If you think strictly about price performance and what the price of a stock is now relative to where it was in the past – in particular, relative to where it was on a pre-pandemic basis – it’s pretty easy to understand why so much attention is being paid to Tech stocks that make remote work, collaboration and e-commerce possible. That shift is clearly one of the reasons a lot of companies have managed to survive the turbulent conditions of the past few months. It makes for great headlines, and it is something that I believe will be part of the historical commentary about 2020 and COVID-19.

What tends to generate less buzz in market news and other media outlets is another trend that I think is also very important and has a few different interesting layers to it. Stay-at-home orders, shuttered restaurants (which even now are still operating at only partial capacity, if they are operating at all) and broad retail closures naturally prompted consumers to stockpile food and household goods. Some analysts thought that would be a short-term trend; but the longer the pandemic lasts, the more likely this trend is to last, and I believe to stick even beyond the eventual end of the health crisis. Why? Simply because the longer consumers have to rely on cooking and eating at home, for example, the more likely that behavior is to become ingrained – creating what analysts like to call stickiness about demand trends. That doesn’t mean we as consumers don’t, or won’t appreciate the opportunity to go out and enjoy the socialization associated with restaurants, theaters, and so on. Even so, I think food-at-home is something that will stick as a natural behavior for fiscally conservative families – and the longer the pandemic persists, the more young couples are going to have to be fiscally conservative.

Another element of the food-at-home trend relates to pets. Pet food is a highly competitive segment of the Food Products industry, but something that analysts like to see as part of a diversified company portfolio. A secondary increase in demand in pet food is likely to see very healthy stickiness because of increased pet purchases and adoptions this year. Makes sense, doesn’t it? Being forced to stay at home, which earlier this year included having parents with young children begin schooling at home, means that the support offered by a cuddly puppy or kitty becomes more compelling – especially if you do have kids. That means that the Food Products companies that have pet food and pet products as part of their business portfolio have a useful second leg to keep revenues healthy on a long-term basis.

For me, Consumer Staples have always made a lot of sense in these kinds of circumstances. While these kinds of stocks aren’t immune from market momentum, and can certainly turn lower with the rest of the market, they also typically display lower volatility characteristics than the most buzz-worthy stocks. General Mills, Inc. (GIS) is a stock that I’ve followed quite some time, and even used on a few different occasions over the last couple of years in my value-based, income-oriented investments. Its usefulness as a defensive position has been proven out this year, as the stock dropped only about -10% during the initial broad market push to bear market levels, but then pushed more than 22% above its pre-pandemic highs by the beginning of August. Broad market uncertainty pushed the stock down from a 52-week high around $66 to a low in mid-September at around $57, but in the last week the stock appears to be building new bullish momentum. Does the stock still have room to go higher, and is there a fundamental, value-based argument to be made for GIS despite its useful performance year to date? Let’s find out.

Fundamental and Value Profile

General Mills, Inc., is a manufacturer and marketer of branded consumer foods and pet food products sold through retail stores. The Company is a supplier of branded and unbranded consumer food products to the North American foodservice and commercial baking industries. It also provides pet food products through its subsidiary Blue Buffalo Pet Products Inc. The Company has four segments: U.S. Retail, International, Pet operating, and Convenience Stores and Foodservice. The Company offers a range of food products with a focus on categories, including ready-to-eat cereal; convenient meals, including meal kits, ethnic meals, pizza, soup, side dish mixes, frozen breakfast and frozen entrees; snacks, including grain, nutrition bars and frozen hot snacks; yogurt, and super-premium ice cream. The Company’s other product categories include baking mixes and ingredients, and refrigerated and frozen dough. It also provides food products for dogs and cats. GIS’s current market cap is $37.6 billion.

Earnings and Sales Growth: Over the last twelve months, earnings increased about 26.5%, while revenues improved 9%. In the last quarter, earnings and sales both declined; earnings dropped -9%, while sales were -13% lower. GIS operates with a healthy, improving margin profile; over the last twelve months, Net Income was 12.13% of Revenues, and strengthened in the last quarter to 14.64%.

