While a lot of sectors in the market are showing a heightened level of volatility and sensitivity lately, many of them remain up quite nicely year to date, or over the past year. Trade concerns have become more and more heightened lately, spreading volatility throughout the market and pushing the curve between short-term and longer-term Treasury bonds into the second inversion of the past year. That’s a bearish indicator that is putting a lot of investors even more on edge; but that inversion is also being seen in another area of the market that I find interesting. The 30-year Treasury yield on Tuesday dropped below the dividend yield of the S&P 500, implying that if you’re an investor that is looking for a “safe haven” investment that can offer a useful, conservative, and passive income, stocks have one more reason to remain more attractive than bonds.

Dividend stocks have remained a central piece of my evaluation method for years – in fact, they are a basic requirement for my value-oriented investing system. Dividend stocks can be as volatile as any other kind of stock, however the fact that the company pays a regular, consistent dividend can offer a good reason to look for and hang onto fundamentally strong companies even during a bear market. If you can also find a stock that happens to be trading at or near historical lows, you’ll often be able to find yourself on the low end of risk even if the market does actually turn bearish.

Westlake Chemical Corp (WLK) is a company in a sector, Materials, that I think is very interesting, even in current market conditions. The sector is generally sensitive to economic cycles, as are most sectors of the market, but it is also true that many of the stocks in this category – particularly in the Chemicals industry – manufacture and market the basic materials that are used in practically every conceivable kind of product.

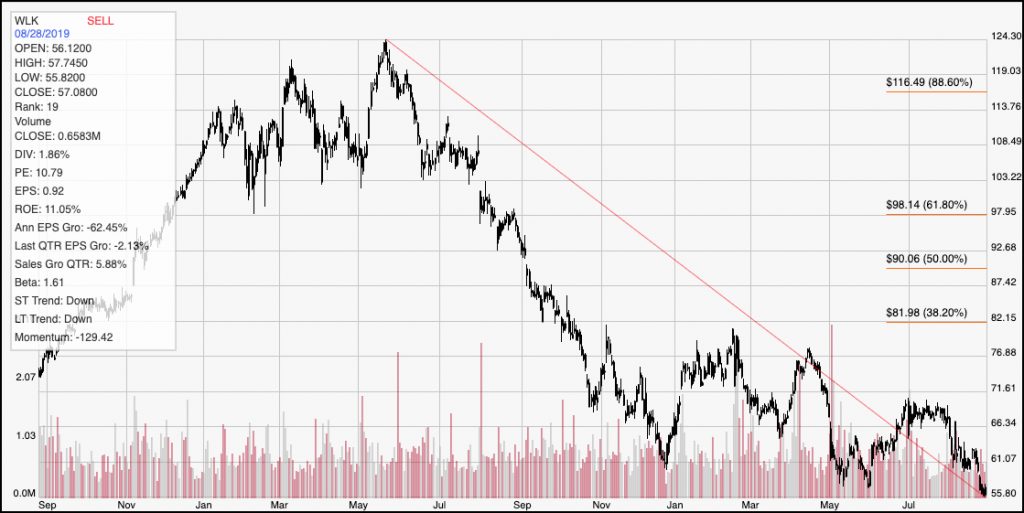

WLK has underperformed the sector, and many of its competitors over the past fifteen months; after reaching a high in May of 2018 at around $124, the stock has dropped back to its current level at around $57. The stock was showing signs of recovery from late May of this year until July, finding a peak a little below $70 before picking up bearish momentum again and dropping back about -15.5% in the last month. The stock is currently sitting at a multi-year low, and is showing signs it could drop even more – but it is also a dividend-paying stock, trading at a deep discount, that fits my earlier description of fundamental strength. Does that make a value stock you should pay attention to? You decide.

