Investors are always looking for the “next big thing” in the stock market to give them something to talk about with their friends. That is part of the reason that market media outlets tend to drive so much of the investing public’s focus on the fastest-growing industries. Along the way, stocks in other industries tend to get less attention, simply because they’re not as fun to talk about.

One of the most un-sexy segments of the market to talk about is Food, Food Products, and Food Retailing. That’s because Food is just a regular part of daily life – and grocery shopping is just another chore that everybody has to get out of the way to keep pantries and fridges stocked. The early stages of the pandemic created big increases in food storage and home consumption, and that is a trend that many analysts expect to persist as a long-term trend in American homes throughout the year even as the economy reopens and social activity. That has been a good thing for a lot of stocks in the Consumer Staples sector, and it should help continue to make stocks in the Food Products and Food Retailing industries attractive.

The increased consumer trend to eat-at-home has actually provided a good opportunity for value-focused investors, because while stocks in “sexy” sectors like Technology, Health Care and others are trading at unreasonably high value multiples, there are a number of stocks in the Consumer Staples sector that have performed well, but are still trading at very attractive multiples. That’s because while most sectors in the market are still having to contend with declines in revenues, earnings, and cash flow, strong home consumption has helped a lot of Food-related stocks improve their balance sheet strength and overall fundamental profile. Along the way, their “Fair Value” price targets have also been going up.

Kroger Company (KR) is a stock that clearly reflects the pattern I described earlier. After falling from a high at around $36 to a bear market low last year at around $28, the stock rallied strongly into August 2020 near to its pre-pandemic high, then dropped back again before the end of the year. The stock has since built a gradual, but clear upward trend that appears poised to keep driving higher.

KR has been among the most proactive in the entire Consumer Staples industry over the past couple of years, investing heavily in alternative revenues streams like Kroger Personal Finance and Kroger Precision Marketing, as well as online shopping and curbside delivery that is now in place in 95% of its coverage area. These have yielded positive results on the company’s earnings reports, and have enhanced the company’s ability to compete against larger rivals like Wal-Mart and Target Stores. I think the stock’s fundamentals give a bullish investor good reason to think about taking a long-term position; but are they strong enough to say the stock is still a big value? Let’s dive in and take a look.

Fundamental and Value Profile

The Kroger Co. (KR) manufactures and processes food for sale in its supermarkets. The Company operates supermarkets, multi-department stores, jewelry stores and convenience stores throughout the United States. As of February 3, 2018, it had operated approximately 3,900 owned or leased supermarkets, convenience stores, fine jewelry stores, distribution warehouses and food production plants through divisions, subsidiaries or affiliates. These facilities are located throughout the United States. As of February 3, 2018, Kroger operated, either directly or through its subsidiaries, 2,782 supermarkets under a range of local banner names, of which 2,268 had pharmacies and 1,489 had fuel centers. As of February 3, 2018, the Company offered ClickList and Harris Teeter ExpressLane, personalized, order online, pick up at the store services at 1,056 of its supermarkets. P$$T, Check This Out and Heritage Farm are the three brands. Its other brands include Simple Truth and Simple Truth Organic. KR has a market cap of $28.7 billion.

Earnings and Sales Growth: Over the last twelve months, earnings declined by about -2.5%, while sales slipped -0.6%. In the last quarter, earnings improved nearly 47% while revenues increased more than 34%. Like most Food retailers, KR operates with razor-thin margins, as Net Income was about 1.14% of Revenues for the last twelve months, and weakened in the most recent quarter to 0.34%. That, along with a flattening of revenues over the last couple of quarters, could be an indication that pandemic-correlated demand could be normalizing.

Free Cash Flow: KR’s free cash flow is healthy, at $1.97 billion over the last twelve months. That marks a decline from $4.1 billion in the last quarter and $3.8 billion in the quarter prior, and translates to a free cash flow yield of 6.8%.

