Just about all of the attention of market analysts and talking heads this year has focused on just a couple of economic sectors as the best places to find opportunities for growth in the stock market. Given the fact that the entire world has had to deal with the effects of the coronavirus epidemic, and a massive number of industries have simply been trying to survive the impact of broad-based shutdowns, I don’t think it’s too surprising that most of attention has been focused on sectors like Healthcare, where companies are racing to develop vaccines and anti-viral treatments, and Technology, where cloud and remote networking services have enabled a number of companies to shift their operations into practical, work-at-home arrangements.

For average investors, that has pushed a lot of focus away from other sectors that tend to ebb and flow in a cyclical fashion. Cyclical stocks are those that are expected to do well when economic conditions are generally healthy, and that will naturally struggle when the economy struggles. One of the core sectors of the economy that fits this description is the Transportation sector, which takes in a broad set of industries, including airlines, railroads, trucking and freight, overseas shipping, and so on.

Uncertainty and volatility amid signs that the economy is is struggling means that you can often find stocks in these industries trading at pretty significant discounts to their not-so-distant highs. That makes them tempting fodder for a contrarian, value-oriented investor. I like to look at these stocks, because their fundamental profile can give me some useful clues about their ability to weather an economic downturn. These are also stocks that, like any other, can see big swings from high to low based on nothing more than market’s expectation for what the economy might do in the near future.

CSX Corporation (CSX) is a good example of the kind of stock I’m referring to. As one of the largest transportation companies in the Road & Rail industry, this is a stock that is very sensitive to a variety of economic dynamics, from commodity and fuel prices to interest rate fluctuations. The collapse of oil prices earlier this year is something that means that fuel costs should generally be lower, which is a good thing; but as economy activity ground to a halt during the second quarter of the year, so too did the demand for transportation services.

From a bear market bottom in March, the stock rebounded like most of the rest of the market as investors acted on the hope that the net economic effect would be temporary; but since reaching a June high at around $76, just a little below the stock’s 52-week high near $80, the stock has retraced a bit as infection spikes across the country have forced some states to pause economic reopening, or in some cases to even reimpose restrictions. The potential continuation of the health crisis is something that shouldn’t be ignored, as it has the potential to extend the economic downturn, which many analysts seem to expect could pass as early as the end of this year into a much longer and more protracted period of time – especially if some models that predict the earliest practical vaccines could be approved and made available for broad-based, public implementation is sometime in mid-2021 or possibly even 2022.

Cyclical stocks like CSX are sensitive to the kind of pressure I’ve just outlined, which is why it becomes important to take a critical look at the company’s balance sheet and overall fundamental strength. This is a company with a strong fundamental profile, and a balance sheet that has weathered the pandemic storm reasonably well to this point. That is a positive that bodes well for the company in the long-term, but another question we have to answer is whether the stock’s current trading price represents a useful value under current market conditions to justify taking its long-term opportunity seriously. Let’s dive in.

Fundamental and Value Profile

CSX Corporation is a transportation company. The Company provides rail-based freight transportation services, including traditional rail service and transport of intermodal containers and trailers, as well as other transportation services, such as rail-to-truck transfers and bulk commodity operations. The Company categorizes its products into three primary lines of business: merchandise, intermodal and coal. The Company’s intermodal business links customers to railroads through trucks and terminals. The Company’s merchandise business consists of shipments in markets, such as agricultural and food products, fertilizers, chemicals, automotive, metals and equipment, minerals and forest products. The Company’s coal business transports domestic coal, coke and iron ore to electricity-generating power plants, steel manufacturers and industrial plants, as well as export coal to deep-water port facilities. CSX has a current market cap of $55 billion.

Earnings and Sales Growth: Over the last twelve months, earnings declined nearly -40%, while sales dropped -26.3%. In the last quarter, earnings fell -35% while sales shrank a little over -21%. Even with those declines – induced first by tariff pressures from the trade war between the U.S. and China that dominated headlines in 2019, and then by the pandemic – CSX operates with a healthy, margin profile; in the last twelve months, Net Income was 26.4% of Revenues, declining modestly to 22.13% in the last quarter.

