Looking for value in the stock market is something that I have found can be done in any market condition, but it is something that tends to get dismissed by most pundits simply because it isn’t very sexy. Names like Tesla, Netflix, and Amazon practically never make the value list because the massive amount of attention the market has given them for years has kept their stocks priced at levels that makes them impractical to consider strictly on the basis of value. Under most market conditions, looking for value means passing over the names and pockets of the market that get the most buzz to dig into the industries that everyone else tends to overlook. Right now, the industries where I have been finding many of the best valuations right now are generally defensive ones, such as Food Products and Health Care, including big Pharma.

If you’ve been following me in this space at all, or participating in my weekly options trading webinar, you already know that CVS is a good, old friend that I’ve followed for quite some time. Since my last review on this stock, the company has released a new earnings report, which shows continued pressure on Net Income that I believe is mostly a reflection of this year’s health crisis-driven pressures. The short-term result is that my long-term target price has dropped a bit from above $100 around the mid point of last year to around $88 – just a little above the stock’s current price.

As economic activity continues to increase, there is a natural tendency to want to say that COVID-19 is a thing of the past, but I think it is important to keep in mind that healthcare services continue to contend with the virus, even as they are able to begin resuming other, normalized operations that have been put on hold for the past year and a half. Variants of the virus are increasing infection rates in various parts of the country, mostly among the unvaccinated population, and that means that the role CVS and other pharmacy companies will take as places the public at large can go to get vaccinated will continue to be an important of this year’s story. This is a company that was already gaining traction in its broad transformation from just a drugstore/specialty retailer to a health care company providing a variety of services locally and affordably, and it is hard not to take CVS seriously. The company is uniquely positioned for the current environment, not only in the pharmacy space but also with what I think is a big competitive advantage over its competitors owing to its 2018 merger with insurer Aetna.

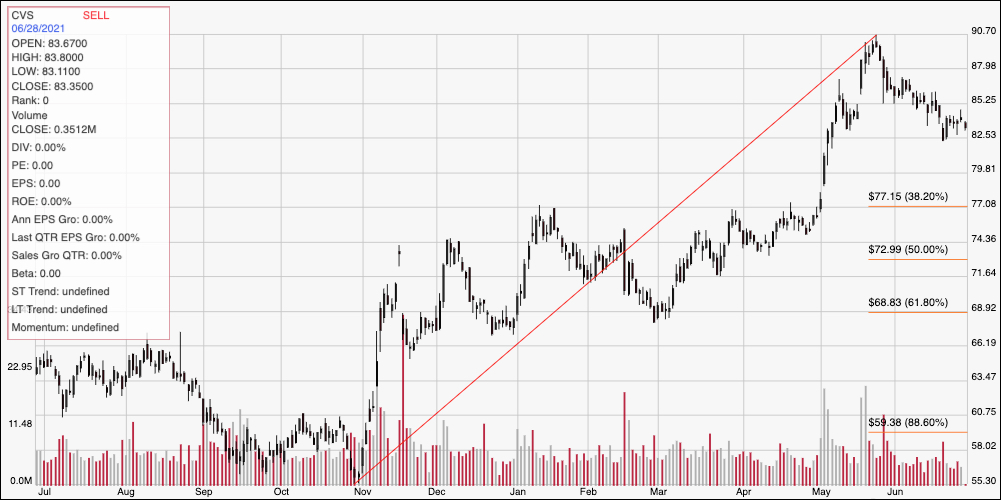

The stock experienced a significant upward trend from early November 2020 to late May of this year, where it peaked at nearly $91 per share. It has been dropping back off of that price since then, and as of this writing is a little more than -8% below that 52-week high. Do the company’s fundamentals support a value proposition far enough above its current price to make CVS an attractive long-term investment opportunity right now? Let’s dig in to find out.

