Looking for value in the stock market is something that I have found can be done in any market condition, but it is something that tends to get dismissed by most pundits simply because it isn’t very sexy. Popular, “buzzy” names like Tesla, Netflix, and Amazon practically never pass the value list because the massive amount of attention the market has given them for years has kept their stocks priced at levels that makes them impractical for an objective analysis based strictly on value. More often than not, looking for value means passing over the names and pockets of the market that get the most attention from media and the general investing public to dig into the industries that everyone else tends to overlook.

If you’ve been following me in this space at all, or participating in my weekly options trading webinar, you already know that CVS Health (CVS) is a good, old friend that I’ve followed for quite some time. Since my last review on this stock, the company has released a new earnings report, which shows a useful increase in some of my favorite fundamental metrics and pressure on others. The stock itself has been a star performer for the past year, rising from about $68 at the beginning of March 2021 to a peak early this month at around $111. From that high, the stock has been following the pattern of the broad market and is about -7.5% lower.

Interest rate fears, along with geopolitical pressures have combined over the last week to increase uncertainty and keep volatility in the market pretty high. The potential for military conflict between Russia and Ukraine has pushed the price of crude to levels above $90 that haven’t been seen for the last six and a half years, with plenty of economic indicators continuing to show increases in inflation that have members of the Federal Reserve Board of Governors at odds about how quickly and severely rates should be increased. In the last week, for example, the governor of the St. Louis Fed has publicly stated on two occasions his belief that the Fed should be more aggressive and decisive, including raising rates by a full point in March. Among the biggest catalysts for bearish momentum the market has always responded to is the fear of rapidly increasing interest rates, so a potentially more hawkish Fed, along with global political uncertainty could be a toxic mix.

The elements I just described are only the latest to pile on to the reality that the pandemic continues to put pressure on health care systems around the world, and will remain a risk factor that we have to contend with for the foreseeable future. I think one of the takeaways investors can take related to the pandemic is that the role CVS and other pharmacy companies will continue to be an important of the story. This is a company that was already gaining traction in its broad transformation from just a drugstore/specialty retailer to a health care company providing a variety of services locally and affordably, and it is hard not to take CVS seriously. The company is uniquely positioned for the current environment, not only in the pharmacy space but also with what I think is a big competitive advantage over the rest of its industry owing to its 2018 merger with insurer Aetna.

The stock’s long-term trend can be interpreted as a sign that the stock’s latest drop is just another, classic opportunity to “buy the dip” and keep riding the trend higher; but I think that some of the larger issues that are starting to overshadow the market might present an increasing risk that the opposite is true, and that since all trends are finite and will inevitably reverse back against themselves, CVS could be at a critical tipping point where the risk doesn’t justify the potential reward. The trend also naturally begs the question of where the stock’s useful, value-oriented price should be. Let’s dig in to find out.

Fundamental and Value Profile

CVS Health Corporation, together with its subsidiaries, is an integrated pharmacy healthcare company. The Company provides pharmacy care for the senior community through Omnicare, Inc. (Omnicare) and Omnicare’s long-term care (LTC) operations, which include distribution of pharmaceuticals, related pharmacy consulting and other ancillary services to chronic care facilities and other care settings. It operates through three segments: Pharmacy Services, Retail/LTC and Corporate. The Pharmacy Services Segment provides a range of pharmacy benefit management (PBM) solutions to its clients. As of December 31, 2016, the Retail/LTC Segment included 9,709 retail locations (of which 7,980 were its stores that operated a pharmacy and 1,674 were its pharmacies located within Target Corporation (Target) stores), its online retail pharmacy Websites, CVS.com, Navarro.com and Onofre.com.br, 38 onsite pharmacy stores, its long-term care pharmacy operations and its retail healthcare clinics. CVS has a market cap of $81 billion. Aetna Inc. is a diversified healthcare benefits company. The Company operates through three segments: Health Care, Group Insurance and Large Case Pensions. It offers a range of traditional, voluntary and consumer-directed health insurance products and related services, including medical, pharmacy, dental, behavioral health, group life and disability plans, medical management capabilities, Medicaid healthcare management services, Medicare Advantage and Medicare Supplement plans, workers’ compensation administrative services and health information technology (HIT) products and services. The Health Care segment consists of medical, pharmacy benefit management services, dental, behavioral health and vision plans offered on both an Insured basis and an employer-funded basis, and emerging businesses products and services. The Group Insurance segment includes group life insurance and group disability products. Its products are offered on an Insured basis. CVS has a market cap of $134.6 billion.

