One of the things I like about value investing is that it complements a natural tendency I’ve had since childhood, which is go against the grain of what people say I should do or want me to do. Growing up, that attitude got me into a lot of trouble – but as an investor it has also helped me figure out how to find opportunities that the average investor, and certainly the talking heads on market media channels simply aren’t paying attention to. A big part of the reason I think that is true is because more often than not, the best opportunities to uncover real value comes when a stock can be seen at the low end of yearly or historical ranges.

Looking for stocks at the low side of their historical ranges generally increases the odds that the stock will represent a good bargain – but these are also stocks that growth-focused investors and traders treat as radioactive, because even the newest, least experienced investor already has it drilled into their head that a stock that has already been going up is more likely to keep going up. That is often true, but it also ignores the flip side, which is that since every stock experiences highs and lows, no bullish rally lasts forever.

Extending the logic I just described also means that even the most drastic downward slide will eventually find a turning point, and that is where the value hunters with the same kind of contrarian, go-against-the-grain tendency that I have learned to embrace in a positive way are able to find opportunity. That is especially true if the company’s fundamental profile is strong; the combination of fundamental strength with bearish price activity often means that the stock is priced well below what the “intrinsic” value of the underlying business actually is.

The opposite logic to what I just described is also true. Value seekers tend to be naturally drawn to stocks that have been following extended downward trends because these are the kinds of situations that are most likely to translate to useful value; but the caveat is that the underlying fundamental strength of the company’s business has to be strong enough to suggest that the stock’s current price represents a discount. It isn’t enough simply to see a stock in a downward trend and so to assume that the value is there. That’s why I’ve learned to combine price action, fundamental strength, and valuation analysis into a three-pronged approach to determine whether I think a stock represents the right kind of opportunity I need.

Corning Inc. (GLW) may be just the kind of stock right now that I’m talking about. If you’re not familiar with the company name, I’m willing to bet you are familiar with one of their most popular products – Gorilla Glass, which is used in a variety of applications and industries, but might be most easily recognized for its place in the automotive industry and in telecommunications, where for example its Ceramic Shield is used exclusively for the iPhone 12. The stock has been following an extended downward trend since April of 2021, when it peaked at almost $47. That trend bottom in late November at around $35, and the stock has mostly been consolidating since then – which is often a technical indication that the previous trend could be poised to reverse and that suits my value-focused mindset very nicely. The question, of course is whether the company’s fundamentals are also strong enough to suggest that the stock’s decline over the last nine months now make GLW a truly attractive value target. Let’s dive in to find out.

Fundamental and Value Profile

Corning Incorporated is a materials science technology and innovation company. The Company’s segments include Display Technologies, Optical Communications, Environmental Technologies, Specialty Materials and Life Sciences. The Display Technologies segment manufactures glass substrates for flat panel liquid crystal displays and other high-performance display panels. The Optical Communications segment manufactures carrier network and enterprise network components for the telecommunications industry. The Environmental Technologies segment manufactures ceramic substrates and filters for automotive and diesel applications. The Specialty Materials segment manufactures products that provide more than 150 material formulations for glass, glass ceramics and fluoride crystals. The Life Sciences segment manufactures glass and plastic labware, equipment, media, serum and reagents enabling workflow solutions for drug discovery and bioproduction. GLW’s current market cap is $32.8 billion.

Earnings and Sales Growth: Over the last twelve months, earnings increased a little more than 30% while revenue grew by about 20.5%. In the last quarter, earnings grew by 5.66%, while revenues were 3.26% higher. The stock’s operating profile over the last twelve months is healthy, with Net Income at 12.15% of Revenues, and decreasing only somewhat to 10.26% in the last quarter.

Free Cash Flow: GLW’s free cash flow is healthy, at $1.78 billion. This number translates to a Free Cash Flow Yield of 5.48%. I also marks a significant increase over the past year, when Free Cash Flow was $840 million.

Debt to Equity: GLW has a debt/equity ratio of .57, which reflects a conservative approach by management to leverage. Their balance sheet also shows a little over $2.2 billion in cash and liquid assets versus $7 billion in long-term debt. It’s worth noting that GLW’s debt has an average maturity of 10 years, giving the company plenty of time to work with, while also preserving liquidity and operating flexibility.

