While most of the Tech sector has been leading the market throughout the year, there are some stocks that have definitely not kept pace. That is always true in any sector, not matter what the broad sector momentum looks like, there are always individual companies that will diverge from the normal pattern.

In 2020, the best Tech stock have been those that were tied in one way or another to remote, distance-based networking, cloud, and collaboration solutions. That trend has not too surprisingly been driven by a forced shift in corporate America away from traditional in-office operations to dispersed, work-at-home solutions due to the ongoing health crisis. That has made the companies that were already providing solutions – wide area and virtual private networking, video conferencing, web collaboration, and more – to facilitate distance-driven interactions much bigger pieces of corporate tech budgets than they were before.

In the same vein, companies that focus on the “enterprise” space – where most corporate tech spending has traditionally gone, for products like servers, computers, printers, and the tools to connect them all in a traditional network setting, for example – have struggled to keep up. In fact, even as vaccines are deployed around the globe right now and in the early parts of 2021, some analysts wonder how much of the work-from-home element of corporate operations will become a permanent part of business life. Even so, it also makes sense that some portion of white-collar workers are going to shift back to some in-office operations, even though that shift back may take some time. That could mean that many of the companies that operate in the Enterprise space could continue to be pressured well into 2021.

That brings us to today’s highlight. Hewlett Packard Enterprise Co. (HPE) is a spin off of Hewlett Packard Corporation (HPQ) that has is among those companies that have underperformed throughout the year, falling from a pre-pandemic high at around $16.50 at the end of 2019 to a March low at around $7.40. It mostly hovered within a couple of dollars of that low until November, when the stock started picking up a lot of bullish momentum; in fact, from that start point a little above $8 in November, the stock has rallied to its current price at around $12 per share. That marks a strong, short-term upward trend that was driven initially by a positive response from investors to the company’s latest earnings report. Does that make HPE a company you should pay attention to? Let’s check it out.

Fundamental and Value Profile

Hewlett Packard Enterprise Company (HPE) is an edge-to-cloud platform-as-a-service company. The Company’s segments include Compute, High Performance Compute & Mission-Critical Systems (HPC & MCS), Storage, Advisory and Professional Services (A & PS), Intelligent Edge, Financial Services (FS), and Corporate Investments. The Compute portfolio offers both general-purpose servers for multi-workload computing and workload-optimized servers. HPC & MCS portfolio offers workload-optimized servers designed to support specific use cases. FS provides investment solutions, such as leasing, financing, information technology (IT) consumption, and utility programs and asset management services, for customers that facilitate technology deployment models and the acquisition of complete IT solutions, including hardware, software and services from HPE and others. Corporate Investments include Hewlett Packard Labs, which is responsible for research and development. HPE has a current market cap of $15.5 billion.

Earnings and Sales Growth: Over the past year, earnings declined about -25%, while sales were flat, but negative at -0.1%. In the last quarter, earnings improved 15.6%, while sales grew 5.75%. The company operates with a narrow, but improving margin profile that appears to be emerging from negative status earlier this year; over the last twelve months, Net Income was just -1.19% of Revenues, but increased to 2.18% in the last quarter.

Free Cash Flow: HPE’s Free Cash Flow is modest, at about $560 million. On a Free Cash Flow Yield basis, that translates to 3.59%. Just a few months ago, Free Cash Flow was about $1.2 billion, and started the year at $1.7 billion. That decline is a good indication of the kind of pressure the company has had to deal with in 2020 as enterprise spending has spending, with corporations deferring many of their expensive technology purchases throughout the year.

Debt to Equity: HPE has a debt/equity ratio of .76, which is a conservative number. Their balance sheet shows $8.4 billion in cash against $12.1 billion in long-term debt. Their balance sheet indicates their operating profits are adequate to service their debt for now; however if Net Income turns back to a negative pattern in the quarters ahead, the company will be forced to rely primarily on its strong liquidity. It is worth noting that at the beginning of 2020, cash and liquid assets were about $3.1 billion.

