In the never-ending search for useful investing opportunities, I’ve learned that it’s good to look for ways to expand my watchlist beyond the normal scope of the stocks I’ve been following and have become familiar with. Adding new stocks to my list from time to time is a good way to keep things fresh and interesting. It’s also useful in making sure that the fundamental and value-based metrics on which I’ve come to rely most heavily aren’t being unfairly skewed by the emotional bias that comes from working with the same stocks over and over again.

There are a lot of ways to find new candidates that might be useful for keeping your money working for you, and I’ve learned not to dismiss any of them too quickly. From water cooler talk with a friend or colleague, to looking up the company that makes a favored brand, or even to listening to talking heads on market news media offer their opinions about current market conditions, they can all be useful in uncovering new places to put your money to work. It’s true that, oftentimes you should take that information with a healthy dose of skepticism – but it’s also true that sometimes those sources can spark an idea that leads you to a very good investing decision.

When I talk to people about one of my favorite methods for finding new opportunities, I inevitably start to talk about the California Gold Rush that started in 1848. To me, the most fascinating part of one of the really colorful periods of American history isn’t about the miners that dug and panned their way to fortunes large and small – it’s the savvy businesspeople that stayed in town and provided the supplies, tools, and other goods and services those miners needed. It’s always made more sense to me to look for a way to be the one selling the shovel, pickaxe and wheelbarrow than the one that breaks his back using them.

That mindset has served me pretty well as a long-term, fundamental investor as well as a bit of a contrarian with a clear preference for deeply discounted stocks. It’s helped me learn to pay attention to the sectors and industries that often get the most attention from investors and media types, and drill down to the sub-industries and related sectors that supply and support them. Like the people selling shovels and whatnot to gold miners, these companies often get overlooked, but can provide excellent opportunities for both long-term growth and useful value.

One of the market trends that has been getting an increasing amount of attention for the past few years is in electric vehicles. It’s easy to focus on companies like Tesla, Inc. (TSLA), NIO Inc. (NIO) and others because they are the companies producing the final product – the vehicle you get to slide behind the wheel and experience what it’s like to drive the “next big thing.” My tendency to look for the businesses that provide and support those manufacturers prompts to pay less attention to those stocks because they are the ones that everybody else is focusing on so I can find other companies those manufacturers are going to be relying on.

Gentex Corp (GNTX) is an interesting example of a company that all automakers rely on, but that you probably haven’t heard about. This company’s specialty is on automatic-dimming rearview mirrors and electronics for the auto industry, as well as dimmable aircraft window and fire protection products. This is a company with a very specific niche that benefits from broad strength in the overall auto industry – which hasn’t been happening so much for the past couple of years – as well as the general shift towards electric vehicles. Semiconductor shortages that pre-date the pandemic are a risk element that has weighed on every part of the industry, and on GNTX’s results; but even with those pressures, this is a company with a healthy operating profile that is bolstered by a healthy balance sheet with next to zero long-term debt. The market has recognized those strengths over the past couple of months, pushing the stock from a 52-week low at around $30 to a current price a little below $37. Could that bullish strength also translate to a useful opportunity to work with it on a long-term, value-oriented basis? Let’s find out.

Fundamental and Value Profile

Gentex Corporation is a designer, developer, manufacturer, marketer, and supplier of digital vision, connected car, dimmable glass, and fire protection products. The Company provides automatic-dimming and non-automatic-dimming rearview mirrors and electronics for the automotive industry; dimmable aircraft windows for the aviation industry; and commercial smoke alarms and signaling devices for the fire protection industry. The Company’s business segment involves designing, developing, manufacturing, and marketing interior and exterior automatic-dimming automotive rearview mirrors that utilizes electrochromic technology to dim in proportion to the amount of headlight glare from trailing vehicle headlamps. Within this business segment, the Company also designs, develops and manufactures various electronics that are value added features to the interior and exterior automotive rearview mirrors as well as electronics for interior visors, overhead consoles, and other locations in the vehicle. GNTX has a current market cap of about $8.7 billion.

Earnings and Sales Growth: Over the last twelve months, earnings declined by -33.33%, while revenues dropped nearly -16%. In the last quarter, earnings were -11.11% lower, while revenues decreased by -6.64%. The company’s margin profile is healthy, but has deteriorated in the most recent quarter; over the last twelve months, Net Income was 22.81% of Revenues, but weakened to 19.18% in the last quarter.

