For the stock market, 2021 clearly appears to reflect investor’s desire to move away from the pandemic-dominated conversations of 2020 and look ahead. One of the ways that has been seen over the last few weeks is in a pretty broad rotation away from conservative, defensive-oriented stocks in sectors like Consumer Staples and into more cyclical names. Ih the last week, I’ve heard the word “boring” used to describe those defensive-minded stocks on news media. Despite the bearish pressure being put on a lot of those stocks right now, the “boring” description makes me chuckle. That’s because I still think these are smart stocks to pay attention to.

I’ve been writing for quite some time in this space about the value to be found in defensively-positioned industries. One of those is the Food Products industry, where a lot of established brands we all grew up can be found. Before the pandemic forced people to stay at home and start stocking their pantries and freezers, a lot of these traditional names were out of favor with the market and with the Millennial generation as being tired, old, and out of touch with the times – in other words, “boring.” One of the specific segments of the industry this has been seen in is in cereal consumption, where consumers had been drifting away from packaged cereal products, but saw an increase in demand in 2020 because of the pandemic.

The reason I like stocks in this industry is that when economic conditions get tough enough that people start losing their jobs and seeing income levels drop, a lot of assumptions about what is “cool” and “hip” start to go away. The latest unemployment report showed claims ticking back up above 900,000, after mostly trending lower into the end of 2020; but the fact that current claims are still about 50% above the highest levels seen in the last recession more than a decade should make anybody think twice about taking too much risk in the stock market right now. My take on that information is that the worst isn’t over; in fact a lot of economists are saying that it will take years, not months for employment to increase again to healthy levels.

Consider that, even as vaccines are being approved and distributed, health experts are still forecasting pandemic conditions to persist into the second quarter of 2021. That means that the long-anticipated “return to normal” may not be seen in tangible terms until late this year – or possibly beyond. That means economic conditions are likely to remain challenged, which means that consumers are going to have to keep thinking in very critical terms about how they’re going to tighten their belts to make it through. That’s why I think a lot of the old, “tired” brands that we always saw in our parent’s fridges, freezers and pantries, and that are still around today look a lot more attractive, because in most cases those brands have always been built around value. Tightening the belt often means these products come back into favor since they make it easier for parents to keep their kids fed.

Kellogg Company (K) is a classic example of what I mean. They do a lot more than just cereal, of course, but the truth is that the cereal aisle is where you recognize them the most quickly. After following the broad market to a bearish low in March 2020 around $54, the stock rebounded to a peak in late July at nearly $73. From that point, the stock has dropped back into a clear downward trend, and as of this writing is only a couple of dollars away from that bear market low point. That sad stock performance belies the fact that K’s balance sheet is healthy, with improving profit and operating margins and a healthy dividend providing good evidence of sustained fundamental strength. That’s why I think that, even with the current bearish momentum, K’s value proposition is too good to ignore. Let’s take a look.

Fundamental and Value Profile

Kellogg Company is a manufacturer and marketer of ready-to-eat cereal and convenience foods. The Company’s principal products are ready-to-eat cereals and convenience foods, such as cookies, crackers, savory snacks, toaster pastries, cereal bars, fruit-flavored snacks, frozen waffles and veggie foods. Its segments include U.S. Morning Foods, which includes cereal, toaster pastries, health and wellness bars, and beverages; U.S. Snacks, which includes cookies, crackers, cereal bars, savory snacks and fruit-flavored snacks; U.S. Specialty, which represents food away from home channels, including food service, convenience, vending, Girl Scouts and food manufacturing; North America Other, which includes the U.S. Frozen, Kashi and Canada operating segments; Europe, which consists of European countries; Latin America, which consists of Central and South America and includes Mexico, and Asia Pacific, which consists of Sub-Saharan Africa, Australia and other Asian and Pacific markets. K’s current market cap is $19.8 billion.

Earnings and Sales Growth: Over the last twelve months, earnings declined about -11.65%, while revenues were 1.69% higher. In the last quarter, earnings we -26.61% lower, while sales declined -1.04%. Despite the negative earnings pattern, the company operates with a margin profile that is strengthening, which is a positive counter that suggests the company is becoming more efficient. Over the last twelve months, Net Income during was 8.8% of Revenues, and increased in the last quarter, to 10.15% of Revenues.

