As a value investor, the search for stocks trading at useful values never really stops, no matter whether the market is sitting at new all-time highs such as what we’ve been seeing since mid-October, or if it has been following a sustained downward trend. Extended conditions tend to elevate valuations across the board, which makes the process more complicated for investors like myself. One of the methods I’ve found useful to find value even under extended bullish conditions is to start looking through sectors or industries that most have been dismissing for one reason or another.

The Auto industry has been experiencing quite a bit of bearish pressure for most of the past few years. Even before COVID-19 became a global health and economic crisis, sales were down globally, reflecting economic slowing in various parts of the world as well as the effects of an extended trade war between the U.S. and China that held investor’s attention through most of 2018 and all of 2019. Just as that headwind seemed ready to fade away with a trade deal at the end of 2019, the global economy ground to a halt amid massive quarantine and shelter-in-place orders that closed down businesses and sent consumers home to limit the spread of coronavirus. For most of this year, the industry continued to struggle as sales remained tepid, even though stocks in the industry have generally performed well. The exception to those unimpressive sales results come from the emerging electric vehicle segment, which has been getting more and more market buzz throughout the past year and a half.

BorgWarner Inc. (BWA) is an example of a U.S. company that provides parts and services to major auto manufacturers, and that until a couple of years ago I wouldn’t have considered as having a significant role in the electric vehicle segment. At the beginning of 2020, however, the company announced it had entered into an agreement to acquire Delphi Technologies. The deal closed in October of 2020, giving the company exposure and opportunity in hybrid and electronic vehicles, which I think puts the company at an interesting intersection of future growth with established presence and strength. In fact, BWA’s most recent reports indicate that this new segment has provided the biggest lift to the company’s sales and earnings over the past year. BWA agreed to pay $3.3 billion for the deal, which some analysts criticized as “paying too much” at the time; but I think that the company’s ability to pay down debt from that deal, along with the major contributions this segment is now providing to the bottom line really confirm that it was simply the price they had to pay to gain entry into the next important source of industry growth.

Even before that deal was announced, the stock began a strong downward trend in November of 2019, dropping from a peak at around $47 to a March 2020, bear market low at around $17 per share. The Delphi deal notwithstanding, another remarkable thing about BWA is that while the pandemic absolutely had an impact on the company, its earnings reports throughout the pandemic show that the company actually managed to absorb the initial blow better than most of its industry brethren. The stock rallied from its March 2020, $17 low to a peak at around $55.50 at the end of May this year before dropping into a downward trend that found bottom in September at around $42, The stock has picked up momentum since then pushing to $48 in October, and again in the last week. It is currently hovering a little below that point, but a new bullish push could extend the stock’s rally into a legitimate new upward trend. What does that mean for the stock’s value proposition? Let’s dig in.

Fundamental and Value Profile

BorgWarner Inc. is engaged in providing technology solutions for combustion, hybrid and electric vehicles. The Company’s segments include Engine and Drivetrain. The Engine segment’s products include turbochargers, timing devices and chains, emissions systems and thermal systems. The Engine segment develops and manufactures products for gasoline and diesel engines, and alternative powertrains. The Drivetrain segment’s products include transmission components and systems, all-wheel drive (AWD) torque transfer systems and rotating electrical devices. The Company’s products are manufactured and sold across the world, primarily to original equipment manufacturers (OEMs) of light vehicles (passenger cars, sport-utility vehicles (SUVs), vans and light trucks). The Company’s products are also sold to other OEMs of commercial vehicles (medium-duty trucks, heavy-duty trucks and buses) and off-highway vehicles (agricultural and construction machinery and marine applications. BWA has a current market cap of about $11.2 billion.

Earnings and Sales Growth: Over the last twelve months, earnings declined a little more than -9%, while revenues improved nearly 35%. In the last quarter, earnings declined by almost -26% while sales were about -9.1% lower. The company’s margin profile is generally narrow, but is showing signs of weakness; over the last twelve months Net Income as a percentage of Revenues was 5.07%, and eroded to 2.81% in the last quarter.

