Throughout the course of the last couple of years I’ve found the Consumer Staples sector, and specifically the Food Products industry a good place to find useful investing opportunities. In 2018 and 2019, a lot of that was being driven by international trade concerns that increased uncertainty in the marketplace. 2020 made the industry a good place to be as the pandemic prompted a massive consumer shift back towards value-based packaged foods. Dining out just hasn’t really been a thing in the last year – unless you count going through a drive-thru or placing a pick up order and then eating in your car “eating out.” Social distancing requirements and dine-in restrictions around the country have kept pressure on restaurants, bars, and clubs that we normally associate with enjoyable social activities. In addition, the latest jobs numbers in the last month show not only that unemployment remains well above the levels seen more than a decade ago, which means that a large number of American families remain financially pressured. Together, that means that food storage, and home dining is likely to continue to follow a similar trend this year as last.

As we’ve shifted into a new year, there appears to have been a clear investor shift away from Food Products stocks, which is why a number of stocks in that category are down 10% or more in the last few weeks despite indications that I usually take as a positive. Economic and industry analysts all expect that the consumer trends I described earlier will show “stickiness” in 2021, meaning that instead of being simple reflections of temporary pressures, they likely represent long-term behavioral shifts. In addition, a lot of these companies have shown improving fundamental profiles throughout the last year, including material improvements in cash flows, debt reduction, and overall balance sheet strength.

Contrast those positives to the current downward pressure on the industry, and I think what is happening amid political turmoil in the U.S. and vaccine distribution is a near-term investor preference to look ahead and hope for the best. I’m not a doomsayer; I am hopeful that 2021 will see the pandemic finally recede into history and social and economic activity will finally start to return to some kind of modified sense of normalcy. I also think that coming out of January with a new political leadership in Washington in place – including a new White House laying out what most expect to be an aggressive and ambitious agenda for its first 100 days that will certainly be different from the mostly business-friendly attitude of the Trump administration – could put the brakes on some of the unbridled enthusiasm many of the hottest sectors of the past year have seen. I think that means that Consumer Staples will still have its place as a smart place to keep in mind in 2021.

You still have to be careful, though; it’s pretty easy to gravitate to well-known, established names like GIS, CPB, and KR, to name just a few, but just because a company has a great name and brand, it doesn’t mean the stock is a good opportunity right now. It is still important to pay attention to a company’s underlying business – in fact, I would argue that it may be more important than ever, because even with strong relative price performance since March 2020, a number of Food Products stocks continue to reflect very attractive valuation levels. That fact can lead to the mistaken notion that it is a bargain; but sometimes, a stock drops off of those historical highs because the market is trying to tell you something.

Kraft-Heinz Co. (KHC) is an example of what I mean. Look in your pantry or fridge, and you’ll probably find a lot of their products on your shelves. In terms of recognizability, there aren’t too many food brands that can claim the brand recognition this company has. Heinz condiments including ketchup, mustard, mayonnaise have been a mainstay of my fridge for years, and Kraft brands like Oscar Meyer are regulars, too. That should mean the company has a stable, strong business, right? Not so fast. One of the big struggles a lot of traditional names in the Food Products business have been fighting has been the trend away from pre-packaged products and into healthier, organic options. While some, like CPB and GIS, seem to finding ways to stay relevant, KHC has struggled. They’re in the midst of a multiyear, long-term transformation strategy, and the pandemic prompted a stock-your-pantry mindset that gave a lot of companies in this industry, including KHC an opportunity to recapture lost customer and gain new ones. 2021 will be an important year to determine if they can retain that new market share. In the meantime, this is a stock that has followed the broad industry trend lower over the last few weeks, but has some interesting fundamental strengths that I think makes its value proposition worth paying attention to. Let’s dive in to the numbers so you can decide if this is a company that is worth putting to work for you.

Fundamental and Value Profile

The Kraft Heinz Company is a food and beverage company. The Company is engaged in the manufacturing and marketing of food and beverage products, including condiments and sauces, cheese and dairy, meals, meats, refreshment beverages, coffee and other grocery products. The Company’s segments include the United States, Canada and Europe. The Company’s remaining businesses are combined as Rest of World. The Rest of World consists of Latin America and Asia, Middle East and Africa (AMEA). The Company provides products for various occasions whether at home, in restaurants or on the go. The Company’s brands include Heinz, Kraft, Oscar Mayer, Philadelphia, Planters, Velveeta, Lunchables, Maxwell House, Capri Sun, and Ore-Ida. The Company’s products are sold through its own sales organizations and through independent brokers, agents and distributors to chain, wholesale, cooperative and independent grocery accounts, convenience stores, drug stores, value stores, bakeries and pharmacies. KHC’s market cap is about $39 billion.

