One of the big recovery stories over the past year or so has come from the Aerospace industry, which includes commercial airlines. From a disastrous 2020, and the first part of 2021, this is a sector that was radioactive not so long ago.

The “reopening” theme that became a part of market commentary in the second half of 2021 meant looking for pockets of the economy where the relaxation of pandemic-driven restrictions would translate to useful increases in economic activity. A lot of economists and analysts have been pointing at this industry as one to watch for the better part of the past eighteen months, since many were predicting a recovery in travel demand as consumers started to exercise long-pent-up desires to get out, take vacations, and see family and friends.

There are two principle commercial airline producers in the world, which is where a proper examination of the Airline industry should start. Those companies are Boeing and Airbus. Both of these producers rely on production of engines and other components from a variety of suppliers to assemble their products, which is why what is good for these companies is also good for the industry. A boost in travel demand in 2021 and 2022 paved the way for both of these companies to ramp up their own production, and by extension increase their orders from their respective suppliers. That’s a positive – but headwinds also exist, like all other sectors of the market, for this industry in the form of inflation and all of its resulting effects.

The market volatility of the past year has been characterized by inflation coming from multiple elements of the global economy, the reality of rising interest rates, and questions about how long the Fed will maintain the aggressive pace it has been following for the past year. Those are current issues that can’t be dismissed, but being a contrarian by nature often means looking past today’s pressures and thinking about much longer-term trends. That normally means that industries that have been out of favor, but look like they could be in position to recover, start to naturally look a bit more attractive, especially in the long term. Many of the most well-known, commercial airlines in the Aerospace industry were hammered by the collapse in consumer and business travel, with modest gains since the second half of 2021, and indications in 2022 and continuing into this year that demand is beginning to approach pre-pandemic levels. That is a significant tailwind that I think could help some of Airbus and Boeing’s suppliers thrive. Raytheon Technologies Corp. (RTX) is an example.

In the commercial airline segment, RTX’s biggest customer isn’t Boeing – it’s Airbus, which before COVID-19 became a global issue was drawing a number of Boeing customers to its business in the wake of the MAX grounding. RTX is also a major player in the government-funded Defense space, which has historically proven to be resilient and even resistant to economic downturns. The pandemic proved the value of RTX’s Defense business, as 2021’s earnings reports demonstrated that segment provided a backstop for the entire company, putting it in position to recover more quickly than other companies whose businesses are closely tied to Boeing.

Strength in their Defense business didn’t completely offset Commercial travel losses in 2020, but they did nonetheless help their balance sheet absorb the hit better than a lot of other businesses, in this industry and others. The company also completed a merger in April of 2020 with Raytheon, which increased its defense and intelligence business to nearly 60% of annual revenues. That gave RTX a backstop of revenue and cash flow that has enabled it to exercise patience with its commercial business, and that most other companies in the industry probably don’t have. I also believe another likely, long-term tailwind lies in the ongoing, grim reality of the war in Ukraine. Regardless of the eventual outcome of that conflict, I expect tension between Russia and the West to remain higher than it has been in a generation, which also implies that military spending will increase, for the U.S. and other NATO nations. Current, multinational efforts to help Ukraine build up its infantry and air defenses are good examples.

While RTX largely underperformed in 2022, falling from an April high at around $106 to about $81 in September, the stock rallied strongly into the end of the year, peaking at around $102. From that point, the stock has mostly settled into a consolidation range that I think will define the stock’s next significant trend. Are the company’s fundamentals still strong enough to make the stock a useful value at its current price, or more risky than it’s worth? Let’s find out.

Fundamental and Value Profile

Raytheon Technologies Corp, formerly, United Technologies Corporation is engaged in providing high technology products and services to the building systems and aerospace industries around the world. The Company operates through segments such as Pratt & Whitney and Collins Aerospace Systems. The Pratt & Whitney segment supplies aircraft engines for the commercial, military, business jet and general aviation markets. Pratt & Whitney segment provides fleet management services and aftermarket maintenance, repair and overhaul services. The Collins Aerospace Systems segment provides aerospace products and aftermarket service solutions for aircraft manufacturers, airlines, regional, business and general aviation markets, military, space and undersea operations. RTX has a current market cap of $144.5 billion.

Earnings and Sales Growth: Over the last twelve months, earnings increased by about 17.6%, while sales were 6.15% higher. In the last quarter, earnings grew by almost 5% while Revenues were 6.75% higher. RTX’s Net Income versus Revenue over the last year was 7.75%, and 7.86% in the last quarter.

