Sometimes there are really remarkable events that diverge from the normally expected narrative that plays out in the markets. “Expected” events are what we usually expect to see talking heads discussing and analyzing – economic reports, consumer activity, monetary policy, the way the latest political intrigue will be felt, and for the past year, the affect the pandemic continues to have. Every so often, however there is a new storyline that emerges to spice things up and keep things really interesting.

This week, one of those storylines came from the news that a “family office” was on the verge of bankruptcy after being severely over-leveraged at the wrong time. The market has started using this term to describe wealthy investors who manage their own money. They are organized as legitimate businesses, and hire personnel to help with their analysis, but these firms don’t solicit capital from other investors, and so they generally don’t fall under the same kind of regulatory scrutiny that hedge funds, mutual funds or other investment management services do.

The impact of leverage on investing is twofold. First, if you are right, the extra shares (or contracts, if you’re working with options) you can work with increase the amount of money you can make – you get a bigger “bank for your buck.” For this particular family office, the aggressive use of leverage meant they made billions of dollars over the past year.

The thing that you have to keep in mind about leverage is that it cuts both ways. While it accelerates your gains when you’re right, it does the exact same thing when you’re wrong. For this family office, when one of their heavily leveraged positions – ViacomCBS Inc. (VIAC) announced last week announced it would be selling new shares to the market. The news diluted the value of existing shares, precipitating a 25% drop shortly afterward. That started a cascading disaster for this family office, which had to start selling other positions to cover margin calls on its borrowed assets. Increased selling – not just by this family office, but other investors as well – precipitated more declines in VIAC’s stock price, accelerating the problem even more.

The story itself is certainly a cautionary one about the dangers of leverage, and should be taken as such to every investor, no matter how large or small. Leverage can be effective if properly used and carefully managed – but you also have to be cognizant of how much your exposure to risk increases when you use it, and be prepared to act quickly if things go against you. The really interesting part of the story I take away, however is more about VIAC itself.

This is a company that was formed by the merger of two broadcast media giants – Viacom and CBS – to be more effective as a combined company in an ever more competitive landscape in its industry. Traditional broadcast channels – cable, satellite TV, and so on – continue to be affected by “cord-cutters” that are shifting more and more to streaming channels – not just for movies and TV series, but also for sports programming. Amazon, for example just paid a king’s ransom for exclusive rights to Thursday Night Football, and VIAC is moving to stay just as relevant, having over paid for an extension of its NFL contract, and also adding Euroleague soccer to its streaming lineup as well.

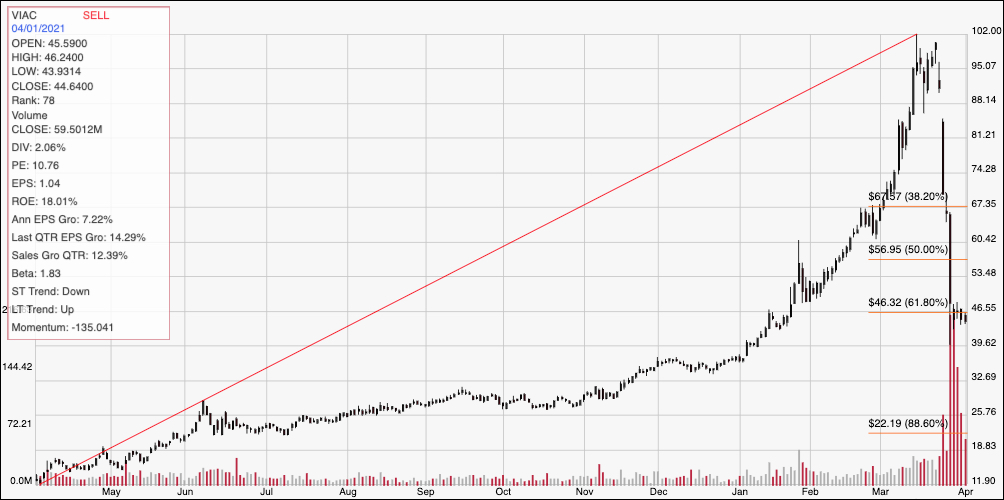

This is a stock that rose from about $12 a year ago to about $35 by the start of 202; but from that point the stock soared, rising to a high just a couple of weeks ago to around $102 per share. The initial announcement of new shares started the stock tumbling, but the margin-induced selling has also pushed the stock to around $45 as of this writing – a decline of more than 50% below those highs. It look like it could finally be reaching a practical consolidation level; if so VIAC could represent one of the best values in a broadly extended bullish market. Let’s dive in.

