One of the most successful in the entire history of the U.S. stock market, and arguably the most famous of our era is Warren Buffett. His annual reports for Berkshire Hathaway have long been considered required reading for any serious fundamental or value-oriented investor because of the way he outlines his views of current conditions and where he is finding useful opportunities to keep his capital working for him. As a value investor, I’ve borrowed from the principles I’ve seen Mr. Buffett lay out in his annual reports to develop my own approach to value identification.

Snippets and quotes from Buffett’s writings and interviews can be found just about anywhere, but one of the most pertinent to a value-oriented investment approach is, “It’s far better to buy a wonderful company at a fair price than a fair company at a wonderful price.” That concept is something that has reinforced my approach to both fundamental and value analysis over the years and helped me refine my own system to what it is today.

One of the things that the last year and a half has made very clear, at least from an economic perspective, is the difference between “fair” companies and “wonderful” ones. It isn’t as simple as looking at the way a stock’s price has moved, no matter what talking heads and growth-oriented investors would have you believe, and it isn’t about finding companies that have been shielded from the ongoing effects of the COVID-19 pandemic. The truth is that every sector of the economy has had to find ways to adjust to current conditions – and that is often where the difference between “wonderful” and “fair” lies.

One of the sectors that has been really interesting to watch over the past year is the Industrial sector. This segment is interesting because when economic activity picks up, a comparable increase in demand for many of the companies in this space is generally anticipated. A healthy real estate market with persistently high demand in multiple areas of the country, for example, means that home builders can keep new projects going, which usually is good news for Machinery stocks like Paccar Inc. (PCAR). Real estate and construction is hardly the only place PCAR operates, of course; it is really just one example where better-than-expected strength should give this company’s business a lift. PCAR’s leading position in the industry in battery-electric trucks has attracted the interest of many analysts, which many expect to benefit from increasing attention from the public and the government in charging station infrastructure to facilitate wider adoption of electric vehicles, even in heavy equipment and machinery.

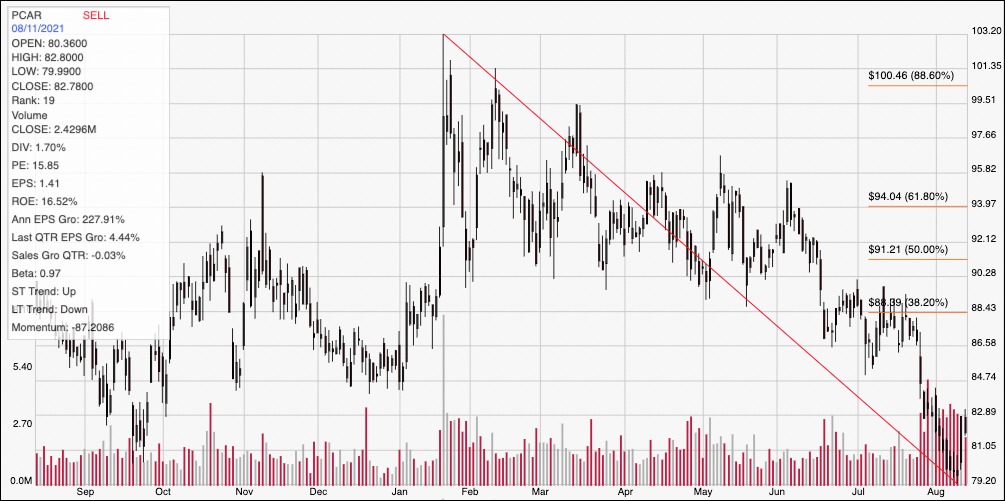

After falling to a March 2020 bottom at around $49, the stock nearly doubled in price by early August of last year, hitting a peak at around $91 per share before falling back to a short-term low around $81. The stock rallied again through October, hitting a new 52-week high at nearly $96 before dropping back to about $82.50 at the end of 2020. From that point, bullish momentum picked up again and pushed the stock to a new yearly high at around $103 in late January. From that high, the stock has dropped into an intermediate-term downward trend that saw the stock hit a recent low point at around $79. The stock’s downward trend has diverged from the sector, which peaked in May has been consolidating near its high ever since. The company’s balance sheet has shown remarkable strength over the past year and a half, even with the pandemic-related pressures that have prevailed in just about every pocket of the economy. Does the stock’s downward trend translate to a useful opportunity to work with it on a long-term, value-oriented basis? Let’s find out.