Free Cash Flow: GIS’s free cash flow is modest, at about $466.9 million, and translates to a Free Cash Flow Yield of 1.33%. This marks a significant decline from the quarter prior, when Free Cash Flow was $1.3 billion, but is marked by the reality of increased costs related to health and safety measures along with increased reliance on external, third-party manufacturing resources to meet demand. This is a concern, but not likely to persist as a long-term headwind.

Dividend Yield: GIS’s dividend is $2.04 per share, and translates to an annual yield of about 3.31% at the stock’s current price. It is also worth noting the company increased their dividend earlier this year from $1.96 per share.

Debt to Equity: GIS has a debt/equity ratio of 1.24. This is a high number, and is indicative in part of the debt the company assumed to complete the acquisition of Blue Buffalo Pet Foods in 2018. Their balance sheet shows liquidity, which had weakened through most of 2019, is improving measurably; in the last quarter, cash and liquid assets were nearly $1.8 billion. This number was about $532.7 million at the beginning of 2019 and $626 million in February before the pandemic began. They also currently have $10.8 billion of long-term debt. The company’s margin profile indicates that they should have no problem servicing their debt.

Price/Book Ratio: there are a lot of ways to measure how much a stock should be worth; but I like to worth with a combination of Price/Book and Price/Cash Flow analysis. Together, these measurements provide a long-term target at about $70.50 per share. That suggests GIS is undervalued by about 15% right now.

Technical Profile

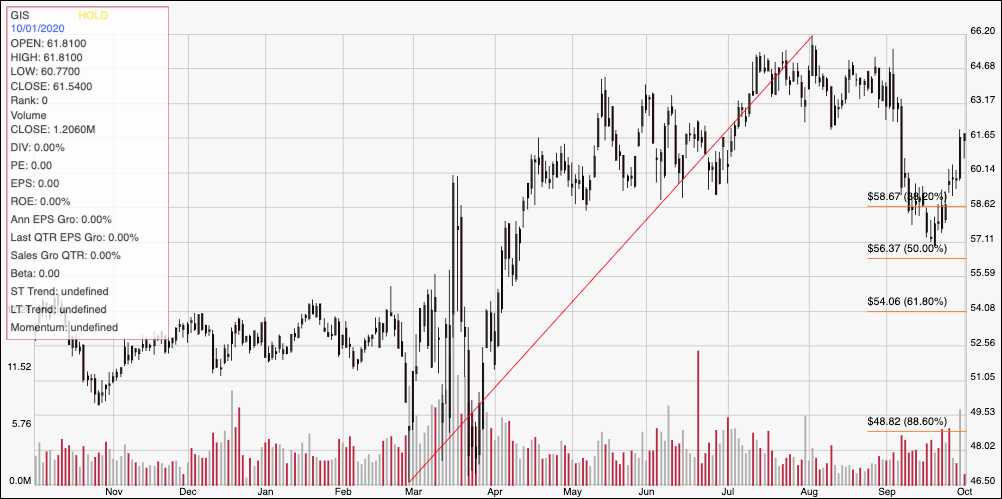

Here’s a look at the stock’s latest technical chart.

Current Price Action/Trends and Pivots: This chart traces the stock’s movement over the last year. The red diagonal line marks the stock’s upward trend from a 52-week low at around $46.50 to its high point at the beginning of August a little above $66; it also provides the baseline for the Fibonacci retracement lines shown on the right side of the chart. In September, the stock dropped back from the mid-$60 range below the 38.2% retracement line, finding support at around $57 before bouncing and starting to move back above that line to its current level. Immediate resistance should be around $63, with support around $60 based on previous pivot activity in that range. A break above $63 should give the stock room to test its 52-week high at around $63, while a drop below $60 may find new support at the 38.2% line which is sitting a little below $59. Continued bearish momentum, however should see the stock test next support between $56 and $57.

Near-term Keys: If you’re looking for a short-term, bullish trade, I think immediate upside in GIS could be limited given current market conditions; however, if the stock does break above $63, it could offer a useful signal to buy the stock or work with call options, with an eye on an exit target at around $66. A drop below support at $59, on the other hand, could offer a useful signal to consider shorting the stock or working with put options, with an eye on the 50% Fibonacci retracement line around $56 as a bearish profit target. The stock’s value proposition is interesting, if not quite compelling, even with the stock’s increase over the course of the year. With a healthy, growing dividend, there is a strong argument to make for using the stock as a useful long-term position.