Intel Corp (INTC) is a stock that I’ve followed for quite some time, and that I’ve written about in this space quite a bit over the last few months. This is one of the 600-lb gorillas of the Technology sector, after all, and the company that is easily considered the gold standard of companies in the Semiconductor industry. The stock has diverged from the movement of the rest of the Technology through the year, however, and after its latest earnings report at the end of last week has dropped to within just a few dollars of its 52-week, pandemic-induced March low around $43.50.

What gives? The market is concerned about issues in production of its next-gen, 7nm chips, which in July management disclosed would be delayed by at least six months. The company is still working through those delays, and analysts and investors seem to be concerned about sales and growth in its data-center business. That pressure could simply be a reflection of the COVID-19 world we live in, but this is also a heavily competitive segment of the industry, and so there is worry they may be losing market share as well.

Trying to make sense of short-term price moves can be pretty maddening – especially if you’re looking at a stock you bought shares of as it goes down. It’s important to be able to look past the price action of the moment, however and to put a broader context on things. That’s one of the reasons that I put such a big emphasis of value investing.

Years ago as I started to really study the principles behind value investing, I read that Warren Buffett learned his method from a professor at Columbia University names Benjamin Graham. If you Google that name, you’ll find a lot of information about the man who the Oracle of Omaha has frequently called the most influential man in his life aside from his own father. Mr. Graham was a master investor in his own right, who started his career early in the 20th century and had built a very successful money management business in his own right before the Crash of 1929. While he was like most investors in the aftermath of that event and absorbed heavy losses, he and his partner managed to stay in business, and he used the experience to begin formulating the approach that is broadly known as value investing. Along the way, he wrote two books, Security Analysis and The Intelligent Investor, which have never gone out of print and are still considered required reading for any serious student of the principles of successful long-term investing.

The Intelligent Investor is the easiest of the two books to read, which isn’t to say it’s a breeze; after all, Mr. Graham was a professor of finance at Columbia University from 1928 until he retired decades later, and he wrote like an economist and an academic. Even so, since of the two it is also the most pertinent to the underlying principles most value investors adhere to, I invested the time and effort to go through it. That was a transformative experience in my investing career, and something that provided the basis for the investing methods I’ve followed ever since.

One of the most interesting ideas that impacted me was Mr. Graham’s contention that if a company’s business was worth more than its current stock price, it didn’t matter what the stock price was doing now, or even what it did in the immediate future. He didn’t worry about the direction of a stock’s trend, or what the latest news headline said. If the numbers showed the business was stronger than the stock price, it was worth an immediate investment, and the smart investor should be willing to be patient and ride through any and all near-term fluctuations in price the stock may see.

Now back to INTC. Despite the bad headlines and negative momentum the market is giving the stock after its earnings report, the reality is that the company’s fundamental profile remains extremely strong, with a solid balance sheet, healthy Free Cash Flow, and operating margins that also remain healthy. There are indications that 2020 has had an impact on these measurements, and those certainly bear watching. I’m not dismissive of concerns about their production problems, but I also respect management’s willingness to take time to determine what their best options are to deal with those issues, no matter how much the market might punish them for it.

Even before I started my career as a value investor, I spent some time working in the Semiconductor industry with a small engineering firm that relied on chips from INTC’s competitors for our finished products. I spent time at trade conventions talking to people in that business, and at the time we all felt like it was us versus the Big, Bad Intel. There was buzz at the time around companies we worked with like AMD and others that were seeing success finding their own niches in the industry, and I admit I got caught up at the time in the idea of being part of the movement to take down the Big Bad. That was a couple of decades ago, and guess what? Most of those companies don’t even exist anymore. Others, like AMD have experienced different levels of success at different periods of time and are still around, and that’s a good thing; but most of those who were betting against INTC have gone the way of the dinosaur.

I think that there is real chance that right now is a similar kind of environment. Yes, INTC is being pressured by intense competition, and they are having to deal with some issues in their own internal processes. Even so, I think that the smart thing as a value-oriented investor is to recognize the deep discount the company offers, and to acknowledge other areas of business INTC is focusing on for the future. A good example is in INTC’s effort to identify the next generation of growth opportunities by investing heavily in cloud processing and storage technology as well as 5G mobile processing. Those investments are expected by most analysts to provide the bulk of their revenue and earnings growth in the foreseeable future. All told, I think INTC remains an incredible value opportunity right now.

Fundamental and Value Profile

Intel Corporation is engaged in designing and manufacturing products and technologies, such as the cloud. The Company’s segments are Client Computing Group (CCG), Data Center Group (DCG), Internet of Things Group (IOTG), Non-Volatile Memory Solutions Group (NSG), Intel Security Group (ISecG), Programmable Solutions Group (PSG), All Other and New Technology Group (NTG). It delivers computer, networking and communications platforms to a set of customers, including original equipment manufacturers (OEMs), original design manufacturers (ODMs), cloud and communications service providers, as well as industrial, communications and automotive equipment manufacturers. It offers platforms to integrate various components and technologies, including a microprocessor and chipset, a stand-alone System-on-Chip (SoC), or a multichip package. The CCG operating segment includes platforms that integrates in notebook, two in one systems, desktop computers for consumers and businesses, tablets, and phones. INTC’s current market cap is about $190.1 billion.

