As a value-focused investor with more than a bit of a contrarian bent, I tend to get nervous when stocks keep making one new high after another, and I like it when I see stocks trading at or near historical lows. That’s pretty different than the mindset of most investors that focus on growth first, and I understand why – one of the most basic rules around trend analysis states that stocks tend to follow the direction of the next longer trend. That means, in part, that in the short term, a stock is more likely to go up if it has already been going up for at least a few months. If the stock has been going up for a year or more, then the rule should hold even more strongly.

The contrarian part of my investing system revolves around what a stock should be worth at any given time. I like to try to identify what I think represents a fair value for a stock. That mindset differs a bit from straight growth investing, because it uses a stock’s underlying fundamental strength, mixed with historical valuation metrics, to arrive at that “fair value” price. It is an attempt to smooth out the volatility that often exists in stocks as they swing from extreme high to extreme low and consider price movement in a more objective fashion than simply assuming that because a stock has been going up or down, it is going to keep moving that direction. If a stock is trading at a discount relative to historical valuations, with a strong book of business underneath, there is a strong argument to be made that the stock should trade higher than it is right now, and that is where the meat-and-potatoes of my investing strategy lies.

I’ve written a lot in this space about the fact that Tech has outperformed the rest of the market throughout the pandemic – and is expected to continue to do so. In fact, the sector seems to be one of the few sectors that many analysts seem to believe is destined to succeed no matter what the economy does in the near-term, or to what extent COVID-19 continues to exert its influence into 2021. The longer pandemic pressures persist, cloud-based, remote networking and work-at-home Tech companies will remain a prime focus for investors looking for bullish trading opportunities. If you start to think in post-pandemic terms, the picture remains pretty bullish, as enterprise demand should stabilize and rebound and investors begin to shift more and more of their attention to the next wave of big tech, which will be in 5G networking and the resulting increase in the Internet of Things (IoT). These are elements that are already in place in the economy, but that I think will get a lot more focus once the health crisis finds its eventual closing point. That doesn’t mean that you can simply buy any Tech stock you want – but it does mean that if you’re careful and selective, you can still find some good opportunities.

Seagate Technology (STX) is one of the biggest providers of storage technology solutions. Where many of its competitors, like Micron (MU) and Western Digital Corporation (WDC) have emphasized innovating in the emerging flash, NAND, and SSD memory space, STX has stayed fixed in traditional disk drives. While demand in traditional PC’s has dropped, the truth is that truly high-capacity storage – the kind required for network and cloud servers, where the tech sector has seen the most growth this year – is still only practical with traditional disk storage technology. That is where STX has put its greatest focus, and where analysts continue to expect to see growth. The work-at-home dynamic certainly played a role in helping STX’s stock drive nearly 41% higher to around $55 by early June after hitting a March low at around $39; from that point the stock dropped sharply back to a low in late July around $44. From that point, STX has begun to build a new upward trend and is now sitting just a little below $50. Despite that increase, the stock remains significantly below its pre-pandemic highs around $64 – a fact that is one of the reasons I find the stock intriguing. Does that mean the stock is trading at a deep discount right now, and should be higher, or is its distance from its 52-week a sign indication of other, deeper problems? Let’s find out.

Fundamental and Value Profile

Seagate Technology public limited company is a provider of electronic data storage technology and solutions. The Company’s principal products are hard disk drives (HDDs). In addition to HDDs, it produces a range of electronic data storage products, including solid state hybrid drives, solid state drives, peripheral component interconnect express (PCIe) cards and serial advanced technology architecture (SATA) controllers. Its storage technology portfolio also includes storage subsystems and high performance computing solutions. Its products are designed for applications in enterprise servers and storage systems, client compute applications and client non-compute applications. It designs, fabricates and assembles various components found in its disk drives, including read/write heads and recording media. Its design and manufacturing operations are based on technology platforms that are used to produce various disk drive products that serve multiple data storage applications and markets. STX has a current market cap of $12.7 billion.

Earnings and Sales Growth: Over the last twelve months, earnings increased by about 28% while sales grew 6.16%. In the last quarter, earnings dropped almost -15%, while revenues decreased by about -7.5%. The company’s margin profile is generally healthy, but like most companies right now has shown signs of deterioration; over the last twelve months, Net Income was 9.55% of revenues, but shrank to about 6.6% in the last quarter.

