Periods of economic uncertainty breed fear into the markets, which usually translates to increasing volatility and bearish price movements. Bearish market conditions mean that finding conservative, defensively-positioned investment opportunities can get harder to do.

Defensive stocks generally mean looking for industries where revenues aren’t closely correlated with the ebb and flow of economic progress. That boils down to finding companies that produce predictable revenue streams, even while consumers are looking for ways to tighten their belts. Food stocks have always been an area I gravitate to that fits this description, and that includes some of the biggest names in the Beverages industry.

Coca-Cola Co (KO) is one of the most recognized brand names in the entire world. They’re so ubiquitous, in fact that for many the word “Coke” doesn’t actually refer to Coca-Cola itself, but to soda in general. That is just one of the reasons that I think KO Is an example of a company that is less sensitive to economic risk, even on a global scale, than many other stocks in the marketplace. Another reason is that, even when the economy turns sour, consumers not only still have to buy food, but they have also proven that there are “indulgences” that they won’t do without. Soda is one of them, and that is why I think the largest stocks in the Beverages industry could be a smart place to think about putting your money to work even as the market remains uncertain and unpredictable. KO also occupies an interesting place in its market, as the soft drink maker of choice among most restaurants, theaters, and other public venues.

Safety is one thing; value is another. The stock has seen some volatility over the past year, dropping from an April high at around $67 to a low in October at around $54. since then, the stock has rallied strongly hitting its latest peak at around $64 this month. The company boasts a balance sheet that, not surprisingly, has held up and remained a source of strength throughout the past year and a half. Does that mean that KO could be a smart bet, both from a fundamental and value perspective, or has the stock’s increase in price outpaced its improving fundamental metrics? Let’s dive in.

Fundamental and Value Profile

The Coca-Cola Company is a beverage company. The Company owns or licenses and markets non-alcoholic beverage brands, primarily sparkling beverages and a range of still beverages, such as waters, flavored waters and enhanced waters, juices and juice drinks, ready-to-drink teas and coffees, sports drinks, dairy and energy drinks. The Company’s segments include Europe, Middle East and Africa; Latin America; North America; Asia Pacific; Bottling Investments, and Corporate. The Company owns and markets a range of non-alcoholic sparkling beverage brands, including Coca-Cola, Diet Coke, Fanta and Sprite. The Company owns or licenses and markets over 500 non-alcoholic beverage brands. The Company markets, manufactures and sells beverage concentrates, which are referred to as beverage bases, and syrups, including fountain syrups, and finished sparkling and still beverages. KO has a current market cap of about $277 billion.

Earnings and Sales Growth: Over the last twelve months, earnings increased by 6.15%, while sales improved a little more than 10%. In the last quarter, earnings decreased by -1.43% while sales growth shrank by -2.31%. KO operates with a very healthy margin profile that strengthened in the last quarter; in the last twelve months, Net Income was 23.44% of Revenues and increased to 25.54% in the last quarter.

Free Cash Flow: KO’s Free Cash Flow is healthy, slipped a bit over the past year. Over the last twelve months, the company generated cash flow of $10.1 billion. That marks a decline from a year ago, when Free Cash Flow was about $11.4 billion. The current Free Cash Flow translates to a Free Cash Flow Yield of 3.73% at the stock’s current price.

Debt to Equity: KO has a debt/equity ratio of 1.45, which is a bit high, but not unusual for stocks in the Beverages industry. Their balance sheet shows $13.2 billion in cash and liquid assets versus $35.4 billion in long-term debt. Cash has increased since the third quarter of 2020, from $10.9 billion to its current level. Their operating profile and balance sheet together indicate that KO should have no trouble servicing its debt.

Dividend: KO pays an annual dividend of $1.76 per share, which at its current price translates to a dividend yield of about 2.8%. KO is considered a “Dividend King;” they increased their dividend in 2020 from $1.60 and again at the end of the first quarter of 2021, to its current level at the start of 2022, marking 60 consecutive years of dividend increases. KO has paid a consistent dividend since 1920 and are a member of the S&P Dividend Aristocrats Index.

Price/Book Ratio: there are a lot of ways to measure how much a stock should be worth; but I like to work with a combination of Price/Book and Price/Cash Flow analysis. Together, these measurements provide a long-term, fair value target around $56 per share. That suggest that KO is overvalued, with about -11% downside from its current price, and a useful discount at around $45 per share.

Technical Profile

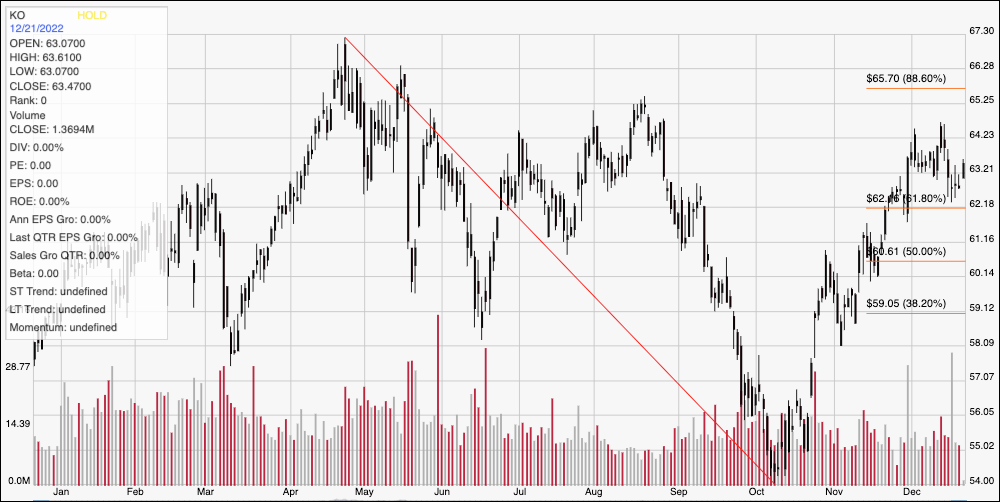

Here’s a look at the stock’s latest technical chart.

Current Price Action/Trends and Pivots: The chart above displays the past year of price activity for KO. The red line traces the stock’s downward trend, from a high in April at $67 to its low in October at around $54. It also provides the baseline for the Fibonacci retracement lines shown on the right side of the chart. The stock has rallied from that low, pushing above all of its major retracement lines to its latest peak at around $64 this month. The stock has current support at around $62, where the 61.8% retracement line sits, with immediate resistance at $64. A push above $64 could see near-term upside to between $66 and the stock’s 52-week high at around $67, depending on the pace of buying activity, while a drop below $62 should find next support at around $61, however an increase in bearish sentiment could push the stock to as low as about $59, which is around the 38.2% retracement line.

Near-term Keys: From a long-term perspective, there really isn’t any way to think of KO as a bargain at its current price. That said, I think there could be some interesting opportunities to take advantage of changes in the stock’s current momentum and trading range with short-term trading strategies. A break above $64 could be an interesting opportunity to take advantage of buying the stock or working with call options with a short-term eye on $66 to $67 as an exit point. Practically speaking the stock would need to drop below $61 to offer a useful bearish signal; in that case, you could consider shorting the stock or buying put options with an eye on the $59 level offering a reasonable, quick-hit profit target on a bearish trade.