One of the things about value investing that I think makes it hard for most investors to embrace is the fact that value-based principles tend to be counter-intuitive to the mindset that most often gets presented about the market. The first, most basic principle of value investing fits well with rule #1 of investing in the stock market – buy low, sell high – but if you listen to talking heads and analysts, stocks that actually are available at significant discounts to historical prices generally get dismissed, while stocks trading at or near all-time highs get pumped even more, with predictions that those prices will continue to move higher.

Value investing becomes counter-intuitive because investors become conditioned to accept the notion – which is, honestly, often correct – that stocks tend to follow their longer trends. That’s a big reason why, when a stock has been going up, the general expectation is that it will continue to go up; it’s a variation on the idea that “a rising tide lifts all ships.” Value investing, however, also understands that all trends are finite, which means that eventually, all trends reverse and start to move in the opposite direction. That means that just as the tides of the sea inevitably rise, and then fall, long, upward trends will fall also, eventually give way to a downward pattern, just as extended downward trends eventually and always will find a bottom and move higher. That is where value analysis begins; if a stock is already trading at a significant discount to its historical highs, the odds begin to increase that when the downward movement reverses, the stock won’t just be cheap compared to previous price activity, but also in comparison to the underlying value of the business itself.

The caveat, of course, is that sometimes a cheap stock is just a cheap stock, having been beaten down because there are serious problems in the company’s business that need to be corrected. That’s why effective value analysis also doesn’t simply take a historical price discount at face value – it also folds a thorough review of the company’s fundamental strength or weakness into the picture to determine if there is a basis to say the stock should be higher than it is right now. This second component is the reason that I think value analysis is so effective at finding useful opportunities in any market condition, because it provides the ability to compare the stock’s current price, no matter whether the current price trend is up or down, against the company’s book of business. If the value proposition is in place, then there is an opportunity to work with the stock that, in the long run, should provide healthy profits that you’ll may miss if you simply try to chase the latest growth stocks in an effort to keep up with the market. It also means that when the market turns seriously bearish, you should be able to avoid being on the sharp end of that downturn.

In that vein, let’s turn our attention to today’s highlight. ConAgra Brands Inc. (CAG) is a stock that I’ve followed some time, and make sure to run a fresh analysis on every so often. While most market media WAGs and talking heads tend to dismiss Food stocks because they’re “boring” and lack sex appeal, they have also proven to especially useful under current market conditions. The initial, downward economic push from the COVID-19 pandemic sent a lot of families rushing to the grocery store to stock up on food items they could pack away in the pantry or the freezer so they could get through shelter-in-place and self-isolation orders across the country. New data from a number of packaged food companies, including CAG’s latest earnings reports, supports the idea that even if eat-at-home trends moderate as restaurants and social gathering places reopen and begin to resume closer-to-normal operation, the need to keep pantries, fridges and freezers well-stocked will still persist as a “sticky” consumer trend.

The pandemic-driven struggles of the past year have meant that while many other sectors continue to deal with serious sales declines, stocks in the Food Products industry, including CAG have by contrast enjoyed significant boosts in sales and earnings. For CAG, that has translated to material gains in critical measurements like free cash flow and Book Value. At the early stage of the pandemic, my analysis put a “fair value” target for the stock at around $38.50 per share; but as of now, a new set of financial data from the last few earnings reports to work with have actually given me a reason to lift that number – which is unexpected, even in this industry, under still somewhat uncertain economic conditions. That means that if you’re looking for a smart place to put your money to work for you, CAG is a stock you should be paying attention to.

Fundamental and Value Profile

Conagra Brands, Inc., formerly ConAgra Foods, Inc., operates as a packaged food company. The Company operates through two segments: Consumer Foods and Commercial Foods. The Company sells branded and customized food products, as well as commercially branded foods. It also supplies vegetable, spice and grain products to a range of restaurants, foodservice operators and commercial customers. Conagra Foodservice offers products to restaurants, retailers, commercial customers and other foodservice suppliers. The Company also operates in the countries outside the United States, such as Canada and Mexico. The Company’s brands include Marie Callender’s, Healthy Choice, Slim Jim, Hebrew National, Orville Redenbacher’s, Peter Pan, Reddi-wip, PAM, Snack Pack, Banquet, Chef Boyardee, Egg Beaters, Rosarita, Fleischmann’s and Hunt’s. The Company sells its products in grocery, convenience, mass merchandise and club stores. CAG’s current market cap is $18 billion.

