It’s kind of funny to see how popular opinion among investors shifts under different conditions. A stock market that has recovered in record time from the fastest plunge to bear market low in recorded history, in the face of the pandemic that prompted the downturn in the first place continues practically unabated, has prompted investors by and large to move away from conservative, defensive-oriented stocks and back to the high-flying kinds of companies that seem to offer the most growth. That means that a lot of the buzz has focused around companies that facilitate work-from-home business operating models or encourage other activities that make self-isolation and the social restrictions associated with living through a pandemic easier. That is why stocks like Zoom Video (ZM), Shopify (SHOP), and Amazon.com (AMZN), to name just a few, have gone parabolic, emerging from those bear market lows to push to extreme new highs that in some cases have more than doubled the value of those shares.

You can argue whether those stocks moved too far, too fast, but the fact is those kinds of extraordinary results will shift a majority of the popular discussion about the market to those stocks. But pandemic conditions offer a lot of different storylines about how you can keep your money working for you; some just aren’t as “sexy” as others, because their business isn’t disruptive to an existing industry, or because the company has a long history as an American staple.

I have written quite a bit about how I like to pay attention to stocks in the Food Products industry when market conditions become more uncertain and broad volatility starts to increase. That’s because while the industry itself can hardly be described as disruptive, the truth is that demand for food doesn’t go away. Consumer trends during periods of economic expansion and extended bull markets often tend to pull away from the established, “traditional” names and brands we’ve all grown up with, but when unemployment is high (even though the latest report has kept the needle moving in a positive direction, it is still around 8.5%) and uncertainty remains about how quickly economic activity will pick up again at the consumer level, a lot of households gravitate back to those familiar brands – because they have been long-established brands due to the fact that they offer good value. They may not be disruptive in their industry, or all that exciting, but they do make it easier for parents to stock their pantries and keep their kids fed.

The earliest phases of the pandemic saw a big shift to some of these stocks, like Campbell Soup Co. (CPB), as families responded to initial shutdown and shelter-in-place orders by stockpiling and building up food storage in their homes. That meant that prepackaged, easy-to-prepare food products, that can be stored for extended periods and stay good were immediately more attractive than they had been in some time. And while it’s safe to say that most of the stockpiling component of this year’s economic trend has passed, reports still indicate that demand for these types of products remains high. CPB, for example is still reporting sizable increases in sales versus the same period last year, when popular opinion was that CPB was outdated and out-of-touch with the Millennial generation and its buying preferences. The pandemic has put pressure on CPB’s supply chain, which has hindered operations somewhat in the last few months and forced management to invest heavily to address those limitations; but those capital investments are expected to pay off in the long run in the form of greater overall cost efficiency.

CPB is a stock that I’ve followed for quite some time and used on a few different occasions over the last couple of years for different, useful trading opportunities. In late 2018, CPB finalized the acquisition of snack food company Snyder’s-Lance, bringing into their brand portfolio some of the products that we can think of as “comfort foods” for social isolation, like Kettle brand potato chips, Goldfish crackers, and Pepperidge Farm cookies. That has helped them broaden their appeal away from just the soup aisle to other areas of your grocery store that is likely to keep them relevant and important. I think it’s also a reason that, while most analysts would still call CPB’s stock “boring,” the price increased from around $40 in July of 2019 to a peak in late August at around $53. Since the last earnings report, where the supply chain problems I previously mentioned came to light, the market has pushed the stock about-15% below that peak, but at the same time this is a stock that continues to offer a compelling value proposition backed by improving free cash flow and a generally healthy balance sheet. That suggests there is still plenty of room to grow.

Fundamental and Value Profile

Campbell Soup Company (CPB) is a food company, which manufactures and markets food products. The Company’s segments include Americas Simple Meals and Beverages; Global Biscuits and Snacks, and Campbell Fresh. The Americas Simple Meals and Beverages segment includes the retail and food service channel businesses. The segment includes the products, such as Campbell’s condensed and ready-to-serve soups; Swanson broth and stocks; Prego pasta sauces; Pace Mexican sauces; Campbell’s gravies, pasta, beans and dinner sauces; Plum food and snacks; V8 juices and beverages, and Campbell’s tomato juice. The Global Biscuits and Snacks segment includes Pepperidge Farm cookies, crackers, bakery and frozen products; Arnott’s biscuits, and Kelsen cookies. The Campbell Fresh segment includes Bolthouse Farms fresh carrots, carrot ingredients, refrigerated beverages and refrigerated salad dressings; Garden Fresh Gourmet salsa, hummus, dips and tortilla chips, and the United States refrigerated soup business. CPB’s current market cap is $13.7 billion.