Fundamental and Value Profile

CVS Health Corporation, together with its subsidiaries, is an integrated pharmacy healthcare company. The Company provides pharmacy care for the senior community through Omnicare, Inc. (Omnicare) and Omnicare’s long-term care (LTC) operations, which include distribution of pharmaceuticals, related pharmacy consulting and other ancillary services to chronic care facilities and other care settings. It operates through three segments: Pharmacy Services, Retail/LTC and Corporate. The Pharmacy Services Segment provides a range of pharmacy benefit management (PBM) solutions to its clients. As of December 31, 2016, the Retail/LTC Segment included 9,709 retail locations (of which 7,980 were its stores that operated a pharmacy and 1,674 were its pharmacies located within Target Corporation (Target) stores), its online retail pharmacy Websites, CVS.com, Navarro.com and Onofre.com.br, 38 onsite pharmacy stores, its long-term care pharmacy operations and its retail healthcare clinics. CVS has a market cap of $81 billion. Aetna Inc. is a diversified healthcare benefits company. The Company operates through three segments: Health Care, Group Insurance and Large Case Pensions. It offers a range of traditional, voluntary and consumer-directed health insurance products and related services, including medical, pharmacy, dental, behavioral health, group life and disability plans, medical management capabilities, Medicaid healthcare management services, Medicare Advantage and Medicare Supplement plans, workers’ compensation administrative services and health information technology (HIT) products and services. The Health Care segment consists of medical, pharmacy benefit management services, dental, behavioral health and vision plans offered on both an Insured basis and an employer-funded basis, and emerging businesses products and services. The Group Insurance segment includes group life insurance and group disability products. Its products are offered on an Insured basis. CVS has a market cap of $110.1 billion.

Earnings and Sales Growth: Over the last twelve months, earnings improved by about 6.8%, while Revenues rose by 3.5%. Earnings increased in the last quarter by almost 57% while sales were flat, but -0.66% lower, respectively. The company’s margin profile is very narrow, but after showing some indications of pandemic-driven weakness, appears to be stabilizing; over the last twelve months Net Income was 2.73% of Revenues, and 3.22% in the last quarter.

Free Cash Flow: CVS’s free cash flow is healthy at about $12.9 billion. That does mark a decline from $13.6 billion in June of last year; however the current number still translates to a healthy Free Cash Flow Yield of about 11.68%. It is also worth nothing that CVS’ Free Cash Flow at the beginning of 2020 – before the pandemic started – was $10.4 billion.

Debt to Equity: CVS has a debt/equity ratio of .83. That is a generally conservative number that has dropped from 1 over the past year. In the last quarter Cash and liquid assets were about $8.8 billion versus $59.2 billion in long-term debt. The vast majority of that debt comes from the acquisition of health insurer Aetna, however the fact that long-term debt has dropped from about $65 billion since the beginning of 2020 is a good reflection of the company’s success so far (with plenty of work still to go) in transitioning these disparate organizations into a larger, productive company.

Dividend: CVS pays an annual dividend of $2.00 per share, and which translates to an annual yield that of about 2.38% at the stock’s current price. It is also noteworthy that, while dividend increases have been suspended (not because of COVID, but to give the company flexibility to reduce debt gradually from the Aetna merger), management has maintained the dividend at current levels.

Value Proposition: there are a lot of ways to measure how much a stock should be worth; but I like to work with a combination of Price/Book and Price/Cash Flow analysis. Together, these measurements provide a long-term, fair value target at about $88 per share. That does mark a reduction from than my 2020 fair value target, which was around $103 and below the $91 my analysis provided at the beginning of this year. It is only about 5% above the stock’s current price, and puts a useful bargain price at around $70 per share.

Technical Profile

Here’s a look at CVS’ latest technical chart.

Current Price Action/Trends and Pivots: The diagonal red line marks the stock’s upward trend from November 2020 to its peak last month at around $91. It also provides the baseline for the Fibonacci retracement lines shown on the right side of the chart. The stock has retraced from that peak a little over -8% in the past month, and appears to be finding current support in the $82.50 range, with immediate resistance at around $85. A push above $85 could see the stock rally again to retest the stock’s 52-week high at around $91, while a drop below $82.50 has downside to about $77 where the 38.2% retracement line should offer new support.

Near-term Keys: If you prefer to work with short-term trading strategies, the best opportunity on the bullish side would come from break above resistance at $85; that would be a good signal to buy the stock or work with call options with an eye on $90 to $91 as a useful exit point. A bearish signal would come from a drop below $82.50, with $77 providing a useful target no matter whether you choose to short the stock or buy put options. From the standpoint of value and long-term opportunity, the stock’s increase into May far outpaced the company’s fundamental strength. The stock’s pullback from that high isn’t enough yet to make the stock a useful value opportunity; the downward pullback would likely need to extend into an intermediate-term downward trend, with the stock pushing below the current, 50% retracement line before it really begins to offer an interesting value proposition.