Debt to Equity: KR has a debt/equity ratio of 1.41. This is higher than I usually prefer to see, but isn’t unusual for Food Retailing stocks. The company’s balance sheet indicates that operating profits are more than adequate to repay their debt, and is a sign of strength, with $3.3 billion in cash and liquid assets, up from $2.7 billion in the previous quarter, against $12.9 billion in long-term debt. Their long-term debt is a reflection of the capital-intensive investments in itself the company has made to stay competitive in its market.

Dividend: KR pays an annual dividend of $.84, which marks an increase from $.64 per share in early 2020 and $.72 per share in the quarter prior. The current payout translates to a yield of about 2.19% at the stock’s current price. The increasing dividend should be taken as management’s confidence in their operating model and ability to keep the business growing in the long-term.

Price/Book Ratio: there are a lot of ways to measure how much a stock should be worth; but I like to work with a combination of Price/Book and Price/Cash Flow analysis. Together, these measurements provide a long-term, fair value target around $49 per share. That means that even the stock’s healthy upward trend, KR remains undervalued by 29% from its current price.

Technical Profile

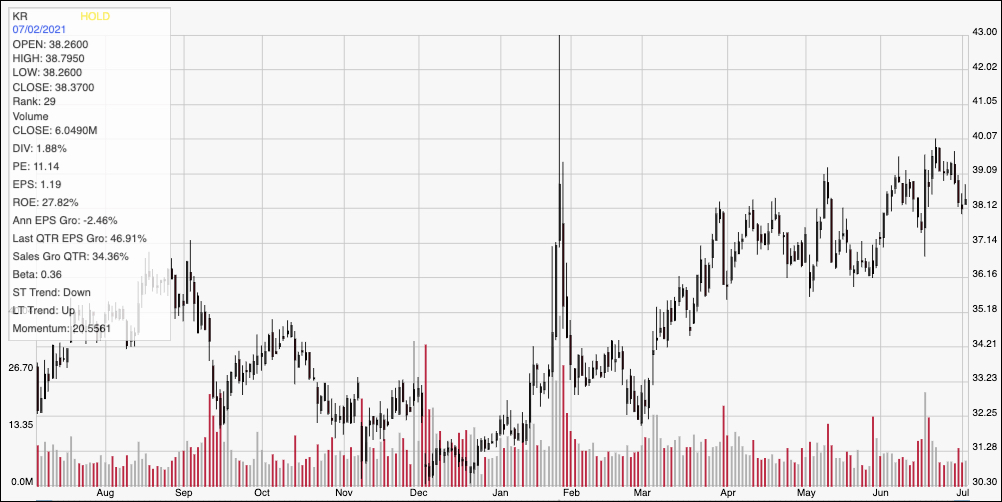

Here’s a look at the stock’s latest technical chart.

Current Price Action/Trends and Pivots: The chart above marks the last year of price movement for KR. The stock’s upward trend began in December 2020 at a low point around $30, and has been building from that point. Most recently, the stock hit a peak in late June at close to $40, and which marks immediate resistance as the stock has dropped from that point, with current resistance right around $38 based on pivot activity in that range in March and April. A push above $40 should see short-term upside to about $42 based on the distance between those support and resistance levels, while a drop below $38 should find next support somewhere between $37 and $36 per share.

Near-term Keys: For a short-term trade, the probability right now is clearly on the bullish side; if you want to be aggressive with a short-term trade by buying the stock or working with call options, you could use the stock’s current push off of support around $38 as a good opportunity to initiate a bullish trade, with room to $40 as a first profit target and $42 if bullish momentum accelerates. The strength of the stock’s upward trend actually makes a bearish-oriented trade pretty speculative right now, however a drop below $36 could be an early sign that the upward trend could be about to reverse and so could act as a useful signal to consider shorting the stock or working with put options, with an eye on a very short-term profit target at around $33 per share. I like KR’s value proposition and overall fundamental profile; despite some operating challenges in the most recent quarter, I rank it among very few companies that has showed positive signs of growth in the difficult environment that is a pandemic. I think KR remains a solid stock to consider as a long-term investment right now.