Free Cash Flow: RTX’s Free Cash Flow is modest, but showing useful signs of improvement. In the last quarter, free cash flow was almost $4.9 billion versus $4.7 billion a year ago, and $3.3 billion in the last quarter. In the quarter prior, this number was about $4.55 billion. The current free cash flow number translates to a Free Cash Flow Yield of 3.32%.

Debt to Equity: RTX has a debt/equity ratio of .41, which is very conservative, and marks a drop from 1.03 in the first quarter of 2020. Their balance sheet shows about $6.2 billion (versus $5.4 billion in the last quarter) in cash and liquid assets against $30.7 billion in long-term debt (versus $45.3 billion at the end of the first quarter of 2020). Servicing their debt is no problem.

Dividend: RTX pays an annual dividend of $2.20 per share, which at its current price translates to a yield of 2.2%. It should be noted that early in 2020, management announced it was reducing the dividend from $2.94 to $1.90 per share, a cost-cutting measure that can be interpreted as positive or negative depending on your general view. Management raised the dividend in 2021 to $2.04, and then again to its current level at the beginning of 2022, which I take as a sign of increasing confidence and strength.

Price/Book Ratio: there are a lot of ways to measure how much a stock should be worth; but I like to work with a combination of Price/Book and Price/Cash Flow analysis. Together, these measurements provide a long-term, fair value target around $94.50 per share, which suggests that the stock is slightly overvalued at its current price, by about -4%, with a useful discount price at around $75.50.

Technical Profile

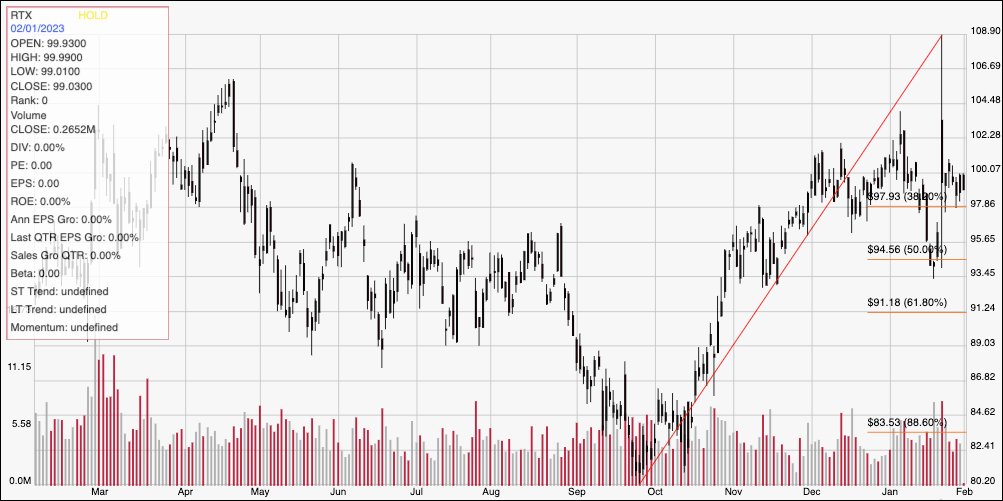

Here’s a look at the stock’s latest technical chart.

Current Price Action/Trends and Pivots: The red diagonal line follows the stock’s upward trend from its September of last year to its high last month at around $109. It also provides the baseline for the Fibonacci retracement lines on the right side of the chart. Aside from a short period of increasing volatility at the beginning of the year, the stock has been holding in a sideways patter since early December, with current support sitting at around $98 and immediate resistance at about $102. A push above $102 should find next resistance at about $106, based on a peak in April of last year, with additional room to test the 52-week high at around $109 if buying activity increases. A drop below $98 should find next support at around $95, based on a consolidation period from June to August of last year.

Near-term Keys: RTX’s balance sheet has remained generally solid throughout the past year, and even some seen some useful improvements in the last quarter. Despite those positives, the stock’s current price does mark it as an overvalued stock right now. If you prefer to focus on short-term trading strategies, a drop below $98 could be a good signal to consider shorting the stock or buying put options, using $95 as an practical bearish trade target, while a push above $102 could be a good signal to buy the stock or work with call options, with upside to about $106 on a bullish trade, and possibly $109 if buying momentum accelerates.