Earnings and Sales Growth: Over the last twelve months, earnings declined about -21% while sales slipped by about -4.5%. In the last quarter, earnings decreased a little over -9.75%, while sales were -7% lower. Despite the challenges already described, INTC operates with a very healthy margin profile; Net Income versus Revenues over the past year was more than 28%, and narrowed in the last quarter to a 23.32%. Both of those measurements have slipped since earlier this year, and that is something to watch. I think it is reflective of the internal difficulties they have dealt with along with the impact of COVID-driven declines in its data center business. Even so, their operating profile gives INTC a lot of flexibility and remains a source of strength.

Free Cash Flow: INTC’s free cash flow is healthy; in the last quarter, it came in at $20.3 billion a little lower than the $21.9 billion of the quarter, prior, but still significantly above the $13.6 billion of a year ago and about $12.5 billion at the end of the first quarter of 2019. That translates to a Free Cash Flow Yield of about 8.87%. The percentage is attractive, but the size of the actual number is a reflection of the company’s operating strength, which should serve it well even if broad economic uncertainty and concern about its data center business and 7nm production continues.

Debt to Equity: INTC has a debt/equity ratio of .44. This is a conservative number. The company’s balance sheet indicates that operating profits are adequate to service their debt, with $18.2 billion in cash and liquid assets (down from $25.8 billion in the last quarter, but still healthy) versus $36 billion in long-term debt. They have a lot of debt, but with a healthy operating margin profile along with a sizable cash position, servicing their debt shouldn’t be a problem.

Dividend: INTC pays an annual dividend of $1.32 per share, which translates to a yield of 2.74% at the stock’s current price.

Price/Book Ratio: there are a lot of ways to measure how much a stock should be worth; but I like to work with a combination of Price/Book and Price/Cash Flow analysis. Together, these measurements provide a long-term, fair value target around $71 per share. That means that INTC is trading at a 52% discount right now, which makes the stock very interesting.

Technical Profile

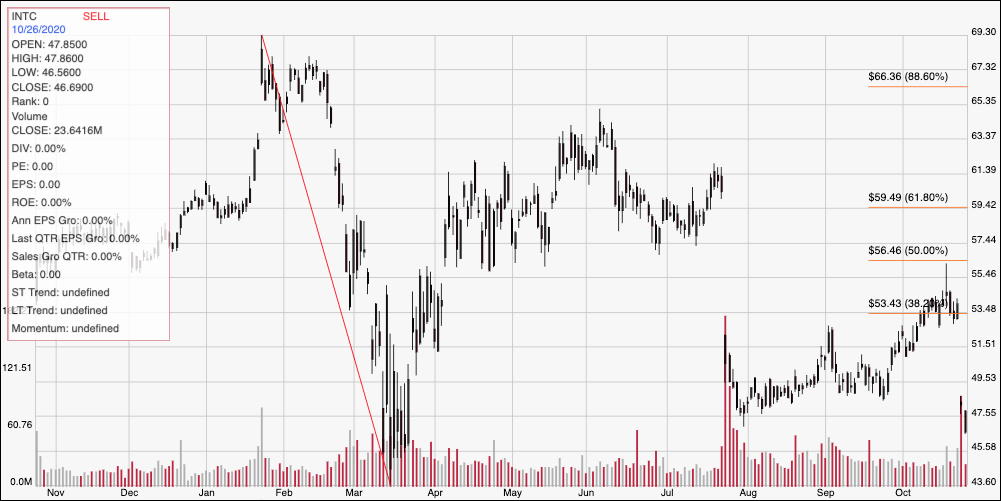

Here’s a look at the stock’s latest technical chart.

Current Price Action/Trends and Pivots: The chart above displays the last year of price activity for INTC. The red diagonal line traces the stock’s drop to a bear market low in March at around $44; it also provides the baseline for the Fibonacci retracement line on the right side of the chart. After following the sector to a nice peak at around $63 in June, the stock gapped back down at the end of July to a low at around $47 following an earnings report the market didn’t take favorably. After climbing back to a high a little below the 38.2% retracement line around $53.50 earlier this month, the stock gapped back down again on Friday after the last earnings report, and is how sitting at around $47. Immediate resistance is around $48 based on the stock’s July low, while a real break above resistance would take a move to about $50. Immediate support could sit anywhere between $45.50 and the stock’s 52-week low around $43.50. A move above $50 should see short-term momentum peak around the 38.2% retracement line at $53.50, while a drop below $45.50 should generally see strong next support between $43 and $43.50 based on pivot lows in that area throughout 2018 and 2019.

Near-term Keys: The narrow ranges between the stock’s support and resistance levels could offer some useful trading opportunities – provided you’re willing to work with quick profits rather than attempting to maximize the stock’s trends. If the stock pushes above $50, consider buying the stock or working with call options, using $53 to $53.50 as a bullish exit target. A drop below $45.50 would be a strong signal to think about shorting the stock or buying put options, with $43.50 to $43 acting as a good profit target on a bearish trade. What about the stock’s value proposition? The company’s solid fundamental profile, with a still very healthy balance sheet, combined with its historical price discount are more than enough to fit Benjamin Graham’s value definition, and I think provide a strong argument to consider taking a new position at the current price. If you’ve purchase shares in the company any any point in the last few months, I also think the opportunity is more than good enough to keep holding on.