Fundamental and Value Profile

PACCAR Inc (PACCAR) is a technology company. The Company’s segments include Truck, Parts and Financial Services. The Truck segment includes the design, manufacture and distribution of light-, medium- and heavy-duty commercial trucks. The Company’s trucks are marketed under the Kenworth, Peterbilt and DAF nameplates. It also manufactures engines, primarily for use in the Company’s trucks, at its facilities in Columbus, Mississippi; Eindhoven, the Netherlands, and Ponta Grossa, Brazil. The Parts segment includes the distribution of aftermarket parts for trucks and related commercial vehicles. The Financial Services segment includes finance and leasing products and services provided to customers and dealers. Its Other business includes the manufacturing and marketing of industrial winches. The Company operates in Australia and Brazil and sells trucks and parts to customers in Asia, Africa, Middle East and South America. PCAR has a current market cap of about $28.5 billion.

Earnings and Sales Growth: Over the last twelve months, earnings have improved by about 228% (not a typo), while revenues increased nearly 91%. In the last quarter, earnings improved by about 4.44%, while revenues were flat, but slightly negative a -0.03%. The company’s margin profile is solid, and improving; over the last twelve months, Net Income was 7.9% of Revenues, and strengthened somewhat to 8.43% in the last quarter. I call those numbers “solid” because both aspects of this measurement has stayed consistently in the 7% to 8% range throughout the past year.

Free Cash Flow: PCAR’s free cash flow is healthy, at about $1.67 billion over the last year. That translates to a useful Free Cash Flow Yield of 6.26%. It does mark a decrease from the last quarter, when Free Cash Flow was a little over $2 billion.

Debt/Equity: The company’s Debt/Equity ratio is .64, which is pretty conservative number for stocks in this industry. PCAR’s balance sheet shows $4.5 in cash and liquid assets in the last quarter (up from $3.3 billion at the start of 2020) against $7.15 billion in long-term debt. Their operating profile indicates that profits are sufficient to service their debt, with healthy liquidity to provide additional flexibility.

Dividend: PCAR’s annual divided is $1.36 per share and translates to a yield of about 1.64% at the stock’s current price. Management increased the dividend payout from $1.28 per share at the beginning of this year, providing another positive sign of confidence and strength.

Price/Book Ratio: there are a lot of ways to measure how much a stock should be worth; but I like to work with a combination of Price/Book and Price/Cash Flow analysis. Together, these measurements provide a long-term, fair value target around $87 per share. That means the stock is somewhat undervalued at its current price, by about 6%, with a useful value price down at around $69 per share.

Technical Profile

Here’s a look at the stock’s latest technical chart.

Current Price Action/Trends and Pivots: The chart above shows the last year of price activity for PCAR. The red diagonal line traces the stock’s downward trend from its January peak at around $103 to its low earlier this week at around $79. It also provides the baseline for the Fibonacci retracement lines shown on the right side of the chart. The stock’s downward trend began to accelerate in June as the stock dropped from a peak at around $94.50 per share, pushing its below every support level offered by the Fibonacci retracement lines. Current support is at $79 from the stock’s recent pivot low, but whether that marks the bottom of the stock’s current trend is an open, unanswered question. Immediate resistance should be at around $85, in the area of pivot activity seen in early July as well as multiple points in the latter part of 2020. Using the distance between current support and immediate resistance as a reference means that a drop below $79 could see additional downside to around $73. A push above $85 should find next resistance at around $88.50 where the 38.2% retracement line sits; that line also marks the approximate level the stock would need to reach to mark a legitimate reversal of its current, downward trend.

Near-term Keys: PCAR’s fundamentals are very solid, and in fact have been improving for most of this year. Their balance sheet is one of the strongest in the industry, but at the current price, the stock offers only a modest value. That doesn’t mean there isn’t upside to be had for growth-oriented investors; only that it is not yet trading at attractive valuations for bargain hunters. It also means that the best possibilities lie on the short-term side, via momentum-based trades. A break above resistance at $85 could offer an interesting opportunity to buy the stock or work with call options, with an eye on $88 as a useful, near-term profit target. If the stock drops below $79, consider shorting the stock or buying put options, using $73 as a practical exit target on a bearish trade.