Fundamental and Value Profile

ViacomCBS Inc., formerly CBS Corp, is a global media and entertainment company. The Company is focused on creating premium content and experiences for audiences worldwide. It operates through various brands, including CBS, Showtime Networks, Paramount Pictures, Nickelodeon, MTV, Comedy Central, BET, CBS All Access, Pluto TV and Simon & Schuster, among others. It also offers production, distribution and advertising solutions for partners across five continents. BET is the primary channel of BET Networks, that provides entertainment, music, news and public affairs television programming for the African-American audience. CBS Sports brand is a broadcaster of television sports. Its Paramount Pictures brand is a producer and global distributor of filmed entertainment. Its CBS Television Studios is a supplier of programming with more than 70 series in production across broadcast and cable networks, streaming services and other platforms. Its brands also include Bellator MMA and COLORS. VIAC has a current market cap of about $28.6 billion.

Earnings and Sales Growth: Over the last twelve months, earnings increased by about 7.25%, while revenue was flat, but positive 0.04%. In the last quarter, earnings were 14.3% higher, while revenues grew 12.4%. VIAC operates with a healthy, strengthening operating profile; over the last twelve months, Net Income was 9.34% of Revenues, and grew to a little over 13% in the last quarter.

Free Cash Flow: VIAC’s free cash flow is healthy, at $1.97 billion. This number increased from about $771 million a year ago, but did drop in the last quarter from about $2.9 billion. The current number translates to a Free Cash Flow Yield of 7.15%.

Dividend: VIAC’s annual divided is $.96 per share, which translates to a compelling yield of 2.15% at the stock’s current price.

Debt/Equity: VIAC carries a Debt/Equity ratio of 1.26, which is a bit high, but not unusual for stocks in this industry. Their balance sheet shows almost $3 billion in cash and liquid assets versus $19.7 billion in long-term debt. Their operating profile suggest that the company should have no problem servicing their debt, with good flexibility and liquidity to go along with it.

Price/Book Ratio: there are a lot of ways to measure how much a stock should be worth; but I like to work with a combination of Price/Book and Price/Cash Flow analysis. Together, these measurements provide a long-term, fair value target a little below $89.50 per share. That suggests that the stock is significantly undervalued right now, with about 100% upside (not a typo) from its current price.

Technical Profile

Here’s a look at the stock’s latest technical chart.

Current Price Action/Trends and Pivots: This chart looks at the last year of price activity for VIAC. The red diagonal line measures the length of the stock’s upward trend from a low at around $12 to its peak in March at around $102; it also informs the Fibonacci trend retracement lines shown on the right side of the chart. Starting last week, the stock picked up significant bearish momentum, pushing the stock more than -50% lower as of yesterday’s close, and appearing to be looking for support at around the $45 level – right around the 61.8% retracement line. A bounce off of that level should see upside to about $57 where the 50% retracement line sits, while a drop below $45 could see the slide extend to somewhere between $39 and $35 based on pivot activity in that area in December.

Near-term Keys: VIAC is a stock under serious bearish pressure from a lot of institutional selling right now, and that means that the slide may not be over yet. Even so, the stock’s current price level does offer some useful clues you can use if you like to work with short-term trading strategies. Use a bounce off support at $45 as a signal to buy the stock or work with call options, using $57 as an attractive short-term bullish target. A drop below $45, on the other hand, should be taken as a strong signal to consider shorting the stock or buying put options, using $39 as a very useful bearish profit target. I think that it’s clear, given the company’s fundamental strength and value proposition, that the stock is extremely oversold; that means that if you are a patient investor, and aren’t afraid of a little volatility, this could be an excellent long-term opportunity to take a long-term, value-driven position.