Earnings and Sales Growth: Over the last twelve months, earnings improved slightly, at about 1.45%, while sales grew 6%. In the last quarter, earnings and revenues were both negative, at about -12.5% and -3.11%, respectively. KHC’s margin profile appears to be improving; Net Income as a percentage of Revenues was -1.92% over the last twelve months, but strengthened markedly in the last quarter, to 9.27%.

Free Cash Flow: KHC’s free cash flow was about $6.2 billion (a sizable improvement from $4.6 billion a year ago, and $560 million in mid-2019) over the past twelve months and translates to a useful Free Cash Flow Yield of 15.79%.

Dividend Yield: KHC’s dividend is $1.60 per share, and translate to an above-average yield of 5% at its current price.

Debt to Equity: KHC has a debt/equity ratio of .57. This is a low number that I think is a bit misleading given a high proportional level of debt versus cash and liquid assets. Their balance sheet shows $2.7 billion in cash and liquid assets against more than $27.8 billion in long-term debt. While debt is significantly below the $31 billion mark it saw in mid-2020, cash has also declined from about $5.4 billion at the beginning of 2020.

Price/Book Ratio: there are a lot of ways to measure how much a stock should be worth; but I like to work with a combination of Price/Book and Price/Cash Flow analysis. Together, these measurements provide a long-term, fair value target just little under $51 per share. That means the stock is trading at a big discount, with about 59% upside from the stock’s current price.

Technical Profile

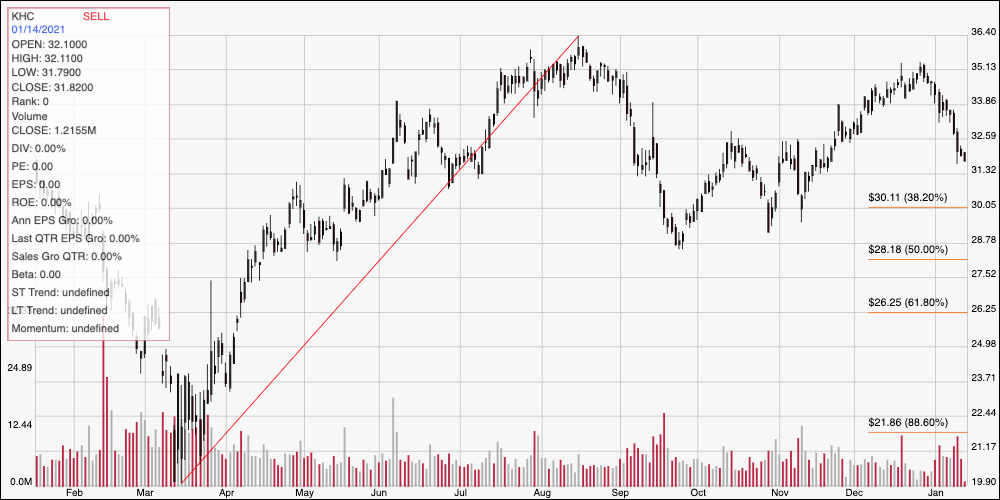

Here’s a look at the stock’s latest technical chart.

Current Price Action/Trends and Pivots: This chart traces the stock’s movement over the last two years. The diagonal red line traces the stock’s upward trend from a March low at around $20 to its high point in August at about $36.50 per share. It also acts as the baseline for the Fibonacci retracement lines shown on the right side of the chart. The stock dropped off of that August peak to a September low at around $29, then rallied again to about $35 at the end of December before dropping back again to its current level below $32 per share. Immediate support should be around $30 where the 31.8% retracement line sits, with immediate resistance expected to be at around $34 based on pivot high activity in that range on multiple occasions over the last year. A drop below $30 should find next support in the $28.50 to $28 price area, where the 50% retracement line lies in the same region as the stock’s September pivot low point. If the stock can find support anywhere between its current price and $30 and reverse its currently bearish momentum to push above $34, additional resistance points lie at around $35 and the stock’s $36.50, 52-week high point.

Near-term Keys: Given the stock’s momentum, the best probabilities of success right now lie more strongly on the bearish side for KHC – but the smart bet is to wait to see if the stock stabilizes around $30 or drops below it. A good bearish signal would come from a drop below $30 per share, using $28 as a quick-hit exit target. If the stock does stabilize, and starts to rally again anywhere between its current price and $30, you can also consider buying the stock or working with call options, with $34 acting as a nice bullish, quick-hit profit target. The stock’s value proposition is very compelling, and the fundamentals have mostly been improving for the year, which makes the long-term potential very interesting. At the very least, KHC is a Food Products stock that is worth keeping in your watchlist.