Free Cash Flow: BWA’s free cash flow is generally healthy, but faded in the last quarter, at $463 million over the last year. That marks a drop from $845 million in the last quarter and $723 million a year ago. The current number translates to a Free Cash Flow Yield of 4.12%.

Debt to Equity: BWA has a debt/equity ratio of .61. This is a very manageable number that suggests the company should have no trouble servicing their debt, even with the declines mentioned above. Their balance sheet shows $1.51 billion in cash and liquid assets against about $4.3 billion in long-term debt. The long-term debt number is made up mostly of debt assumed at the beginning of 2020 ahead of finalization of its Delphi acquisition.

Dividend: BWA’s annual divided is $.68 per share and translates to a yield of 1.45% at the stock’s current price. It is also noteworthy that BWA has maintained its dividend, where other companies in the industry that previously paid useful dividends have cut or suspended their dividend payouts to help weather the pandemic.

Price/Book Ratio: there are a lot of ways to measure how much a stock should be worth; but I like to work with a combination of Price/Book and Price/Cash Flow analysis. Together, these measurements provide a long-term, fair value target around $53 per share. That means that BWA is undervalued by 14%. It is also worth noting that at the end of 2020, my price target for this stock was around $42, but this number also declined from the last quarter, when my analysis translated to a fair value price of $54.

Technical Profile

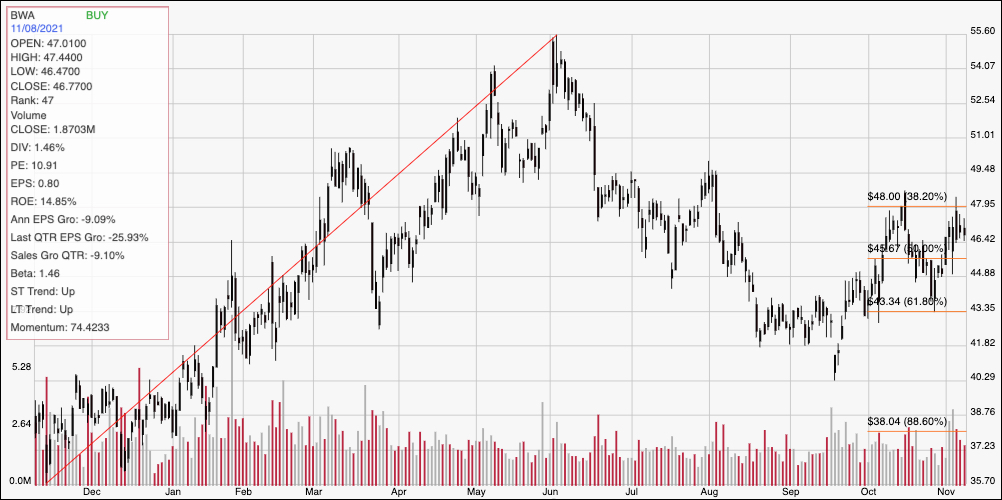

Here’s a look at the stock’s latest technical chart.

Current Price Action/Trends and Pivots: The red diagonal line measures the length of the stock’s upward trend over the past year, and also informs the Fibonacci trend retracement lines shown on the right side of the chart. The stock’s downward trend found bottom at the beginning of August and started to reverse in September. The stock pushed to a high at around $48, inline with the 38.2% retracement line in October and revisited that level a few days ago, marking immediate resistance, with current support at the 50% retracement around $45.50. A push above $48 will see next resistance at around $49.50, with additional upside to $51 if buying activity increases. A drop below $45.50 should have secondary support a little above $43 where the 61.8% retracement line currently sits.

Near-term Keys: BWA’s strengthening fundamental profile has weakened in the last quarter, which makes the stock less useful as a practical value-based opportunity. If you prefer to work with short-term strategies, you could use a push above $48 as a signal to buy the stock or work with call options, looking for a peak at around $49.50 as an initial profit target on a bullish trade and $51 above that if bullish momentum picks up. A drop below $45.50 would be a useful sign to think about shorting the stock or buying put options, with $43 providing a good target to close a bearish trade.