One of the big themes this year of the “reopening” trade has come from a generally expected increase in consumer activity in activities that were almost completely restricted in 2020 such as travel to take vacations. That generally implies consumer demand for airlines, hotel bookings, and resorts should also increase, which is typically good news for the Energy sector.

That anticipation for increased demand early in the year – followed by indicators that confirmed demand for these activities was actually increasing – has pushed big increases in price for the commodity; from a starting point below $50 per barrel in January, for example West Texas Intermediate (WTI) crude is now sitting at around $72 per barrel. The increase is generally also being seen at the pump – which is generally good news for stocks in the Energy sector. One of the possible exceptions, however applies to oil refiners, who have the difficult role of trying to find a balance between cost-efficiency in crude and passing cost increases downstream through the energy supply chain. Increased prices of the raw commodity generally make that task more difficult and weigh on the profitability of refiners, including the largest, industry leaders.

Phillips 66 (PSX) is one of the largest refiners in the United States, and that came into 2020 in better position than most other companies in its industry. While oil refining is its primary business, it also had the foresight to position itself before the downturn, diversifying into crude storage and shale pipeline projects to alleviate congestion in the Permian Basin and Eagle Ford areas, where a large amount of U.S. shale has been held up by pipeline limitations. They were also aided by an increase in consumer demand in its chemicals business, including packaging for cleaning products. Those are areas that helped to minimize, while not entirely offset the near-term effect of cratered refined crude demand in 2020. After finally finding a bottom in November of last year at around $43, the stock rallied into an extended upward trend that peaked in June at around $94.50 per share. The stock has dropped into a downward trend from that point, falling in price by about -30%. Recent earnings reports have suggested that the impact of reduced demand, along with more recent, increasing refining costs have had an impact on the company’s fundamental strength this year; but they also seem to show that the company has begun to turn the corner back to profitability. Does that mean the stock’s downturn in the last three months is actually a new opportunity for value investors? Let’s find out!

Fundamental and Value Profile

Phillips 66 is an energy manufacturing and logistics company with midstream, chemicals, refining, and marketing and specialties businesses. The Company operates through four segments: Midstream, Chemicals, Refining, and Marketing and Specialties (M&S). The Midstream segment gathers, processes, transports and markets natural gas, and transports, stores, fractionates and markets natural gas liquids (NGLs) in the United States. The Chemicals segment consists of its equity investment in Chevron Phillips Chemical Company LLC (CPChem), which manufactures and markets petrochemicals and plastics. The Refining segment buys, sells and refines crude oil and other feedstocks at refineries in the United States and Europe. The M&S segment purchases for resale and markets refined petroleum products, such as gasolines, distillates and aviation fuels, primarily in the United States and Europe, as well as includes the manufacturing and marketing of specialty products, and power generation operations. PSX’s current market cap is $28.8 billion.

Earnings and Sales Growth: Over the last twelve months, earnings increased by 200% (not a typo), while sales increased more than 149%. In the last quarter, earnings improved by almost 164%, while sales were a little more than 27% higher. After spending most of the last year in negative territory, the company’s margin profile has also turned positive; over the last twelve months, Net Income was -2.05% of Revenues, and improved to 1.1% in the last quarter.

Free Cash Flow: PSX’s free cash flow was $1.375 billion for the trailing twelve month period. This measurement confirms the turnaround I just described using Net Income, and provides a more comprehensive view of the company’s recovery, as Free Cash flow was -$163 million in the quarter prior, -809 billion six months ago, and -$526 million a year ago.

Debt to Equity: PSX has a debt/equity ratio of .63, a generally conservative number that indicates the company operates with a conservative philosophy about leverage. Their balance sheet shows $2.2 billion in cash and liquid assets versus $12.9 billion in long-term debt. It is worth noting that in July of this year, long-term debt was almost $16 billion while cash was around $1.3 billion.