Free Cash Flow: GNTX’s free cash flow is generally healthy, at about $378.42 million over the last year. That translates to a modest Free Cash Flow Yield of 4.67%. It also marks a decrease from the last quarter, when Free Cash Flow was a little over $472.3 million.

Debt/Equity: The company’s Debt/Equity ratio is 0, reflective of the fact GNTX carries zero long-term debt. GNTX’s balance sheet also shows $276.9 million in cash and liquid assets in the last quarter. This number has decline from the quarter prior, when cash was $366.83 million, and $481.88 million two quarters ago. The decline in liquidity is running in parallel with their declining Free Cash Flow, and is a concern. Their operating profile indicates that profits are sufficient to service their debt.

Dividend: GNTX’s annual divided is $.48 per share and translates to a yield of about 1.31% at the stock’s current price.

Price/Book Ratio: there are a lot of ways to measure how much a stock should be worth; but I like to work with a combination of Price/Book and Price/Cash Flow analysis. Together, these measurements provide a long-term, fair value target around $22 per share. That means the stock is overvalued at its current price, by about -41%, with a useful value price down at around $17 per share.

Technical Profile

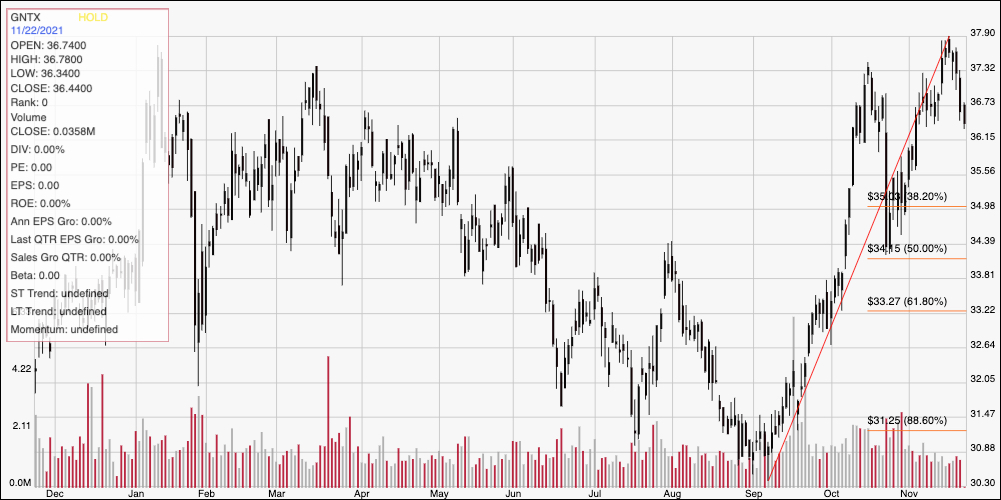

Here’s a look at the stock’s latest technical chart.

Current Price Action/Trends and Pivots: The chart above shows the last year of price activity for GNTX. The red diagonal line traces the stock’s upward trend from a September, downward trend low at around $30 to its peak earlier this month at around $38. It also provides the baseline for the Fibonacci retracement lines shown on the right side of the chart. The stock has dropped off of that peak in the last week or so, and appears to be approaching expected, current support at around $36 based on pivot activity at multiple points in the first quarter of 2021. Immediate resistance is at the stock’s last peak at $38. A drop below $36 should find next support at the 38.2% retracement line, which is currently sitting around $35, with additional downside to about $34 around the 50% retracement line if bearish momentum accelerates. A bounce off of support around $36, however should have immediate room to at least $38, with additional upside to about $40 (adding the current, $2 distance between support and resistance to the stock’s 52-week high) if buying activity picks up.

Near-term Keys: GNTX’s fundamentals are solid, but the declining patterns in Free Cash Flow, cash and liquid assets, and Net Income are all red flags. Along with the fact that the stock is significantly overvalued right now, I think those are all good reasons to put GNTX aside if you’re looking for a useful long-term, value-oriented opportunity. If you prefer to focus on short-term trading strategies, a bounce off of $36 could offer a signal to think about buying the stock or working with call options, using $38 as a good initial profit target, and $40 providing additional upside if bullish momentum accelerates. You can also use a drop below $36 as a signal to consider shorting the stock or buying put options; but keep in mind that with next support expected around $35, you’ll need to be ready to take profits quickly.