China’s financial markets are nearing “peak stress” levels, with worries mounting over its highly leveraged property sector as the saga around troubled developer China Evergrande Group plays out.

And investors shouldn’t expect a sustained bounce in the country’s equity market until the credit cycle turns for the better, said analysts at Danske Bank.

But assets indirectly linked to the world’s second-largest economy have yet to feel the spillover effects of China’s economic slowdown, they also warned, in a Friday note.

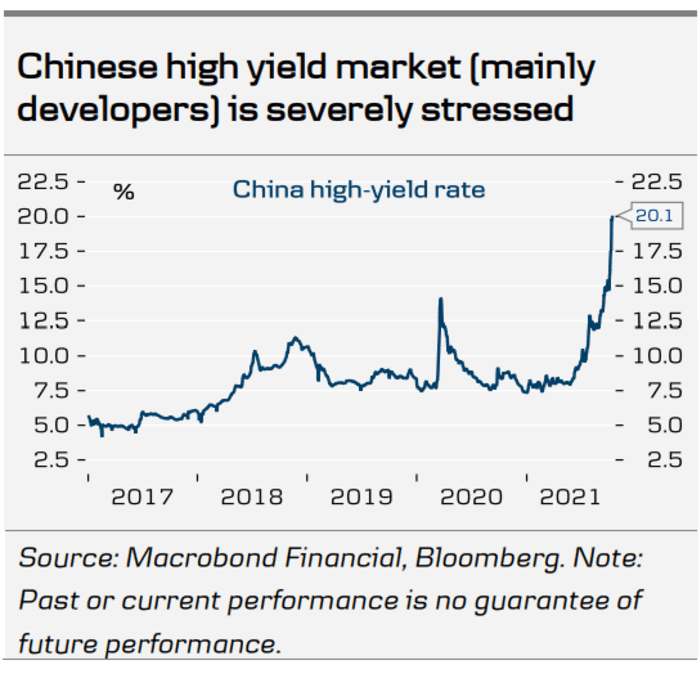

“While Chinese equity markets have been more stable lately, the stress in credit markets for developers have continued unabated with rates on high yield credit reaching new highs by the day,” wrote Copenhagen-based Allan von Mehren and Lars Sparresø Merklin (see chart below).

Danske Bank

Evergrande the highly leveraged developer with more than $300 billion in debt, has been in the spotlight, reportedly missing several coupon payments in recent weeks and in danger of being declared in default as grace periods for those payments run out. Evergrande’s chief executive, Xia Haijun, was holding talks in Hong Kong with creditors and investors over a restructuring and potential asset sales, Reuters reported Friday, citing two persons familiar with the matter.

A selloff last week for dollar-denominated bonds of Chinese developers was triggered after luxury developer Fantasia Holdings Group Co. failed unexpectedly to repay $206 million in dollar bonds that matured on Oct. 4.

Amid fears of a spillover, China’s central bank on Friday piped up to say that threats to the financial system from the property sector, which are estimated to account for nearly 30% of the country’s gross domestic product once upstream and downstream links are taken into account, were controllable, The Wall Street Journal reported, citing state media outlets.

Zou Lan, head of financial markets at the People’s Bank of China, said officials were urging Evergrande to speed up asset disposals and resume projects to protect the interests of home buyers, the report said. The official said financial authorities, the housing ministry and local governments would work together to provide funding support so stalled projects could restart.

The Danske analysts noted that big state banks were told to ease restrictions on mortgage lending and were allowed to securitize loans again, in an effort to underpin home sales.

They said Beijing will likely take steps soon to “unfreeze” credit markets, “as very few developers can survive this kind of funding and liquidity squeeze for long.”

Among the options, the PBOC could cut the reserve requirement ratio and direct big state banks to start buying high-yield bonds, they said. The analysts argued that if conditions calm, purchasing bonds at 20% would likely turn out to be a “quite favorable” investment for the banks, while private investors would also be encouraged to begin buying if the government gets involved.

They also see more direct bank lending to developers, with authorities likely to loosen regulations that crimped loans last year.

However, the Danske analysts and other China watchers have argued that Evergrande and the property sector were unlikely to threaten a “Lehman moment,” a reference to the 2008 collapse of Lehman Brothers that temporarily froze global credit markets and marked the bleakest phase of the global financial crisis. That’s because the government’s ability to dictate the actions of lenders and others give Beijing more flexibility.

But the crackdown on excesses in the property sector and other factors were still likely to ensure a continued slowdown in China’s economy.

“Even following an orderly restructuring of the worst-affected developers with minimal contagion to the financial system, construction activity would still almost inevitably slow much further. As we have warned for some time, that’s the logical consequence of the ‘three red lines’ policy imposed on developers last year, plus the enormous demographic headwinds that the sector faces,” said Oliver Jones, senior markets economist at Capital Economics, in an Oct. 12 note.

The Danske analysts emphasized that there’s a long way to go from peak financial stress to restarting the credit cycle.

“For Chinese equities, this may simply be a period of time where we see more sideways moves, awaiting the next large cyclical reboot of credit,” they wrote. “For assets which are more indirectly linked to Chinese assets and the credit cycle, we suspect this will mean little.”

For example, the euro is likely to continue falling versus the dollar “as the effects of historical Chinese tightening moves through the global manufacturing

chains.”