Earnings and Sales Growth: Over the last twelve months, earnings increased by about 52.3%, while Revenues rose by a little over 10%. Earnings were flat, but positive in the last quarter by 0.51% while sales were about 3.8% higher. The company’s margin profile is very narrow, and is showing some weakness; over the last twelve months Net Income was 2.71% of Revenues, and slipped to 1.7% in the last quarter.

Free Cash Flow: CVS’s free cash flow is very healthy, at nearly $15.74 billion. That marks an improvement from $12.9 billion a year ago, and a little under $15.2 billion in the quarter prior. The current number translates to an attractive Free Cash Flow Yield of about 11.44%.

Debt to Equity: CVS has a debt/equity ratio of .69. That is a generally conservative number that has dropped steadily from 1 a little over a year ago. In the last quarter Cash and liquid assets were about $12.5 billion (compared to $10.1 billion two quarters ago) versus $51.9 billion in long-term debt. The vast majority of that debt comes from the acquisition of health insurer Aetna, however the fact that long-term debt has dropped from about $65 billion since the beginning of 2020, with about $5 billion of that coming in the last quarter, is a good reflection of the company’s success so far (with plenty of work still to go) in transitioning these disparate organizations into a larger, productive company.

Dividend: CVS pays an annual dividend of $2.20 per share, and which translates to an annual yield that of about 2.11% at the stock’s current price. It is also noteworthy that, while dividend increases were been suspended (not because of COVID, but to give the company flexibility to reduce debt gradually from the Aetna merger) beginning in 2020, management maintained the dividend throughout the pandemic and announced the first increase, along with a new stock buyback program after the latest announcement.

Value Proposition: there are a lot of ways to measure how much a stock should be worth; but I like to work with a combination of Price/Book and Price/Cash Flow analysis. Together, these measurements provide a long-term, fair value target at about $92 per share. That suggests the stock is close overvalued, with -11% upside from its current price, and a practical discount price at $73.50.

Technical Profile

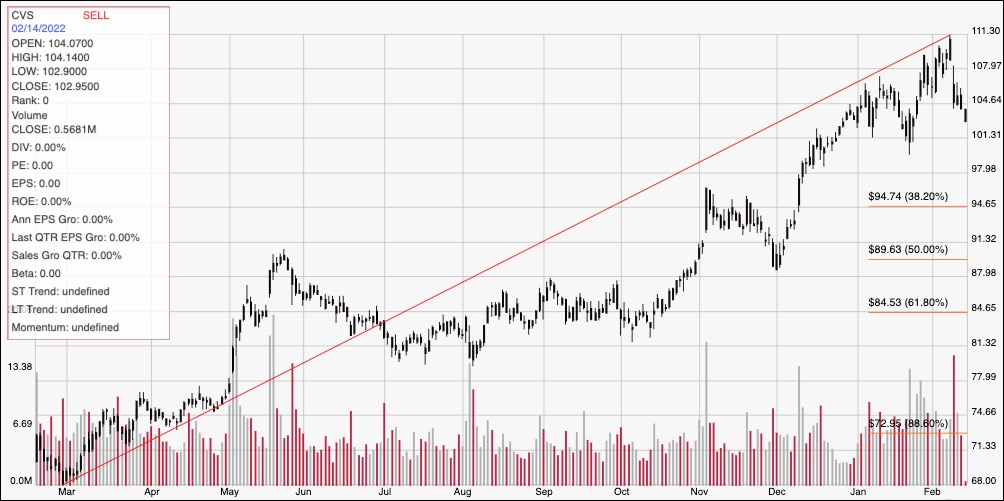

Here’s a look at CVS’ latest technical chart.

Current Price Action/Trends and Pivots: The diagonal red line marks the stock’s upward trend from February 2021 to its peak earlier this month at around $111. It also provides the baseline for the Fibonacci retracement lines shown on the right side of the chart. The stock has been dropping from that peak as broad market momentum has turned increasingly bearish, and has dropped in the early part of today’s session below $104.50, marking a drop below previous support that should now act as immediate resistance. Current support should be at around $101. A drop below $101 could have near-term downside to about $95 before finding next support, while a push above $104.50 could have room to retest the stock’s 52-week high at around $111.

Near-term Keys: If you prefer to work with short-term trading strategies, the best opportunity on the bullish side would come from break above resistance at $104.50; that would be a good signal to buy the stock or work with call options with an eye on $111 as a useful exit point, however I think that the current shift in momentum actually puts the best, directional probability on the bearish side. A bearish signal would come from a drop below $101, with $95 providing a useful target no matter whether you choose to short the stock or buy put options. From the standpoint of value and long-term opportunity, the stock’s yearlong upward trend has outpaced the company’s fundamental strength, and the recent pullback hasn’t come back far enough to make the stock a useful value opportunity. For practical purposes, the stock would need to fall to around $73.50 before I think a compelling, value-based argument can be made.