to work with a combination of Price/Book and Price/Cash Flow analysis. Together, these measurements provide a long-term, fair value target around $41.55 per share. At the end of 2020, this measurement was about $39 per share, so this is another useful sign of fundamental strength; however, it also means that the stock is overvalued right now, with -14% downside from its current price, with a useful discount price at around $33.50.

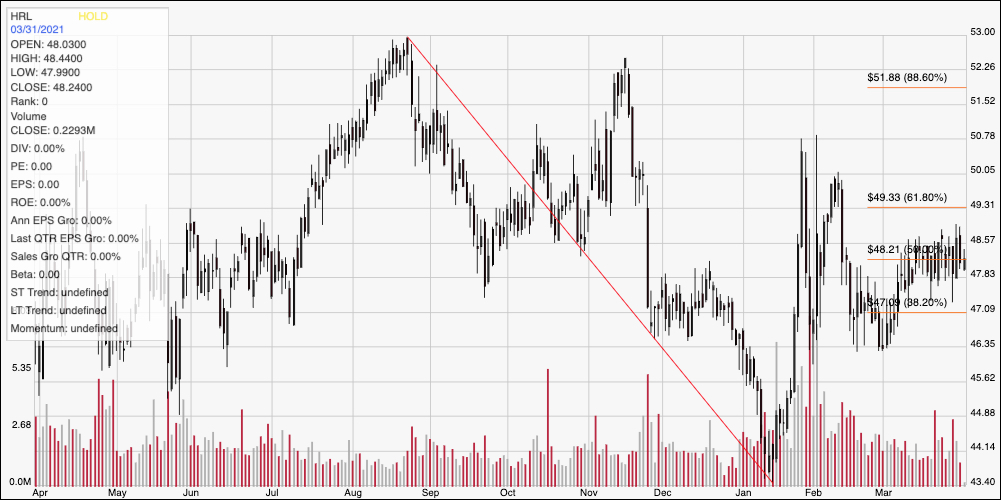

Technical Profile

Here’s a look at the stock’s latest technical chart.

Current Price Action/Trends and Pivots: This chart traces the stock’s movement over the last year. The diagonal red line traces the stock’s downward trend from August 2020 to its low at around $43.50 in January. It also acts as the baseline for the Fibonacci retracement lines shown on the right side of the chart. The stock rallied strongly at the end of January, with a lot of volatility in the early part of February as well; after that, the stock dropped to a low at around $46 before settling into a tight, narrow range over the last few weeks between $48 and $48.50. The 61.8% retracement line, at around $49 should be considered next resistance if the stock breaks out of its current range, with additional upside to around $51 or $52 based on the stock’s January pivot high as well as the 88.6% retracement line. A drop below $48 should find next support at around $47, where the 38.2% retracement waits, with additional support a little above $46. A drop below $46, however should see near-term downside to test the stock’s 52-week low at around $43.50.

Near-term Keys: HRL’s fundamentals are solid, especially considering the challenging conditions just about every sector in the market has had to deal with during the pandemic; unfortunately, however the stock’s price performance doesn’t add to the value proposition. Short-term trading strategies are also a bit difficult with this stock given the tight ranges between immediate and next support or resistance levels. That said, a push above $49 could offer a signal to think about buying the stock or working with call options, using $52 to $53 as near-term exit targets for a short-term bullish trade. A drop below $46 could act as a signal to consider shorting the stock or buying put options, using the stock’s 52-week low at around $43.50 as a useful profit target on a bearish trade.