One of the challenges for any investor, no matter what method they prefer to use, is how to find new, useful opportunities to put their money to work. In that effort, one area that I think most investors don’t think about is investing in the companies that make access to the markets possible.

I like to keep an eye on the Financial sector, especially as they relate to the ebb and flow of economic activity, and so also of interest rates. Beyond the investment banks, brokerage houses, and mutual fund companies that I think most of us associate with the Financial sector, however are the companies that manage financial exchanges, track and provide access to all kinds of financial data (on individual companies as well as on the broad market itself).

Nasdaq Inc. (NDAQ) is an excellent example of what I mean; if you track the markets at all, you’ve heard of the NASDAQ and know that it is one of the biggest exchanges in the United States, but you probably didn’t know that for the company that operates that exchanges, trading and clearing are just a part of what its overall business does. One of the areas that the company has been putting a lot of recent investment and focus, for example, is on its Investment Intelligence segment, which provides market and index data and analytics for financial institutions. This is an area that operates primarily as a subscription-based service, which provides a high-margin stable operating base as well as some of the company’s best long-term growth opportunities. Another growth area is in the company’s fraud and anti-money laundering solutions, which NDAQ strengthened by acquiring Verafin, a leading anti financial crime technology provider, in early 2021.

The company’s fundamental strengths include strengthening free cash flow and health operating margins. Those strengths appear to have given the company a useful headwind that has allowed it to diverge from the broad market since late May of this year, rising from a yearly low at around $46.50 to its current price at around $58 per share. Are those strengths also enough to make the stock a useful value at its current price? Let’s find out.

Fundamental and Value Profile

Nasdaq, Inc. is a global technology company. The Company manages, operates, and provides its products and services in four business segments, including Market Technology, Investment Intelligence, Corporate Platforms, and Market Services. Its Market Technology segment is a global technology solutions provider and partner to exchanges, clearing organizations, central securities depositories, regulators, banks, brokers, buy-side firms, and corporate businesses. The Investment Intelligence segment includes its market data, index, and analytics businesses. The Corporate Platforms segment includes its listing services, and investor relations and environmental, social and governance (IR & ESG) services businesses. The Market Services segment includes its equity derivative trading and clearing, cash equity trading, fixed income and commodities trading and clearing (FICC) and trade management services businesses. It provides broker services, clearing, settlement and central depository services. NDAQ’s market cap is about $29 billion.

Earnings and Sales Growth: Over the last twelve months, earnings increased 14.6%, while sales increased by 14.75%. In the last quarter, earnings shrank by -1.45%, while sales growth was flat, but positive by 0.32%. The company’s margin profile is healthy; over the last twelve months, Net Income was 18.74%, and 18.88% in the most recent quarter.

Free Cash Flow: HRL’s free cash flow was a little over $1.4 billion over the past twelve months and translates to a modest Free Cash Flow Yield of 5.07%. It should be noted that Free Cash Flow increased from $1.13 billion in the last quarter, and $961 million a year ago.

Dividend Yield: NDAQ’s dividend is $.80 per share, and translates to a yield of 1.39% at its current price.

Debt to Equity: NDAQ has a debt/equity ratio of 0.78. This is a conservative number that I think is a little misleading. Their balance sheet shows about $481 million in cash and liquid assets, which declined from about $742 million three quarters ago against $4.5 billion in long-term debt. The company’s decline in liquidity in the face of improving free cash flow and stable operating margins could be a simple reflection of the company’s focus on investing in growth of its Investment Intelligence business.

Price/Book Ratio: there are a lot of ways to measure how much a stock should be worth; but I like to work with a combination of Price/Book and Price/Cash Flow analysis. Together, these measurements provide a long-term, fair value target around $61 per share. That suggests that the stock is only somewhat undervalued right now, with a little over 4% upside from its current price, and with a useful discount price at around $48.50.

Technical Profile

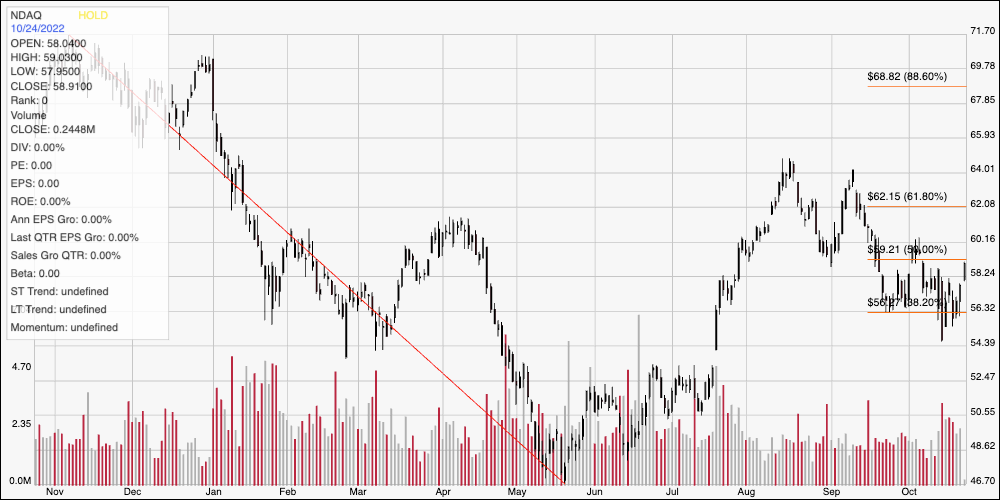

Here’s a look at the stock’s latest technical chart.

Current Price Action/Trends and Pivots: This chart traces the stock’s movement over the last year. The diagonal red line traces the stock’s downward trend from from its high point a year ago at around $72 to its low in May around $46.50. It also acts as the baseline for the Fibonacci retracement lines shown on the right side of the chart. The stock rallied strongly into mid-August, peaking at around $64 before dropping back in the last couple of months to its latest pivot low last week at around $56 where the 38.2% retracement line sits to mark current support. Immediate resistance is around $60, where the stock last peaked early this month. A push above $60 should find next resistance between $62, where the 61.8% retracement can be seen, and $64 where the stock peaked twice, first in August and again in September. A drop below $56 should see limited downside, with next support at around $54 based on pivot low activity seen in February and March as well as last week.

Near-term Keys: NDAQ has some useful fundamental strengths, but also shows a couple of things that are worth paying attention to in the quarters ahead, such as its declining liquidity, for improvement before considering a long-term investment more seriously. The stock’s current price also doesn’t represent a useful value right now, which means that the best probabilities to work with this stock lie in short-term trading opportunities, with particular emphasis on a bullish focus. A push above $60 would be a useful signal to consider buying the stock or working with call options, with $62 to $64 offering reasonable bullish profit targets. While I don’t see a bearish trade as offering reasonable probabilities of success right now, you could use a drop below $56 as a signal to think about shorting the stock or buying put options, with $62 acting as a practical profit target on a bearish trade.