Trying to keep a thumb on the pulse of the market is an inexact science at best. I’ve learned to start by narrowing my focus on a single industry or sector, and then work outward.

One of the sectors that I have learned to pay attention to as a starting point to find the temperature the economy in general is the Materials sector. That’s because the companies that comprise it produce or mine many of the raw materials that make up the building blocks for most of the finished goods we use every day. The sector includes industries that cover chemicals and plastics, construction materials, paper, forest, and packaging products, as well as metals and minerals – which means that in some form, this sector touches practically every other segment of the economy in one more or another.

Since 2022 started, the market’s volatility has increased amid inflation and interest rate fears, and have been compounded by the war in Ukraine that shows no signs of peaceful resolution in the foreseeable future. During that time, stocks in the Materials sector have certainly not been immune to the broad market’s momentum. With energy prices still sitting at levels not seen in nearly a decade, the challenges that have driven the market’s momentum so far this year seem likely to remain in place. That means they could continue to act as a headwind to blunt the pace of economic growth that has prompted the Fed to implement progressively more aggressive, incremental interest rate increases throughout the year. Whether these varying elements will be a positive, or a negative for the Materials sector depends, I think on the specific niche a company operates in and their exposure to larger commodity movements.

Huntsman Corp (HUN) is a company that has benefitted from a homebuilding industry that has been surprisingly robust since late 2020 and all of last year, as residential construction saw big increases in numerous parts of the country. From its bear market low in March at around $12, the stock more than doubled in price by the end of 2020, and peaked in late February of this year at almost $42. From that point, however, the stock has followed broad market momentum downward, not finding a bottom to its own bearish push until June at around $27.50. The stock has been trying to rally from that point, and is a little below $30 as of this writing. That gradual increase seems to dovetail nicely with a fundamental profile that includes increasing cash flow, and a healthy balance sheet. Against that fundamental backdrop, the stock’s latest price activity begs the question of whether the stock might offer a useful value proposition, along with a nice technical bullish signal to think about. Let’s dive in.

Fundamental and Value Profile

Huntsman Corporation is a manufacturer of differentiated organic chemical products and of inorganic chemical products. The Company operates all of its businesses through its subsidiary, Huntsman International LLC (Huntsman International). The Company operates through five segments: Polyurethanes, Performance Products, Advanced Materials, Textile Effects, and Pigments and Additives. Its Polyurethanes, Performance Products, Advanced Materials and Textile Effects segments produce differentiated organic chemical products and its Pigments and Additives segment produces inorganic chemical products. The Company’s products are used in a range of applications, including those in the adhesives, aerospace, automotive, construction products, personal care and hygiene, durable and non-durable consumer products, digital inks, electronics, medical, packaging, paints and coatings, power generation, refining, synthetic fiber, textile chemicals and dye industries. HUN’s current market cap is $6 billion.

Earnings and Sales Growth: Over the last twelve months, earnings increased 48.84%, while revenues grew by 16.7%. In the last quarter, earnings were 7.56% higher while revenues declined by -1.13%. HUN’s operating profile improved through most of this year, but appears to be experiencing some deterioration as of the most recent earnings report. In the last year, Net Income was 13.45% of Revenues, but weakened to 9.65% in the last quarter.

Free Cash Flow: HUN’s free cash flow is $986 million. This marks an improvement over the last year, when Free Cash Flow was $73 million, and $741 million in the last quarter. The current number translates to a useful Free Cash Flow Yield of 16.34%. It is also noteworthy that HUN’s Free Cash Flow saw a peak at $1.2 billion in June 2018, and has declined from that point, but the turn over the last year from negative territory, along with healthy liquidity provides a useful counter to the current Net Income pattern and could signal that the company has successfully navigated that storm.