Dividend: PSX pays an annual dividend of $3.60 per share, which translates to a yield of almost 5.5% at the stock’s current price. Management has maintained the dividend throughout the pandemic’s challenges, and appear to have managed to reverse the negative profitability trend from prior quarters without resorting to more drastic measures like cutting or eliminating the dividend to preserve cash.

Price/Book Ratio: there are a lot of ways to measure how much a stock should be worth; but I like to work with a combination of Price/Book and Price/Cash Flow analysis. Together, these measurements provide a long-term, fair value target around $84.50 per share. That suggests that PSX is very nicely undervalued, by about 28% at the stock’s current price. It is also worth noting that in July, this same analysis yielded a long-term target price at around $52 per share.

Technical Profile

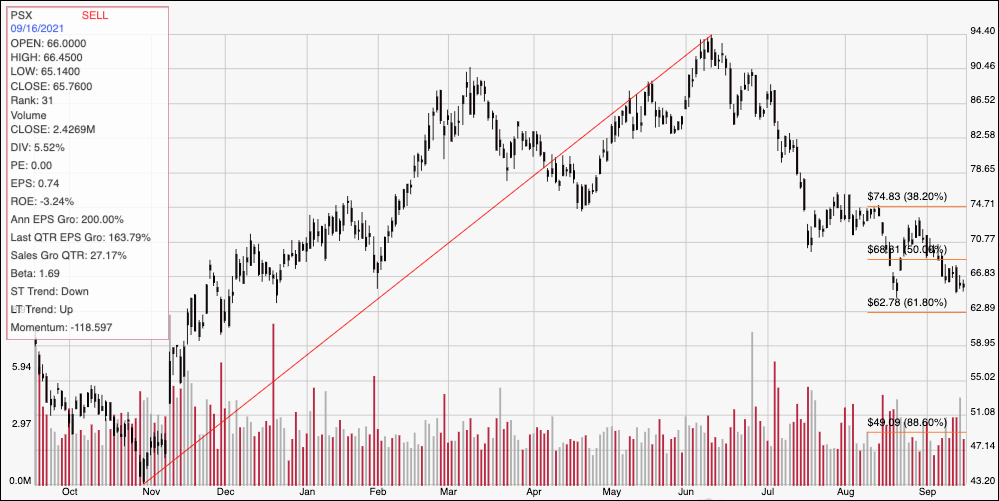

Here’s a look at the stock’s latest technical chart.

Current Price Action/Trends and Pivots: The chart above shows the stock’s price action over the past year. The red diagonal line traces the stock’s upward trend from November 2020 to its peak in June at around $94.50. It also provides the baseline for the Fibonacci retracement lines on the right side of the chart. The stock’s downward trend from that level is clear, but appears to have solid support from the 61.8% retracement line at around $63; that level provided a temporary bounce for the stock in August, and more recently bearish momentum appears to be slowing as the stock nears that level again. Immediate resistance is around $71, based on pivot activity in August, July, and late in 2020. A push above $71 should find next resistance at around $75, where the 38.2% retracement line waits, while a drop below $63 could have downside to anywhere between $58 and $55 based on pivots in November and October of 2020.

Near-term Keys: Given the improving fundamental picture that I think accurately reflects not only the challenges PSX has been dealing with for the past year and a half, but also their ability to navigate them successfully, it isn’t hard to understand the stock’s undervalued status. I also think that means that the stock’s current decline is a sign of increasing long-term opportunity, even though it is still unclear whether the downward trend has run its course. If you prefer to work with short-term trading strategies, you could use a drop below $63 as a strong signal to consider shorting the stock or working with put options, with $58 acting as a very attractive initial bearish profit target, or $55 if bearish momentum accelerates. A bounce off of support anywhere between the stock’s current price and $63 could also act as an interesting, if counter-trend bullish signal; in that cases, you could consider buying the stock or working with call options, using $71 as an excellent profit target on a bullish trade.