Earnings and Sales Growth: Over the last twelve months, earnings increased 50%, while revenues rose 18.43%. In the last quarter, earnings were -24 lower, while sales were -5.8% lower. The quarterly decline is attributable to the supply chain inefficiencies already described, and which I expect to be a temporary condition. CPB’s operating profile is healthy, but like many stocks, pandemic conditions have had a deteriorating effect. In the last twelve months, Net Income was 18.73%, but decreased to 4.08% in the last quarter. This is also a reflection of supply chain issues. Management has stated they expect these issues to normalize in the months ahead, and so I believe the last quarter’s deterioration to be a temporary effect.

Free Cash Flow: CPB’s free cash flow is $1.1 billion over the last twelve months. This is a big increase from earlier this year, when Free Cash Flow was about $860 million. The current number translates to a Free Cash Flow yield of 8.02%.

Debt to Equity: CPB has a debt/equity ratio of 1.94. which indicates the company is highly leveraged. This isn’t especially unusual for the industry, and most of the company’s debt load is attributable to the Snyder’s-Lance acquisition. Cash and liquid assets were $859 million versus only $58 million at the beginning of the year; but this number did decline from $1.2 billion in the quarter prior as the company increased capital expenditures to address the supply chain. Long-term debt is around $4.9 billion – a number that has dropped significantly since the Snyder’s-Lance deal closed and long-term debt stood at around $8 billion.

Dividend: CPB pays an annual dividend of $1.40 per year, which at its current price translates to an annual yield of about 3.08%.

Price/Book Ratio: there are a lot of ways to measure how much a stock should be worth; but I like to work with a combination of Price/Book and Price/Cash Flow analysis. Together, these measurements provide a long-term, fair value target around $62 per share. That means the stock is significantly undervalued, with about 37% upside from its current price.

Technical Profile

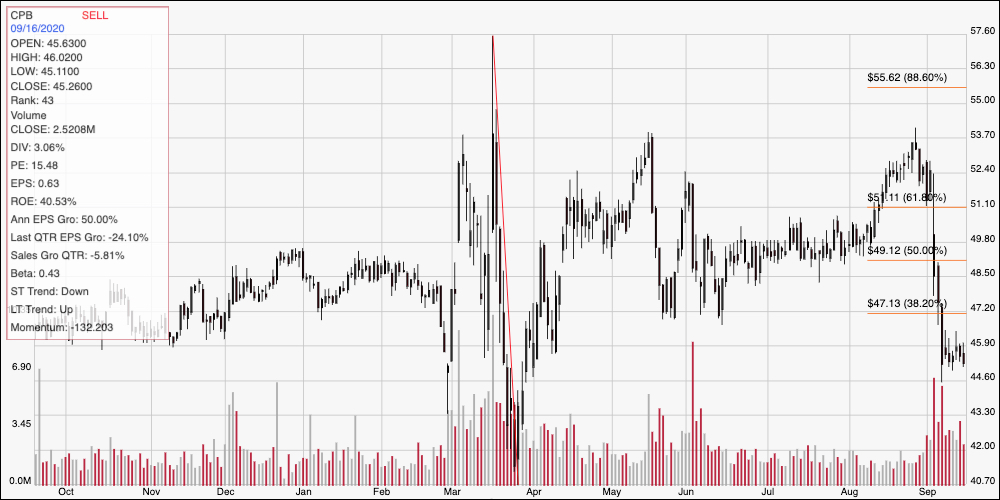

Here’s a look at the stock’s latest technical chart.

Current Price Action/Trends and Pivots: The red diagonal line traces the stock’s plunge in March from a high at around $57 to a bear market low around $41. It also provides the baseline for the Fibonacci retracement lines shown on the right side of the chart. After consolidating in a narrow range through most of June and all of July, the stock broke to a short-term peak at around $53 per share in late August before the latest earnings report prompted investors to start selling. In the last week, the stock has found support around $45 per share, with immediate resistance at the 38.2% retracement line around $47 per share. A push above $47 should give the stock room to rally to the 50% retracement line, which is around $49, with $51 reachable beyond that if bullish momentum picks up. A drop below $45 would likely give the stock enough bearish momentum to see it test its 52-week low at around $41.

Near-term Keys: CPB’s plunge since its last earnings report has most bullish-minded investors running for the exits; but it is also improving the stock’s value proposition more each day the stock remains under pressure. CPB is a stock that is a bit difficult to use for short-term trading strategies like swing or momentum trades; even so, a push above resistance at $47 could offer an interesting bullish opportunity by either buying the stock or working with call options, using $49 as an initial profit target with additional upside to about $51 if bullish strength remains healthy. A drop below $45 could act as a signal to consider shorting the stock or working with put options, with the stock’s bear market low around $41 offering an interesting bearish target point.