Debt to Equity: HUN has a debt/equity ratio of .35. This is a conservative number that has also decreased since the beginning of 2020 from .77. HUN’s balance sheet shows that total cash in the last quarter was about $608 million (down from $1.04 billion six months ago), while long-term debt is $1.5 billion. Debt service is not a concern given the company’s healthy Free Cash Flow and a balance sheet that remains healthy even with its drop in the last couple of quarters.

Dividend: HUN pays an annual dividend of $.85 per share, which translates to an annual yield of about 2.84% at the stock’s current price. It is also worth noting that management increased the dividend at the beginning of the year\, from $.75 per share, and from $.65 per share earlier in 2021.

Price/Book Ratio: there are a lot of ways to measure how much a stock should be worth; but I like to work with a combination of Price/Book and Price/Cash Flow analysis. Together, these measurements provide a long-term, fair value target at around $42 per share. That suggests that at its current price, the stock is undervalued by about 41%.

Technical Profile

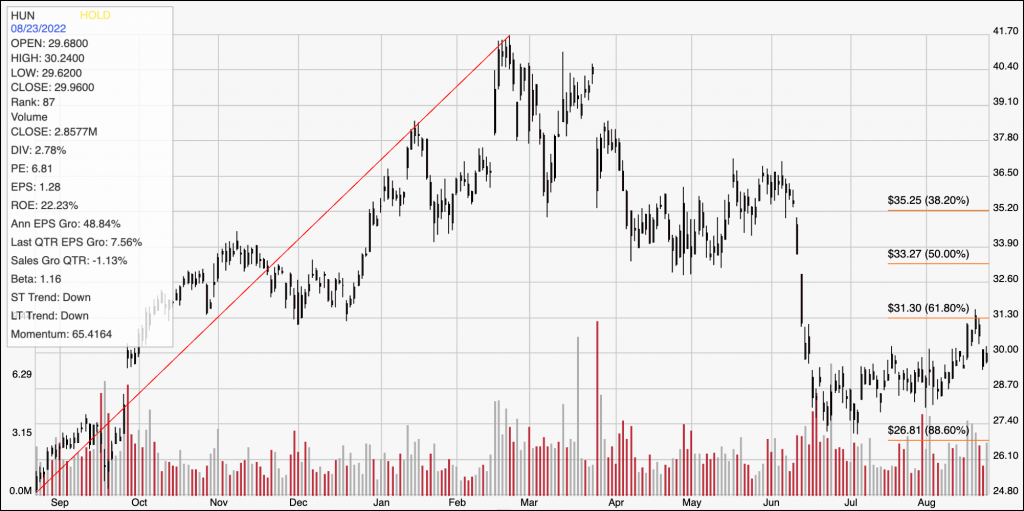

Here’s a look at the stock’s latest technical chart.

Current Price Action/Trends and Pivots: The diagonal red line on the chart above traces the stock’s upward trend from a low at around $25 a year ago to its high point around $42 in February. It also provides the baseline for the Fibonacci retracement lines shown on the right side of the chart. The stock hit its latest high, and immediate resistance at around $31 at the end of last week, which also coincides with the 61.8% retracement line. Current support is around $29, based on pivot lows throughout July and the start of this month around that level. A drop below $29 could see the stock drop to a little below $27, where the stock’s lows in June provided the launching point for the stock’s stabilization since then. A drop below $27 should see the stock retest its yearly low at around $25. A push above $31 could see the stock rally to about $34 before finding next resistance at pivot low levels seen in April and May.

Near-term Keys: HUN’s appears to be building bullish momentum, which could mean that if you prefer to focus on short-term trading strategies, a push above $31 could offer a signal to buy the stock or work with call options, with $34 offering an attractive profit target. A drop below $29 could be a signal to consider shorting the stock or buying put options, using $27 as a useful initial profit target on a bearish trade and $25 possible if selling activity increases. The company’s fundamentals support HUN as an interesting value at its current price. If you’re willing to accept the potential for continued, high volatility in the market right now, this could be an interesting long-term opportunity.