Dividend: HPE pays a dividend of $.48 per share, which translates to an annual yield of about 3.96% at the stock’s current price. I think that it is also noteworthy that the company has not cut or reduced their dividend; in fact it remains a bit above the $.44 per share payout they maintained until the beginning of 2020, when management increased the dividend.

Price/Book Ratio: there are a lot of ways to measure how much a stock should be worth; but I like to worth with a combination of Price/Book and Price/Cash Flow analysis. Together, these measurements provide a long-term target at about $15.33 per share. That suggests that even with the stock’s current increase, HPE stock is nicely undervalued by about 28%.

Technical Profile

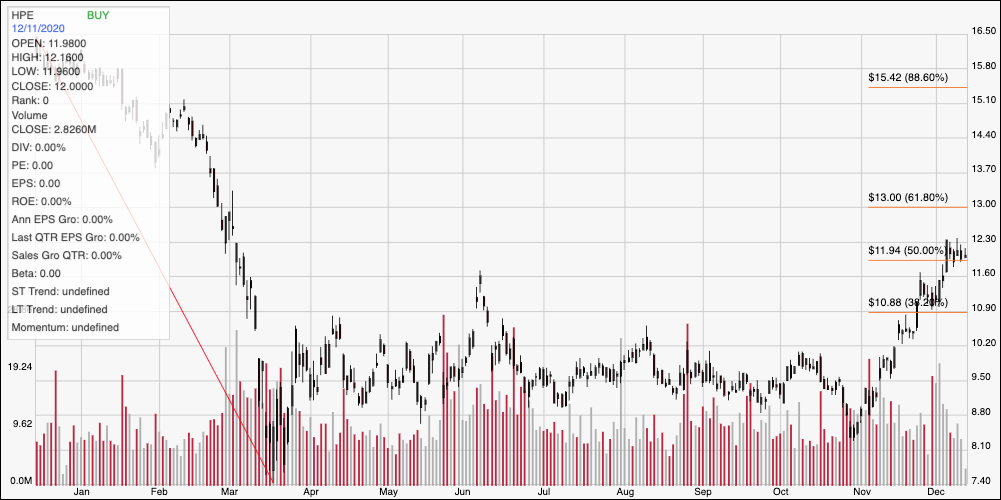

Here’s a look at the stock’s latest technical chart.

Current Price Action/Trends and Pivots: The chart above traces the last year of price activity for HPE. The red diagonal line traces the stock’s decline to a bear market, March low at around $7.40; it also provides the baseline for the Fibonacci retracement lines shown on the right side of the chart. The stock’s increase since November pushed it out of a narrow consolidation range at the bottom of its downward trend, and it has since punched its way above both the 38.2% and 50% retracement lines. Since previous resistance should act as new support, immediate support should be right around $12 where the 50% retracement line rests, while immediate resistance could sit right at $13 based on the 61.8% retracement line. If that line doesn’t hold, however there is near-term upside to see the stock push to anywhere between $14.50 and $15.50 where the 88.6% retracement line lies. A drop below $12 should find next support a little below $11 where the 38.2% retracement line waits.

Near-term Keys: The stocks’ current momentum is interesting, and if you prefer to focus on short-term trades could be a reason to start looking for a trading signal. A break above $13 could offer an opportunity to buy the stock or work with call options, using a target at around $14.50 as a functional profit target for a bullish trade. A drop below $12 might provide a signal to short the stock or buy put options, with $11 acting as a very close, near-term target. I think the best probabilities with HPE actually lie on the long-term, value-based side. This is a company that appears to have weathered the worst that 2020 has been hand out, and that I think will be in good position to lead out in a very crowded and competitive industry, which means that the near-term could see some volatility; but with a healthy dividend and a nice value proposition, it could offer a patient investor some good opportunities.