Cisco Systems Inc. (CSCO) is one of the most recognizable and established companies in the Technology sector. With a market cap of about $200 billion, they are also one of the largest, if not THE largest player in the Networking & Communications segment. They are, without question, the standard that all other networking businesses are measured and compete against. No matter whether you’re talking about wired or wireless networking, CSCO is one of the companies that not only developed the standards and infrastructure the entire Internet is built on today, but that continues to lead the way into the future, including cloud-based computing and the next generation of technology in the so-called “Internet of Things” (IoT).

It’s ironic, perhaps that despite CSCO’s unquestioned dominance in its industry, the stock has mostly languished for nearly two decades. After riding the “dot-com boom” of the late 1990’s to a peak at around $80 per share, the stock cratered when that boom went bust, dropping to as low as about $8 in late 2002. From that point it never rose higher than into the low $30 range – at least not until the latter part of 2017, when the stock finally broke that top-end resistance. That pushed the stock to a high in May a little above $46 per share as Tech stocks generally prospered. 2019 started off pretty well for investors in the stock, as well; the stock increased about 30% from its late December 2018 low around $40 per share, and hit a new multi-year high a little above $58 in mid-July.

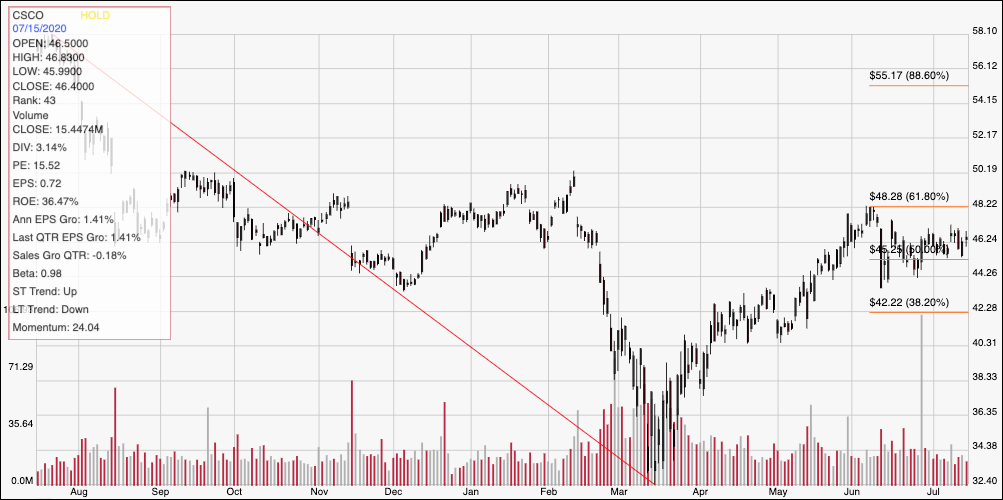

From that point, trade concerns in the latter part of 2019, followed by the COVID-19 that propelled the entire market into the first legitimate bear market in more than a decade pushed the stock all the way to a multiyear low at around $32 in mid-March. From that point, the stock picked up some useful bullish momentum, forming a nice short-term upward trend that saw the stock peak at around $48 in early June. Over the last six weeks CSCO has started to hover in a range a little off of that $48 peak. Despite a strong fundamental profile, CSCO doesn’t really qualify as a good bargain under my normal definition of value; but current conditions do make an interesting case that it might be worth paying attention right now anyway.

For massive portions of corporate America, COVID-19 has meant sending white-collars workers home and setting up various telecommuting solutions to keep business going. That’s given an intriguing rise to companies that are getting quite a bit of buzz in the media as new, hip players in what I think will actually translate to a long-term, fundamental shift in the way business is done all over the world, even after the pandemic has eased and economic activity has resumed previous levels. While they may not be getting a lot of that media-generated buzz, the truth is that CSCO has been providing solutions and services for exactly this kind of condition for more than two decades, from Wide Area Networking to teleconferencing and more. CSCO is also a big player in the 5G world, which represents the next stage in remote connectivity in ways that we are really only beginning to appreciate. Those are reasons that I think CSCO’s current price could offer a very interesting opportunity for a patient, long-term investor right now.

Fundamental and Value Profile

Cisco Systems, Inc. (CSCO) designs and sells a range of products, provides services and delivers integrated solutions to develop and connect networks around the world. The Company operates through three geographic segments: Americas; Europe, the Middle East and Africa (EMEA), and Asia Pacific, Japan and China (APJC). The Company groups its products and technologies into various categories, such as Switching; Next-Generation Network (NGN) Routing; Collaboration; Data Center; Wireless; Service Provider Video; Security, and Other Products. In addition to its product offerings, the Company provides a range of service offerings, including technical support services and advanced services. The Company delivers its technology and services to its customers as solutions for their priorities, including cloud, video, mobility, security, collaboration and analytics. The Company serves customers, including businesses of all sizes, public institutions, governments and service providers. CSCO has a market cap of $195.9 billion.

Earnings and Sales Growth: Over the last twelve months, earnings grew by 1.41%, while sales declined roughly -7.5%. In the most recent quarter, earnings grew 1.41% while sales dropped -0.18%. CSCO has a very healthy operating profile, with Net Income running at 21.32% of Revenues over the last twelve months. That number increased in the last quarter to 23.15%, which is a good sign that the company’s profitability remains on very strong footing.

Free Cash Flow: CSCO’s free cash flow over the last twelve months is nearly $15 billion. This is a number that the company has historically managed to maintain at very healthy levels and translates to a Free Cash Flow Yield of 7.74%.

Debt to Equity: CSCO has a conservative, manageable debt-to-equity ratio of .32. CSCO’s balance sheet shows more than $28.5 billion in cash and liquid assets versus about $11.5 billion in long-term debt. Servicing their debt is not a concern, and liquidity to pursue additional expansion or return value to shareholders via stock buyback or increased dividends is excellent.

Dividend: CSCO currently pays an annual dividend of $1.44 per share, which translates to an annual yield of about 3.1% at the stock’s current price.

Price/Book Ratio: there are a lot of ways to measure how much a stock should be worth; but I like to work with a combination of Price/Book and Price/Cash Flow analysis. Together, these measurements provide a long-term, fair value target around $39.50 per share. That means that CSCO is overvalued by about -15%.

Technical Profile

Here’s a look at the stock’s latest technical chart.

Current Price Action/Trends and Pivots: The diagonal red line traces the stock’s downward trend from July 2019 to its low point in March of this year. It also provides the baseline for the Fibonacci retracement lines shown on the right side of the chart. The stock built a nice short-term upward trend from that bottom, and began to consolidate in June, with resistance right around $48 where the 61.8% retracement line sits and support back in line with the 50% retracement line around $45. A drop below $45 should see the stock fall to around $42 where the 38.2% lies in wait, while a push above $48 could give the stock enough momentum to begin pushing towards its July 2019 highs in the mid-$50 range.

Near-term Keys: If the stock breaks above $48, you could have a good short-term opportunity to buy the stock or work with call options, with an initial profit target sitting at around $50 back around the stock’s February, pre-pandemic swing high, and more room above that point if bullish momentum can keep building. A drop below $45 would mark a good signal to think about shorting the stock or to buy put options, using an initial target price at $42, with next support probably around $40 if bearish momentum accelerates. Based on my traditional metrics, I can’t call CSCO a solid value right now; but I do think there are a number of other elements – continued work-at-home adoption, 5G implementation over the next year or so – that aren’t being factored into my value analysis because of their forward-looking nature. Those are elements that could provide enough of a tailwind to CSCO’s business to make this an exception to the normal value-based argument.