Free Cash Flow: STX has generally healthy free cash flow of a little over $1.13 billion over the last twelve months. This number has decreased from a high point in September of 2018 at around $2.1 billion. At the stock’s current price, this also translates to a Free Cash Flow Yield of about 9.02%.

Debt to Equity: the company’s debt to equity ratio is 2.33, an elevated number that suggests STX is highly leveraged. The company’s balance sheet indicates their operating profits are more than sufficient to service their debt, with $1.72 billion in cash and liquid assets and a little over $4.1 billion in long-term debt.

Dividend: STX pays an annual dividend of $2.60 per share, which translates to an annual yield of 5.29% at the stock’s current price. Not only is that remarkable for a tech company, most of which don’t pay any dividend at all, but this is also well above the industry average. It is also worth noting that while competitors like WDC have suspended their dividend payout to preserve cash, STX has increased their dividend from $2.52 about a year ago.

Price/Book Ratio: there are a lot of ways to measure how much a stock should be worth; but I like to work with a combination of Price/Book and Price/Cash Flow analysis. Together, these measurements provide a long-term, fair value target around $38.25 per share. That means that STX is clearly overvalued right now, with about -22% downside from its current price. Its actual bargain price is even lower, at a little below $31.

Technical Profile

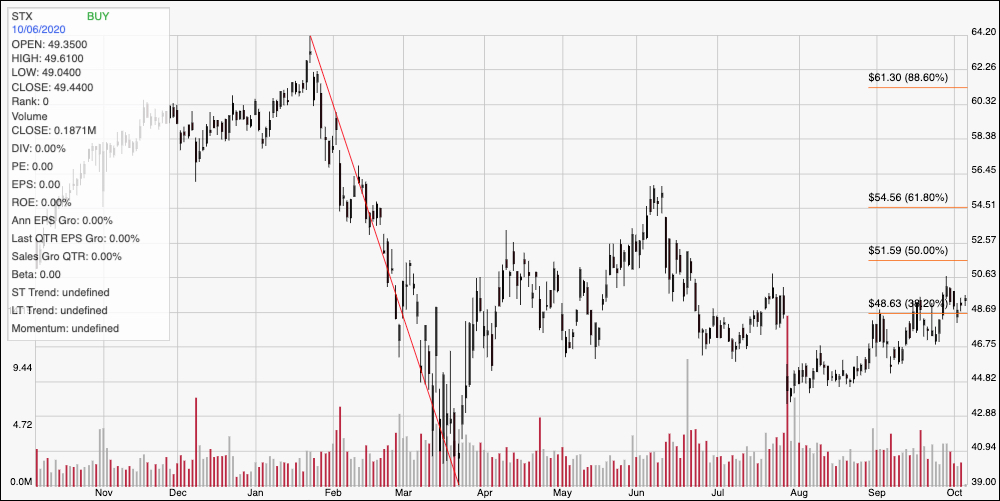

Here’s a look at the stock’s latest technical chart.

Current Price Action/Trends and Pivots: The diagonal red line traces the stock’s downward slid from a January peak at around $64 to its March low at close to $39 per share. It also provides the baseline for the Fibonacci retracement lines shown on the right side of the chart. From that low, the stock rebounded quickly, pushing to a high around $55 in early June before falling back to a late July low around $44. From that point the stock has started to rebound, pushing above the 38.2% retracement line to a little above $50 as of this writing. Immediate support is around $48.50, inline with the 38.2% retracement line, with resistance at around $51.50 where the 50% retracement line sits. The stock appears to be bouncing off of support, so a continued push higher should give the stock room to test $51.50, with room to extend to $54.50 where the 61.8% line sits if bullish momentum picks up. A drop below $48.50 has downside to next support around $46.40 based on previous pivot activity in that area.

Near-term Keys: STX has some interesting fundamental metrics working in its favor right now; despite those strengths, however, the stock is clearly overvalued. That means that if you want to work with the stock on a long-term basis, you’re doing it strictly on the basis of its growth prospects. The fact is that most analysts aren’t overly bullish on the storage segment’s long-term prospects right now, as declining consumer trends in the space provide a big counter and major headwind to the strength of enterprise demand, which is expected to narrow through the rest of the year and into 2021. I think that means that the best probabilities for a stock like STX lie in shorter-term trading strategies. If the stock can keep rallying off its current support, you could think about buying the stock or working with call options, using $51.50 as a good profit target. A drop below $48.50 could be a good signal to consider shorting the stock or buying put options, with a profit target around $46.50 on a bearish trade that could extend to around $45 if bearish momentum accelerates.