As an analyst, I take a lot of interest in trying to find reasons the market stages some of the moves it makes. The factors, geopolitical, economic, or emotional, that drives trends over any time period can be widely varied, and sometimes it’s interesting to see not only what is influencing the market today, but also to look back and, with the advantage of hindsight, being able to evaluate whether a certain condition or element played a role in driving the market to the point it is at today.

Among the various macroeconomic factors I try to pay attention to is the ebb and flow of oil prices. I think oil is one of the most interesting commodities of all; no matter whether you drive a gas-guzzler, an electric vehicle or a hybrid, the truth is that oil is a factor in every sector of the market, with tentacles that reach into economic policy and most certainly into geopolitics.

The beginning of 2020 started with oil leading financial headlines as Saudi Arabia and Russia engaged in a brief but damaging price war that saw crude prices start to tumble from peaks around the mid-$60 per barrel range for West Texas Intermediate (WTI) crude, and mid-$70’s for Brent. That drop only accelerated beginning in February as global COVID-19 fears took hold and forced financial markets all over the world to drop to bear market lows. That saw WTI crude to hit its own low around $20 per barrel before it finally started to recover.

As the economy has reopened, and summer ushered in the beginning of a new driving season, some expected demand for oil to increase and begin to reduce inventories; actual inventory reports, however have recently revealed that inventories have continued to build, which means that demand has remained low. That has forced WTI crude to fall from the mid-$40 range to around $37 per barrel level as of this writing.

The drop in oil prices has naturally been working against the energy sector, which includes oil explorers and producers, especially the largest players like ConocoPhillips (COP). In the last month, the stock has dropped from a June peak at around $50 to its current price at around $33. That’s the kind of bearish momentum that would have most growth-oriented investors running away from the sector – but for a contrarian-minded value investor, it could also mean that there could be good opportunities to take advantage of steep bargains.

Fundamentally speaking, COP has a lot going for it, with healthy cash flow and very manageable debt levels that have been a product of a strict focus by management over paying a high, unsustainable dividend or pushing for heavy production growth. COVID-related pressures only demonstrated the wisdom of management’s conservative approach; the company has so far been able to weather the storm better than a number of other companies in the sector. That could mean COP is a stock worth paying attention to right now.

Fundamental and Value Profile

ConocoPhillips is an independent exploration and production company. The Company explores for, produces, transports and markets crude oil, bitumen, natural gas, liquefied natural gas (LNG) and natural gas liquids. The Company operates through five segments: Alaska, Lower 48, Canada, Europe and North Africa, Asia Pacific and Middle East, and Other International. The Alaska segment explores for, produces, transports and markets crude oil, natural gas liquids, natural gas and LNG. The Lower 48 segment consists of operations located in the United States Lower 48 states and the Gulf of Mexico. Its Canadian operations consists of oil sands developments in the Athabasca Region of northeastern Alberta. The Europe and North Africa segment consists of operations and exploration activities in Norway, the United Kingdom and Libya. The Asia Pacific and Middle East segment has exploration and production operations in China, Indonesia, Malaysia and Australia. COP’s current market cap is $35.6 billion.

Earnings and Sales Growth: Over the last twelve months, earnings decreased more than -191%, while sales also dropped -52%. In the last quarter, the decline in earnings accelerated by -304.5%, while sales dropped about -16.5%. COP’s margin profile is healthy, but showing signs of deterioration that aren’t entirely surprising given conditions of the last few months. Net Income over the last twelve months was 8.49% of Revenues, and weakened to 6.47% in the last quarter.

Free Cash Flow: COP’s free cash flow is healthy, at more than $5.4 billion for the trailing twelve month period and which translates to a Free Cash Flow yield of 15.32%.

Debt to Equity: COP has a debt/equity ratio of .47, a relatively low number that indicates the company operates with a conservative philosophy about leverage. They reported about $7.8 billion in cash and liquid assets in the last quarter versus $14.8 billion in long-term debt. The combination of good liquidity along with operating profits that are sufficient to service their debt, generally gives them much better financial flexibility than most of the other stocks in the industry.

Dividend: COP pays an annual dividend of $1.65 per share, which translates to a yield of 5.1% at the stock’s current price. That puts COP among the highest dividend-paying stocks in the market, at a time that many other stocks are reducing or completely eliminating their dividend payouts.

Price/Book Ratio: there are a lot of ways to measure how much a stock should be worth; but I like to work with a combination of Price/Book and Price/Cash Flow analysis. Together, these measurements provide a long-term, fair value target around $50 per share. That means that COP is trading at a discount of more than 50% right now, which makes the stock very tempting from a value perspective.

Technical Profile

Here’s a look at the stock’s latest technical chart.

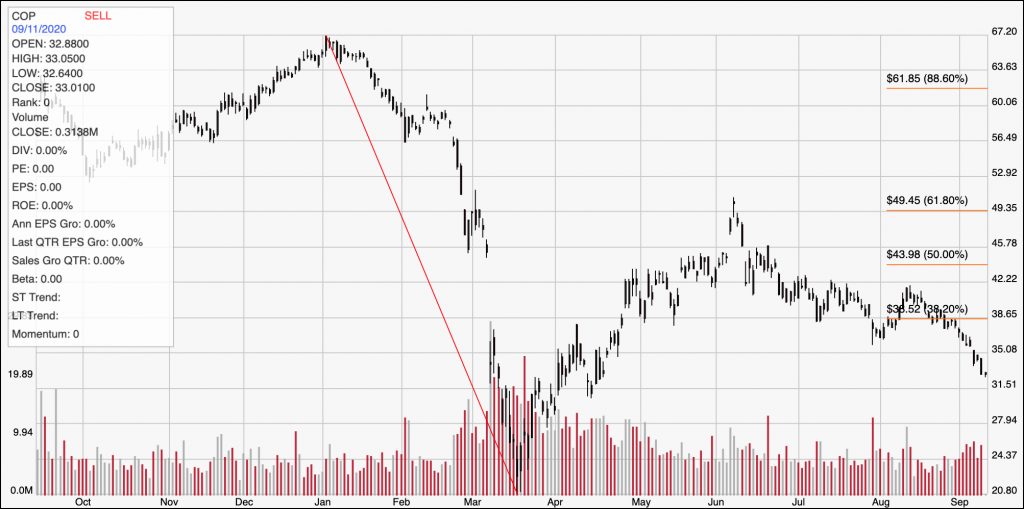

Current Price Action/Trends and Pivots: The red diagonal line traces the stock’s downward plunge from its December high at around $67 to its bear market low in March at about $21; it also informs the Fibonacci retracement lines shown on the right side of the chart. In the last month, the stock has fallen back from a high at about $42 per share, dropping below the 38.2% retracement line to a current price around $33 per share. Based on previous pivot activity, the stock should offer support around $31.50 per share, with current resistance at around $38.50. A bounce off of support offers interesting upside to around $38.50, while a drop below support at $31.50 could see the stock keep falling to retest its bear market lows around $21.

Near-term Keys: If you work strictly off of the basis of the stock’s valuation, COP looks like a terrific value; however the stock’s current bearish momentum, along with the reality of current economic conditions mean that taking a long-term bet right now requires the ability and willingness to accept the potential for a continued drop to much lower levels. If you prefer to work with short-term trading strategies, you could use a bounce off of support anywhere between the stock’s current price and $31.50 as a signal to buy the stock or start using call options, using $38 as a useful profit target. A drop below $31.50 could also be a good signal to think about shorting the stock or buying put options, with a short-term target price between $24 and $21 per share on a bearish trade.