(Bloomberg) — Henry Kaufman is one of the rare Wall Street veterans who can authoritatively draw parallels between the inflation scare of the 1970s and today’s alarming run-up in prices. And he has zero confidence Chair Jerome Powell’s Federal Reserve is ready for the battle it now faces.

Kaufman decades ago was the celebrated chief economist at Salomon Brothers nicknamed “Dr. Doom.” He correctly anticipated the era’s crippling inflation and approved when then-Fed Chairman Paul Volcker delivered the so-called Saturday Night Special, a radical — and unexpected — tightening of monetary policy on an October weekend in 1979.

To Kaufman, Powell is no Volcker. Not even close.

“I don’t think this Federal Reserve and this leadership has the stamina to act decisively. They’ll act incrementally,” Kaufman, 94, said in a phone interview. “In order to turn the market around to a more non-inflationary attitude, you have to shock the market. You can’t raise interest rates bit-by-bit.”

Powell this week told lawmakers in congressional testimony that there’s a “long road” toward getting Fed policy to a “normal” setting — suggesting more aggressive action isn’t needed to pull down inflation. Powell said the planned withdrawal of stimulus “should not have negative effects on the employment rate” — a big contrast with the Volcker-era tightening that contributed to a surge in joblessness.

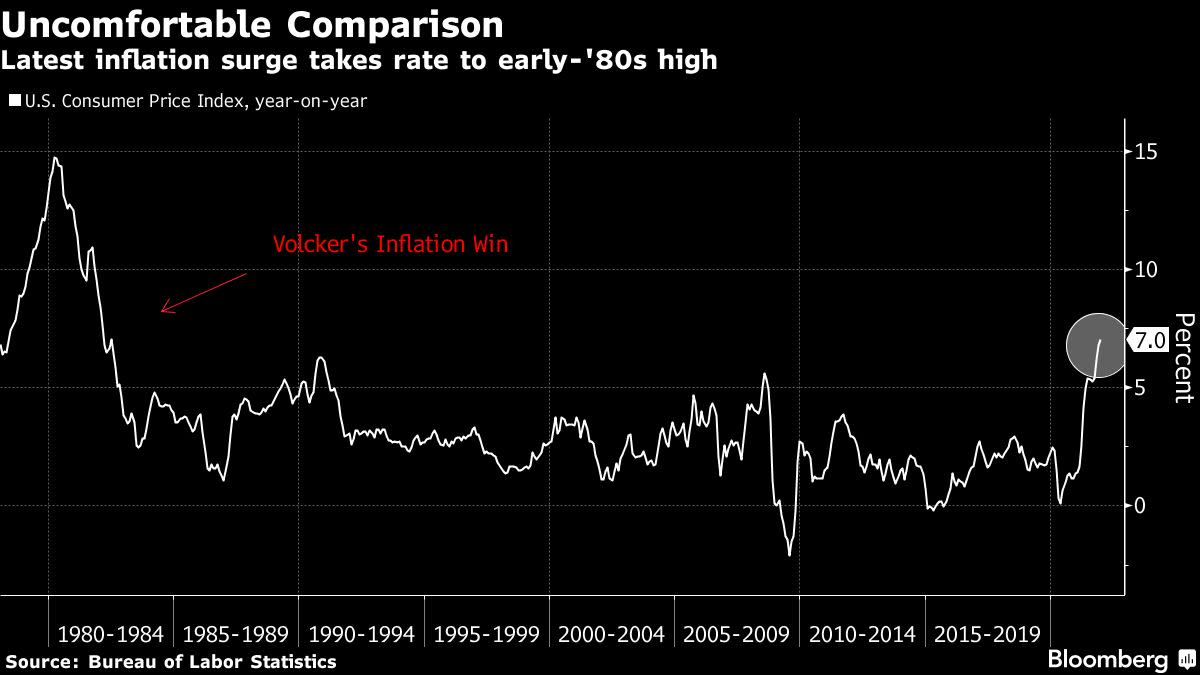

A more serious pledge to tame inflation would require the Fed going much further, Kaufman said. Volcker’s 1979 decision to restrict the supply of money drove short-term rates to excruciating levels but, eventually, also crushed inflation. Prices, rising at an annual 14.8% in March 1980, were ticking up at just 2.5% a year by July 1983. Volcker emerged a hero.