Free Cash Flow: K’s free cash flow is about $1.36 billion and translates to a Free Cash Flow Yield of 6.88%. It should also be noted that Free Cash Flow has improved steadily in each quarter of the past year, from about $590 at the end of 2019.

Dividend Yield: K’s dividend is $2.28 per share, which translates to an annual yield of about 3.94% at the stock’s current price.

Debt to Equity: K has a debt/equity ratio of 1.95. This is a high number, and makes them one of the most heavily leveraged stocks in the Food Products industry. Their balance sheet indicates that in the last quarter, cash and liquid assets were a little over $1.5 billion, versus $7 billion in long-term debt. That actually marks a significant improvement from the latter part of 2019, when cash was $340 million against $8.5 billion in long-term debt. This is a solid confirmation not only that profitability is improving, but also that their balance sheet is getting stronger.

Price/Book Ratio: there are a lot of ways to measure how much a stock should be worth; but I like to work with a combination of Price/Book and Price/Cash Flow analysis. Together, these measurements provide a long-term, fair value target around $89 per share, which means that K is extremely undervalued, with about 55% upside from its current price. I should also mention that in mid-2020, this same analysis offered a $79 long-term target price.

Technical Profile

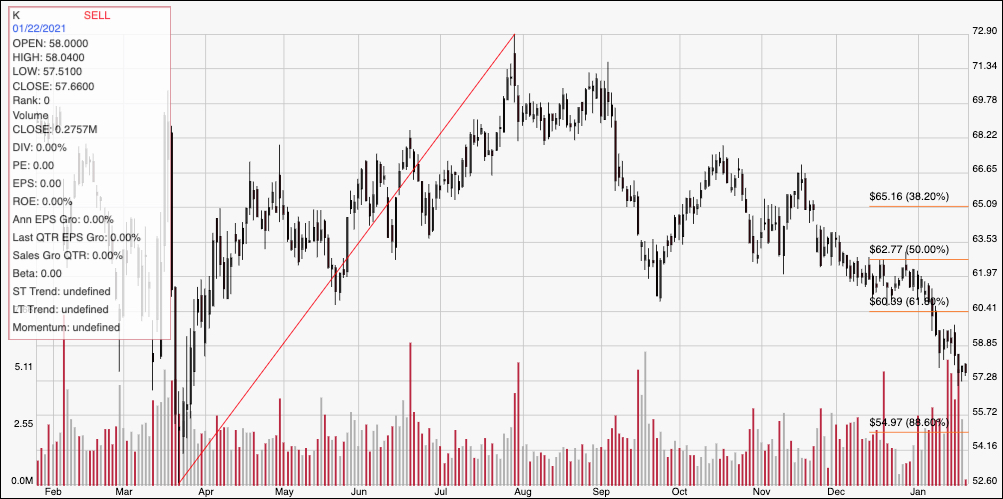

Here’s a look at the stock’s latest technical chart.

Current Price Action/Trends and Pivots: This chart traces the stock’s movement over the last year. The diagonal red line traces the stock’s upward trend from its March 2020, bear market low at around $54 to its July high at around $73. It also provides the baseline for the Fibonacci retracement lines shown on the right side of the chart. After dropping to about $60 in September, the stock temporarily rallied before peaking again at $66 and resuming its downward trend. That includes an acceleration of bearish momentum in the latter part of 2020 and into this week, with the stock looking like it is trying to find support at around $57 right now. Immediate resistance is at about $60 based on the 61.8% retracement line. A drop below $57 should see the stock retest its 52-week low around $54, while a reversal of the upward trend can’t be confirmed until the stock breaks secondary resistance at around $63 where the 50% retracement line currently sits.

Near-term Keys: Even with K’s current bearish momentum, the value proposition on this stock is compelling. If you’re willing to accept the possibility of some near-term volatility, K is a stock that offers an excellent long-term opportunity. If you prefer to focus on short-term trading strategies, you could use a bounce off of support anywhere between the stock’s current price and $57 as a signal to consider buying the stock or working with call options; but the smart approach in this case would be to work with very short-term price targets, with resistance at around $60 offering a good exit point. A drop below $57, on the other hand would provide a strong signal to consider shorting the stock or buying put options, using the stock’s 52-week low at around $54 as a useful profit target on a bearish trade.