Free Cash Flow: CSX’ Free Cash Flow is healthy, at about $3.08 billion. It is worth noting that while this number declined from $3.55 billion in late 2019, the drawdown has been modest. Their current Free Cash Flow number translates to a Free Cash Flow Yield of 5.64%.

Debt to Equity: CSX has a debt/equity ratio of 1.33. This indicates the company is highly leveraged; but this is also typical of stocks in the Transportation industry. Their balance sheet indicates they have about $2.6 billion in cash and liquid assets against nearly $16.1 billion in long-term debt as of the most recent quarter. CSX’ operating profile suggests their should be no problem servicing the debt they carry.

Dividend: CSX pays an annual dividend of $1.04 per share, which at its current price translates to a dividend yield of about 1.48%. Their dividend payout ratio is also conservative, at less than 25% of their earnings over the last year and has increased from the end of 2019, when it was $.96 per share.

Price/Book Ratio: there are a lot of ways to measure how much a stock should be worth; but I like to work with a combination of Price/Book and Price/Cash Flow analysis. Together, these measurements provide a long-term, fair value target around $77 per share. That means the stock is moderately undervalued, with 9% upside from its current price, with a useful bargain discount at around $62.

Technical Profile

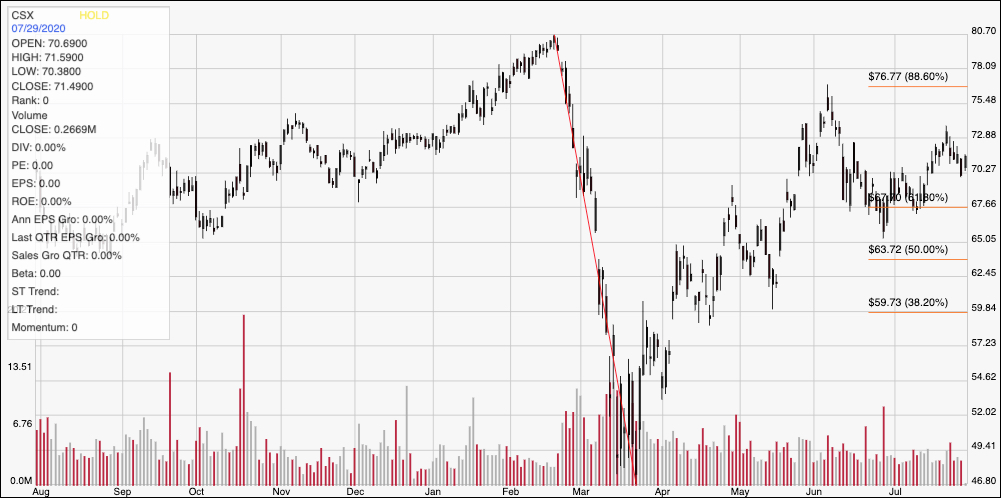

Here’s a look at the stock’s latest technical chart.

Current Price Action/Trends and Pivots: The chart above displays the past year of price activity for CSX. The stock’s peak at a little below $81 came in February, after which the pandemic prompted the stock to follow the rest of the market to an extreme, bear-market low at around $47 per share. From that point the stock rebounded strongly to a June peak at around $77 before falling back again late in that month to support around $66. This month the stock saw another short rally, with the last peak marking immediate resistance at around $73, with support at the stock’s recent pivot low at around $70. A break above $73 should give the stock room to rally to its June peak at $77, with additional room if bullish momentum continues to test its 52-week high around $81. A drop below $70, on the stock hand has immediate downside to somewhere between $65 and $67.

Near-term Keys: From a long-term perspective, it’s hard to see a lot of long-term upside in CSX, despite its generally strong fundamental profile. Based on the fair value analysis I described earlier, the stock wouldn’t offer a compelling value-based price unless it drops to about $62 per share – which is about -11.4% below the stock’s current price, with only about 9% upside to its fair value price. That means the best opportunities to work with the stock are with short-term, momentum-oriented trades. If you want to be bullish, look for a break above $73 as a signal to buy the stock or work with call options, using $77 as a useful short-term profit target. A drop below $70 is a signal to think about shorting the stock or buying put options, with a practical point on a bearish trade anywhere between $65 and $67 per share.