“It requited a lot of fortitude in 1979 to do what the Fed did,” Kaufman said.

Now, inflation is again roaring back. From an average of 1.7% in the 10 years through 2020 — below the Fed’s 2% objective — it jumped to a four-decade high of 7% last month.

If he were advising Powell, Kaufman said he’d urge the Fed chair to be “draconian,” starting with an immediate 50-basis point increase in short-term rates and explicitly signaling more to come. Plus, the central bank would have to commit in writing to doing whatever is necessary to stop prices from spiraling higher.

Out-of-Consensus

That’s a stark contrast with market and economist expectations for the Fed to wait until March to start boosting its key rate, and then only by a quarter point.

Even with several doses of strong medicine, it would take at least a year for inflation to moderate to 3%, Kaufman said. The median forecast of economists surveyed by Bloomberg is for consumer prices to rise by less than 3% by year-end,

“The longer the Fed takes to tackle a high rate of inflation, the more inflationary psychology is embedded in the private sector — and the more it will have to shock the system,” Kaufman said.

Kaufman was born in Germany during the Weimar Republic and fled the Nazi regime in 1937. He earned a PhD in banking and finance at New York University, worked for the Fed as an economist and then, over a quarter century at Salomon, became Wall Street’s authority on the bond market and monetary policy.

Big Call

He was called “Dr. Doom” for his bearish views and his criticism of government policy. But in 1982, Kaufman famously predicted that interest rates would fall — triggering a historic rally in stocks and ushering in the bull market.

Today, he’s hardly alone in calling for faster rate hikes. Others including former Treasury Secretary Lawrence Summers have said recently that the Fed is underestimating the challenge of bringing inflation under control.

Kaufman’s perspective is distinguished by his being one of the few of the people who held senior roles on Wall Street in the late 1970s and is still closely studying the markets. Another such veteran is Byron Wien, Blackstone Inc.’s 88-year-old vice chairman of private wealth solutions. In his annual “Ten Surprises” note, posted this month, Wien and his colleague Joe Zidle predicted that “persistent inflation becomes the dominant theme,” the Fed is forced to raise rates four times in 2022 and the 10-year Treasury yield climbs to 2.75%.

In Kaufman’s view, Powell made two key errors as Fed chief over the course of 2021. The first was attributing some inflation to direct and indirect effects of the Covid-19 pandemic, something he said is “impossible to measure” and thus unknowable with any precision. The second was calling it transitory.

‘Dangerous’ Signal

“It’s dangerous to use the word transitory,” Kaufman said. “The minute you say transitory, it means you’re willing to tolerate some inflation.”

That, he said, undermines the Fed’s role of maintaining economic and financial stability to achieve “reasonable non-inflationary growth.”

Powell told Congress in late November he would drop transitory from the Fed’s lexicon. By then, inflation had already reached 6.2% and some economists were scoffing at his continued use of the term.

While Kaufman sees many reasons to draw lessons from the Fed’s experience in the 1970s, much is different now. For starters, the economy is booming, the unemployment rate is under 4% and stock indexes are close to records.

Less Drastic

In early 1980, even after Volcker’s policy move, prices were still rising so fast that Kaufman, at a bankers’ meeting in Los Angeles, called for the declaration of a national inflation emergency as well as temporary wage freezes and price controls. Today’s situation doesn’t warrant the same degree of alarm, he says.

“That’s when prices reach levels where the average American realizes income is inadequate to cover inflation and that puts pressure on household spending and consumption,” he said. “It’s too early in the game.”

©2022 Bloomberg L.P.