Dividend: GLW pays an annual dividend of $.96 per share, which translates to a yield of 2.51% at the stock’s current price. Management increased the dividend from $.88 per share at the beginning of 2021, confirming management’s confidence in the company’s prospects. I also think it should be noted that company also increased their dividend at the beginning of 2020 and maintained it throughout that year while still managing its way through the various difficulties the pandemic has imposed on the entire economy.

Price/Book Ratio: there are a lot of ways to measure how much a stock should be worth; but I like to work with a combination of Price/Book and Price/Cash Flow analysis. Together, these measurements provide a long-term, fair value target around $48 per share. That suggests that GLW is nicely undervalued, with 26% upside from its current price.

Technical Profile

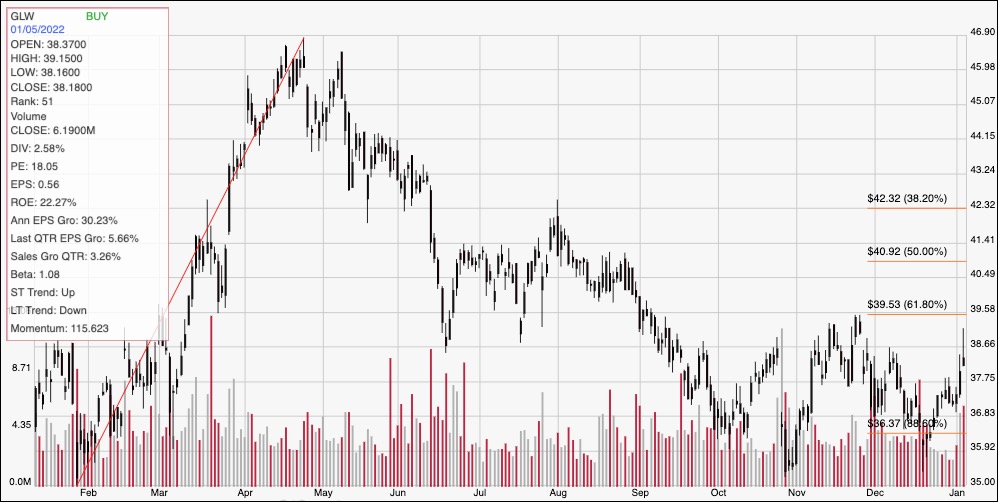

Here’s a look at the stock’s latest technical chart.

Current Price Action/Trends and Pivots: The chart above displays GLW’s price action over the past year. The diagonal red line traces the stock’s upward trend from a low point at around $35 last January to its April peak at around $47 per share; it also provides the reference for calculating the Fibonacci retracement levels indicated by the horizontal red lines on the right side of the chart. The stock’s downward trend finally found bottom in November at around $35, and it has picked up bullish momentum in the last couple of weeks as it has driven to about $38 as of this writing; but the stock has also been consolidating since October between immediate resistance at about $39 and current support around $36. The stock would actually need to push to about $40, above the 38.2% retracement line, to confirm a bullish trend reversal, but in that case could have short-term upside to about $41.50 to $42 before finding next resistance. A drop below $36 should see limited downside to the stock’s 52-week low around $35.

Near-term Keys: GLW is a stock that I think offers very intriguing possibilities for long-term, value-oriented investor. The company’s fundamentals are solid, with a stable, consistent dividend, and a very nice value proposition to boot. If you prefer to work with short-term trading strategies, I think the best signal would come from a push above $40, which would strongly indicate the stock’s longer, downward trend is reversing. In that case, consider buying the stock or working with call options, with an eye on $41.50 to $42 as good, quick-hit exit points, and $44 possible if buying activity increases. I don’t think GLW offers very good probabilities for bearish, momentum-based trading strategies right now, but if the stock pivots off of current resistance at around $39 and starts to move low, you could consider shorting the stock or buying put options, using current support at $36 as a practical exit target on a bearish trade.