While the Tech sector has been a bit depressed over the last month, most analysts continue to expect Tech stocks to lead the market for the foreseeable future. That is especially true for stocks that specialize in the technologies that enable remote networking and cloud-based operations. If you follow the sector, or this particular trend, you are probably already familiar with some of the names in that segment, and that have been leading the sector’s surge throughout the year – but you may not be familiar with the companies that provide the services and solutions for those companies. The Semiconductor industry is a good example of an industry that supplies most of what makes just about every other kind of Tech solution possible; another is the Electronic Manufacturing Services industry.

Sub-industries can offer interesting opportunities to work with a fast-moving sector from a different angle than most can expect. Jabil Inc. (JBL) is an interesting example. This is a company that established itself by providing manufacturing services for a very narrow market segment – mobile phone manufacturers like Apple (AAPL), which continues to be their largest single customer. Over the last few years, however the company has worked to diversify its operations to reduce its reliance on that narrow segment and into cloud business as well as industrial and energy services. The stock has nearly doubled in price since hitting a bear market low in March but still has diverged from the sector’s pattern since June.

JBL is currently sitting at the top end of a tight consolidation range it has held since that time. Could it be ready to break out and push higher to test its pre-pandemic highs? Possibly; it has some interesting fundamental strengths, along with an interesting value proposition. Let’s dive in to the numbers to see if it is also worth considering on a long-term basis.

Fundamental and Value Profile

Jabil Inc., formerly Jabil Circuit, Inc., provides electronic manufacturing services and solutions throughout the world. The Company operates in two segments, which include Electronics Manufacturing Services (EMS) and Diversified Manufacturing Services (DMS). The Company’s EMS segment is focused on leveraging information technology (IT), supply chain design and engineering, technologies centered on core electronics, sharing of its large scale manufacturing infrastructure and the ability to serve a range of markets. Its DMS segment is focused on providing engineering solutions and a focus on material sciences and technologies. It provides electronic design, production and product management services to companies in the automotive, capital equipment, consumer lifestyles and wearable technologies, computing and storage, defense and aerospace, digital home, emerging growth, healthcare, industrial and energy, mobility, packaging, point of sale and printing industries. JBL’s current market cap is $5.3 billion.

Earnings and Sales Growth: Over the last twelve months, earnings increased 29.41%, while revenues increased 11%. In the last quarter, earnings increased by a whopping 229.4%, while sales were 15.2% higher. JBL operates with a very narrow, but improving margin profile; over the last twelve months, Net Income was 0.2% of Revenues, and strengthened in the last quarter to 0.93%.

Free Cash Flow: JBL’s free cash flow is healthy, at about $460.9 million, and translates to a Free Cash Flow Yield of 8.91%.

Dividend Yield: JBL’s dividend is a modest $.32 per share, and translates to an annual yield of about 0.93% at the stock’s current price.

Debt to Equity: JBL has a debt/equity ratio of 1.47. This is a high number, and usually reflects a high degree of leverage. In JBL’s case, however their balance sheet shows healthy liquidity, with cash and liquid assets of nearly $1.4 billion in the last quarter versus $2.6 billion of long-term debt. It is also noteworthy that the company’s cash grew from around $763 million in the quarter prior. Their healthy liquidity and Free Cash Flow, for now are effective counters to their narrow margin profile, and strongly suggest they should have no problem servicing their debt; however any kind of reversal of Net Income could create problems on that front.

Price/Book Ratio: there are a lot of ways to measure how much a stock should be worth; but I like to worth with a combination of Price/Book and Price/Cash Flow analysis. Together, these measurements provide a long-term target at about $43 per share. That suggests JBL is trading at a healthy discount, being undervalued by about 21% right now.

Technical Profile

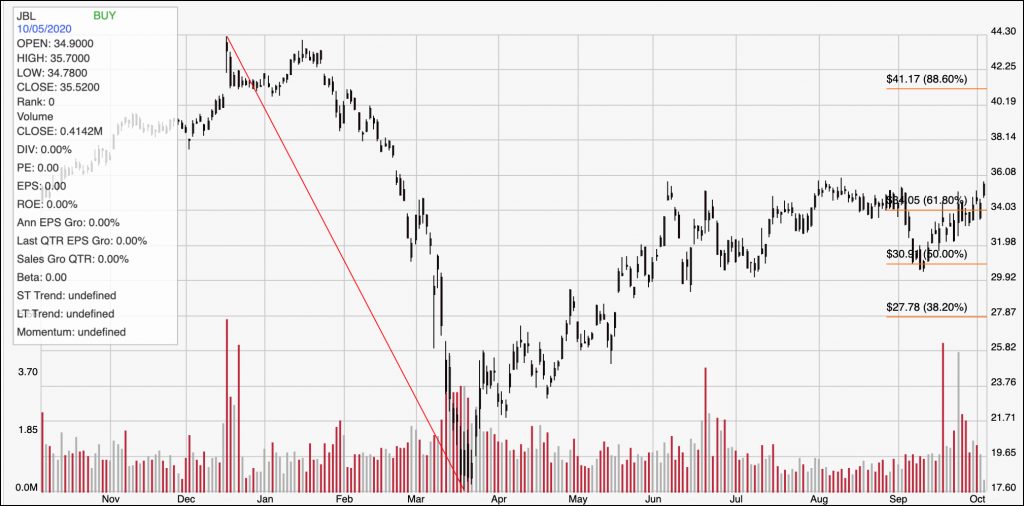

Here’s a look at the stock’s latest technical chart.

Current Price Action/Trends and Pivots: This chart traces the stock’s movement over the last year. The red diagonal line marks the stock’s downward slide from a 52-week high at around $44 to its low point in mid-March at around $17.50; it also provides the baseline for the Fibonacci retracement lines shown on the right side of the chart. The stock rallied strongly from that low to a peak in early June at the 61.8% retracement line, marking a near-term peak at around $36 per share before falling back to find support at around $30. In the last month, the stock has rallied off of that support point to approach the $36 high point with some strong bullish momentum. A break above $36 could give the stock room to rally close to the $40 range, while a pivot and drop off of resistance at $36 has near-term downside to about $31.

Near-term Keys: If you’re looking for a short-term, bullish trade, a break above $36 could offer a useful signal to buy the stock or work with call options, with an eye on a quick exit target between $39 and $40. A pivot off of resistance at $36, on the other hand, could offer a useful signal to consider shorting the stock or working with put options, with an eye on $30 as a bearish profit target. The stock’s value proposition is compelling, and the company’s fundamentals are generally solid. JBL’s narrow margin profile has the company riding a razor’s edge in its operations, which means that any misstep could be costly. I would prefer to see margins improving; but If you aren’t afraid of the potential for the stock to be volatile in current market conditions, I think there is a long-term opportunity in a stock with a useful value opportunity in one of the hottest sectors of the market right now in.