Fundamental and Value Profile

Westlake Chemical Corporation is a global manufacturer and marketer of basic chemicals, vinyls, polymers and building products. The Company’s products include a range of chemicals, which are fundamental to various consumer and industrial markets, including flexible and rigid packaging, automotive products, coatings, water treatment, refrigerants, residential and commercial construction, as well as other durable and non-durable goods. Its segments include Olefins and Vinyls. It manufactures ethylene (through Westlake Chemical OpCo LP (OpCo)), polyethylene, styrene and associated co-products at its manufacturing facility in Lake Charles and polyethylene at its Longview facility. The Company’s products in its Vinyls segment include polyvinyl chloride (PVC), vinyl chloride monomer (VCM), ethylene dichloride (EDC), chlor-alkali (chlorine and caustic soda) and chlorinated derivative products and, through OpCo, ethylene. It also manufactures and sells building products fabricated from PVC. WLK’s current market cap is $7.3 billion.

Earnings and Sales Growth: Over the last twelve months, earnings declined sharply, by -62.45, while revenues dropped by about -4%. In the last quarter, earnings improved, but still somewhat negative, at -2.13%, while sales increased by 5.88%. A lot of stocks in the Chemicals industry are showing a similar earnings pattern, as trade, currency, and even energy prices have worked against the industry. This is a concern, but as it is related to macroeconomic concerns rather than management issues, it isn’t a major red flag. The company’s margin profile is generally healthy, but is also showing signs of erosion, with Net Income running at 7.38% of Revenues for the last twelve months, and declining to 5.55% in the last quarter.

Free Cash Flow: WLK’s free cash flow is generally healthy, at $526 million. This measurement is also showing signs of erosion, since it was a little over $1 billion one year ago. It’s current level translates to a Free Cash Flow Yield of 7.3%.

Debt to Equity: WLK’s debt/equity ratio is .47, which is conservative and implies the company takes a careful approach to debt management. WLK’s cash and liquid assets in the last quarter were about $409 million while long-term debt was about $2.9 billion. While their operating profile indicates they should have no problem servicing their debt, it is also true that cash has declined in the last year from about $800 million, suggesting that liquidity has also deteriorated and could be a concern.

Dividend: WLK pays an annual dividend of $1.05 per share, which translates to a dividend yield of about 1.87% at the stock’s current price.

Price/Book Ratio: there are a lot of ways to measure how much a stock should be worth; but one of the simplest methods that I like uses the stock’s Book Value. WLK’s Book Value is $48.80, which means that the stock’s Price/Book ratio right now is 1.16. WLK historical average Price/Book ratio is 2.41, which means that the stock is significantly undervalued, by more than half. WLK’s Price/Cash Flow ratio also shows a similar, undervalued perspective, which means that between both measurement there is a case to be made for a long-term target price between $117 and $119 per share.

Technical Profile

Here’s a look at the stock’s latest technical chart.

Current Price Action/Trends and Pivots: The red diagonal line traces the stock’s downward trend from May of 2018 to its recent low around $55; it also provides the baseline for the Fibonacci retracement lines shown on the right side of the chart. The stock’s downward trend can’t be missed, and its acceleration of bearish momentum in the last month is a clear sign the stock could drop even more; however in the last couple of days it has also increased from that low around $55 to its current level at around $57. It has immediate resistance around $59, but if the stock can break above that level, it could see a short-term bullish rally to around $65 per share. If support at $55 breaks down, the stock could tumble to lows between $49 and $50 that it hasn’t seen since late 2016.

Near-term Keys: WLK’s current bearish momentum seems to make any near-term bullish outlook very aggressive, with downside risk being quite a bit higher than any upside potential. If you don’t mind being aggressive, however, a break above $59 could offer a momentum-based signal to buy the stock or work with call options; but be ready to take profits quickly at between $64 and $65 if you do decide to place a bullish trade. The more likely near-term scenario is that the stock will break support at $55 and offer a signal for a bearish trade, either by shorting the stock or working with put options. In that case, the exit target is around $49. If you are working with a long-term perspective, and the short-term downside doesn’t scare you, the truth is that WLK’s value proposition is pretty attractive, and could only get better in the days and weeks to come. The fundamentals are generally strong, but given the state of its downward trend and accelerating bearish momentum, I would prefer to see improvements in Free Cash Flow, available cash, and strengthening Net Income before I take WLK seriously as a truly compelling value candidate.