The Technology sector has been a bright spot throughout the COVID-19 pandemic. One of the reasons the sector has led the market for most of the past year and a half is because so much of the shift to remote, work-from-home operations for corporate America, and contactless sales and delivery methods now being used by a lot of retail businesses is driven by technology solutions. That’s driven investors to flock to stocks that specialize in remote networking, conferencing and cloud-based solutions, including digital transaction handling and CRM services. Many of these companies have defied the broader economic trend and managed to post impressive results.

Cognizant Technology Solutions (CTSH) is a professional services company that works with companies in a variety of sectors that focuses on software development and digital platform engineering services for its clients. That puts CTSH in the IT Services industry, which is, at least in part, an area that has continued to see healthy demand as more companies have been forced to identify ways to use technology to shift their business focus. Economists are putting a big focus on companies with healthy balance sheets to help ride through any uncertainty that may extend into a longer-term period of time, and CTSH is company that, despite experiencing its own pressures over the course of the last eighteen months or so, looks to fit that bill as well. From its own bear market low at around $40, the stock rallied to a peak in December 2020 at around $83. After dropping, then retesting its high in May, the stock dropped to a low in mid-July at around $66 per share. After the company’s latest earnings announcement, the stock picked up a fresh wave of bullish momentum, reaching a short-term peak about a week ago at around $78 per share and currently sitting just a little below that level.

As a value-focused investor, my natural inclination when I see a stock hitting a historical high, or driving to a new high is a little different than most growth-oriented investors. Instead of assuming the stock will keep driving to new highs, I tend to question how much gas the stock has left. Of course, I recognize that the fact the stock is at a new high doesn’t automatically mean it is doomed to reverse; but it does prompt me to dive in to the company’s fundamentals to determine if there is a strong, business-based argument case to argue the stock should keep going higher. Let’s see where CTSH sits.

Fundamental and Value Profile

Cognizant Technology Solutions Corporation is a professional services company. The Company operates through four segments: Financial Services, Healthcare, Manufacturing/Retail/Logistics, and Other. The Financial Services segment includes customers providing banking/transaction processing, capital markets and insurance services. The Healthcare segment includes healthcare providers and payers, as well as life sciences customers, including pharmaceutical, biotech and medical device companies. The Manufacturing/Retail/Logistics segment includes manufacturers, retailers, travel and other hospitality customers, as well as customers providing logistics services. The Other segment includes its information, media and entertainment services, communications and high technology operating segments. Its services include consulting and technology services and outsourcing services. Its outsourcing services include application maintenance, IT infrastructure services and business process services. CTSH has a current market cap of $40.3 billion.

Earnings and Sales Growth: Over the last twelve months, earnings increased by a little under 21%, while sales increased by about 14.6%. In the last quarter, earnings improved by 2.06% while Revenues were 4.18% higher. CTSH’s Net Income versus Revenue is healthy, at 9.65% over the last twelve months and strengthening to 11.17% in the last quarter.

Free Cash Flow: CTSH’s Free Cash Flow is healthy, at about $2.1 billion. That number decreased from the quarter prior, when Free Cash Flow was $2.6 billion, and about $2.9 billion a year ago. The current number translates to a Free Cash Flow Yield of 5.45%.

Debt to Equity: CTSH has a debt/equity ratio of .06, which is extremely low and a good reflection of the company’s very conservative approach to leverage. Their balance sheet shows about $1.85 billion in cash and liquid assets against about $645 million in long-term debt. Their operating profile and high liquidity are good indications CTSH has the financial flexibility to adapt to ongoing changes in the markets it operates in; but it should be noted that cash has decreased over the last six months from $2.7 billion to its current level. That is a red flag that, along with the declining Free Cash Flow pattern, raises concern.

Dividend: CTSH pays an annual dividend of $.96 per share, which at its current price translates to a dividend yield of about 1.25%. That is modest, but it is also much less than 50% of the stock’s earnings per share over the last twelve months – a conservative payout ratio that actually helps bolster the company’s balance sheet strength. It is also noteworthy that earlier this year, CTSH’s dividend was $.88 per share.

Price/Book Ratio: there are a lot of ways to measure how much a stock should be worth; but I like to work with a combination of Price/Book and Price/Cash Flow analysis. Together, these measurements provide a long-term, fair value target at about $72 per share. That means that the stock is moderately over valued, with -5% downside from the stock’s current price. It also puts its “bargain price” at around $58 per share.

Technical Profile

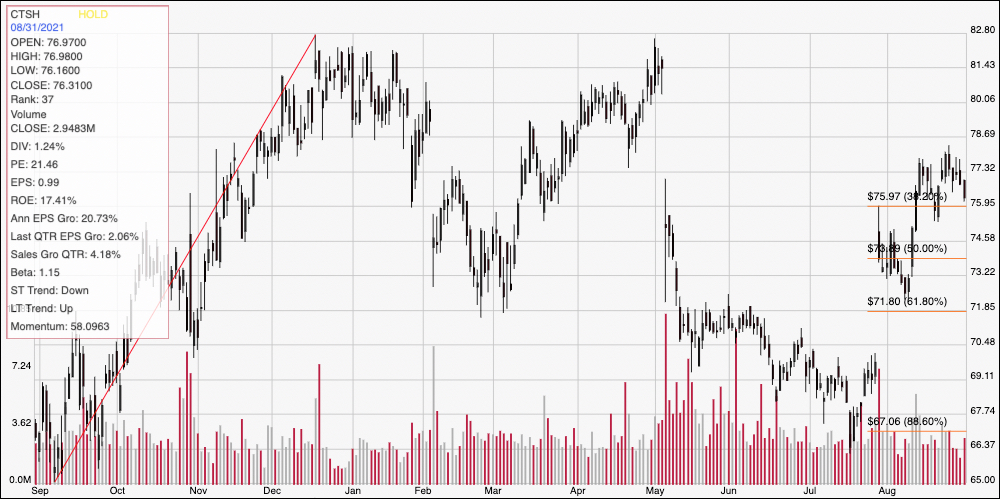

Here’s a look at the stock’s latest technical chart.

Current Price Action/Trends and Pivots: The chart above covers the last year of price activity; the diagonal red line traces the stock’s upward trend from its September 2020 low around $65 to its December 2020 peak at around $83. It also provides the baseline for the Fibonacci retracement lines shown on the right side of the chart. After finding a downward trend low point at around $67 in July, the stock rebounded strongly, pushing above every Fibonacci retracement line, including the 38.2% line this month. That line marks current support for the stock at around $76, with immediate resistance at around $78. A push above $78 per share should see upside to about $81.50 per share, while a drop below $76 could have downside to about $72, where the 61.8% retracement line sits before finding new support.

Near-term Keys: The stock’s fundamentals are very strong, showing that CTSH has weathered the difficulties of the past year well; however declines in Free Cash Flow as well as cash and liquid assets are a concern. The stock is overvalued right now, which means that there isn’t a strong argument to make right now for the stock as a useful, value-oriented investment; I would also look for reversals of the current decline in liquidity and Free Cash Flow before taking any potential value opportunity seriously. If you prefer to work with short-term strategies, a push above $78 could offer an interesting signal to buy the stock or to work with call options, using $81.50 providing a useful, quick-hit profit target on a bullish trade. A drop below $76 would offer a strong signal to consider shorting the stock or buying put options; in that case, next support at around $72 offers a very useful profit target for a bearish trade.