Earnings and Sales Growth: Over the last twelve months, earnings increased about 25%, while Revenues rose by about 8.5%. Earnings and sales dropped in the last quarter – to -27.16% and -7.5%, respectively – but that doesn’t paint a complete picture of the company’s profitability, which has remained very stable. The company’s margin profile over the last twelve months is healthy, with Net Income at 10.15% of Revenues over the past twelve months as well as in the last quarter.

Free Cash Flow: CAG’s free cash flow is healthy, and strengthening at about $1.53 billion. That marks a steady increase from $1.4 billion in mid-2020, and $575.6 million at the beginning of 2019. The current number also translates to a useful Free Cash Flow Yield of about 8.39%.

Debt to Equity: CAG has a debt/equity ratio of .99. That number has declined steadily from 1.58 at the beginning of 2019, but the number remains a tad high, a reflection of the reality that the company’s liquidity remains a question mark. In the last quarter Cash and liquid assets were $80.7 million – a decline from $438.2 million from six months ago, versus $8.2 billion in long-term debt. Most of that debt is attributable to CAG’s acquisition of Pinnacle Foods in the last quarter of 2018. The complexities associated with the transition of the two companies into one is part of the reason the stock struggled into the early part of 2019, but reports in the last three quarters indicate that the synergies the company has worked to achieve have been working. In the last year and a half, long-term debt declined by more than $2 billion, which is a positive.

Dividend: CAG pays an annual dividend of $1.10 per share – which the company increased from $.85 in its last earnings call of 2020, and which translates to an annual yield of about 2.93% at the stock’s current price.

Price/Book Ratio: there are a lot of ways to measure how much a stock should be worth; but I like to work with a combination of Price/Book and Price/Cash Flow analysis. Together, these measurements provide a long-term, fair value target at about $46 per share. That means the stock is nicely undervalued, with about 23% upside from its current price.

Technical Profile

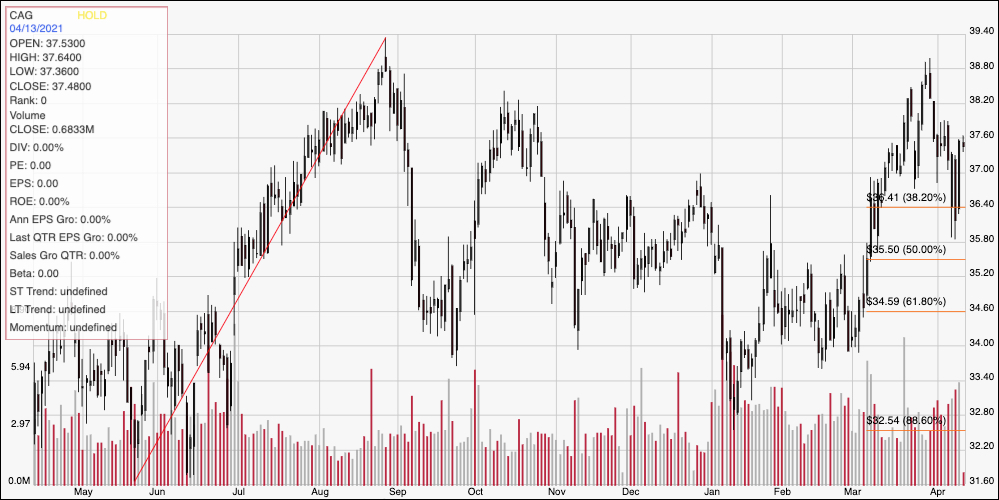

Here’s a look at the stock’s latest technical chart.

Current Price Action/Trends and Pivots: The chart above marks the stock’s price activity over the last year. After peaking in August a little above $39, the stock fell into a gradual downward trend that bottomed at the beginning of this year at around $33 per share. From that point, it started moving into a new upward trend, finding a peak in late March at around $38.50. More recently, the stock marked strong, current support at around $36.50 and looks set to rally right now to test immediate resistance at $38.50 to $39. A drop below $36.50 should have pretty limited downside right now, to around $35 based on a lot of pivot activity around that price area throughout the year.

Near-term Keys: From a fundamental standpoint, CAG’s profile is very attractive, and its value proposition is very useful right now. I agree with analysts that contend that demand for packaged food products such as what CAG offers is going to remain consistent, and that should mean that CAG will continue to stand out in the market through the year. If you prefer to work with short-term strategies, the stock’s current bounce of off support at $36.50 could offer an interesting signal to consider buying the stock or working with call options, with $38.50 as a useful exit target. A drop below $36.50, on the other hand could offer a signal to consider shorting the stock or working with put options, as long as you move quickly to take profits at around $35.