Uncertainty in the financial markets, and in the economy is usually considered a bad thing, because it makes things more difficult and stressful for everybody. Fear about inflation, the likelihood of rising interest rates, and the continued impact of a pandemic that is now extending into its third year has taken a toll on the broad market this month, with all three major indices all approaching or recently passing legitimate correction territory. That is both a technical and emotional benchmark that puts a lot of investors on edge, and has prompted some analysts to start throwing around even scarier terms like “bear market” and “recession.”

I find it interesting that even when conditions are uncertain, there are companies in normally cyclical industries that find new ways to succeed. Sometimes that is planned, and sometimes it happens to be the opportunistic happenstance of being in just the right place at the right time. Some of the most obvious examples of what I mean since early 2020 have come from the Tech sector, with companies that offer a variety of cloud-based, remote collaboration and networking tools and solutions that proved to be the perfect way to keep much of corporate America running amid broad-based economic shutdowns and social restrictions.

Another unexpected element of opportunity that has emerged from the difficult conditions of the past two years has come from the Consumer Discretionary sector – an area of the market that usually suffers when basic economic indicators, like unemployment (which, at about 3.9% as of the last report, continues to trend lower, but is still a bit above pre-pandemic levels) demonstrate clear weakness in the broad economy. Stay-at-home orders in early 2020 included shuttering or limiting access to gyms, and changed work life for white-collar workers to long-term remote arrangements. That prompted an increase in demand for outdoor, active, and athletic apparel. The trend was apparently driven by remote workers who realized they could dress as comfortably as they wished to work from home while also finding creative ways to stay fit and healthy even though they might not have access to a local gym. This year, increasing vaccinations, continued positive progress in the unemployment trend and recovering local business and social activity have offered reasons for hope even as infections and hospitalizations from new COVID variants continue to strain capacity limits in the health care sector.

VF Corp (VFC) is a company that you might not recognize by its corporate name, but you almost certainly will by their brands. This is the company behind well-known apparel and footwear brands including Dickies, The North Face, Vans, and Timberland. It’s a better than even bet that you’ve bought their products before, and I’m even willing to go out on a limb and say that it’s a fair bet you have some of their products in your closet or dresser drawer right now; I know I do. Like just about every other stock in this sector, the company has had to absorb the complications and difficulties that come from an uncertain marketplace and economy; but they have also seen traction from their ability to position themselves as a performance-driven, lifestyle sports company. They also have managed to maintain a strong balance sheet even in the midst of pandemic conditions while dramatically reducing their reliance on department stores. This is also a company that enjoyed the distinction of being a ‘dividend aristocrat,’ having increased their dividend for 47 years in a row before the pandemic prompted management to reduce it.

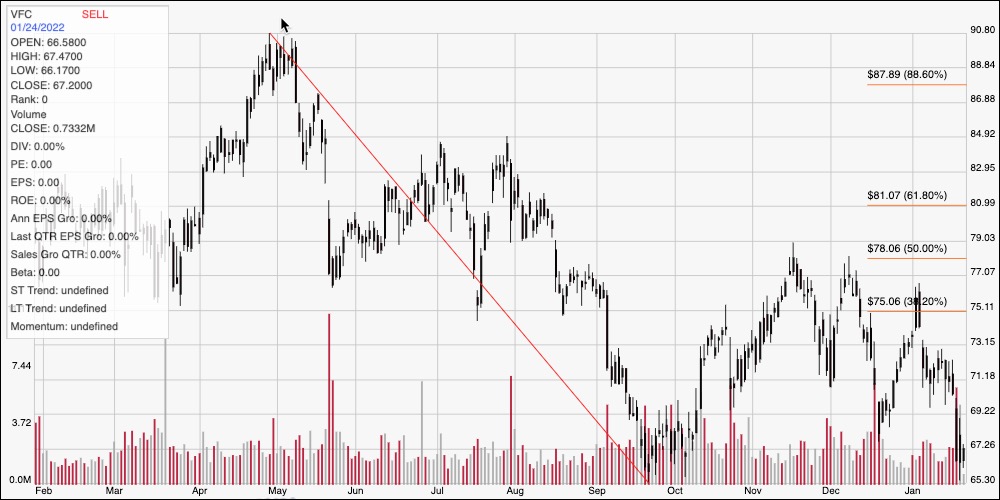

Since hitting a 52-week high price in April 2021 at around $91, the stock saw bearish momentum force the stock dramatically lower, hitting a downward trend low at around $65 in September. The stock rallied to a November peak at around $79 before dropping back again and bouncing between $69 and $77 through the rest of the year. From an early January high at around $75, the stock has picked up a lot of bearish momentum along with the market and is very close to its 52-week low. Could that mean the stock now offers a good opportunity for value-oriented investors to buy a good company at a nice price, or is the bearish momentum a sign that you should stay away for the time being? Let’s dig in and find out.

Fundamental and Value Profile

V.F. Corporation is engaged in the design, production, procurement, marketing and distribution of branded lifestyle apparel, footwear and related products. The Company’s segments include Outdoor & Action Sports, Jeanswear, Imagewear and Sportswear. It owns a portfolio of brands in the outerwear, footwear, denim, backpack, luggage, accessory, sportswear, occupational and performance apparel categories. Its products are marketed to consumers shopping in specialty stores, department stores, national chains, mass merchants and its own direct-to-consumer operations. Its direct-to-consumer business includes VF-operated stores, concession retail stores and e-commerce sites. Its brands sell products in international markets through licensees, distributors and independently-operated partnership stores. Its brands primarily include The North Face, Vans, Timberland, Wrangler, Lee, and Kipling. VFC has a current market cap of about $26.1 billion.

Earnings and Sales Growth: Over the last twelve months, earnings increased a little over 65.6%, while revenues grew by about 22.6%. In the last quarter, earnings were 311% higher, while sales grew by almost 46%. The last couple of quarters indicate the company’s margin profile has mostly absorbed the damage inflicted by COVID-19 and reversed to healthy, strengthening levels; Net Income as a percentage of Revenues over the last twelve months was 11.19%, and strengthened nicely to 15.14% in the last quarter.

Free Cash Flow: VFC’s free cash flow is healthy despite its decrease in the last quarter. It was $828.54 million in the last quarter versus $1.2 billion in the quarter prior. This is a number that had persisted in negative territory since the first quarter of 2017, and was -$217.12 million at the beginning of 2019. I find it encouraging that even with this quarter’s dip, Free Cash Flow has improved steadily from that point; in June 2020, for example Free Cash Flow was $626 million.

Debt to Equity: VFC’s debt/equity ratio is high, at 1.3. A big portion of that debt came in 2020 as the company borrowed heavily to bolster its cash reserves in order to manage its way through the health crisis. As of the last quarter, the company reported $1.36 billion in cash and liquid assets against about $4.7 billion in long-term debt. It should be noted that at the beginning of 2020, cash was around $1.3 billion versus $2.6 billion in long-term debt.

Dividend: VFC’s annual divided is $2.00 per share, which translates to a yield of 2.94% at the stock’s current price. in 2019, the dividend was $2.04 per share; however considering the difficulties imposed by pandemic conditions, the fact that the dividend has been maintained relatively close to that 2019 level is a useful sign of management’s commitment to delivering shareholder value. It is also worth noting that after the most recent earnings call, management increased the dividend from $1.96 per share.

Price/Book Ratio: there are a lot of ways to measure how much a stock should be worth; but I like to worth with a combination of Price/Book and Price/Cash Flow analysis. Together, these measurements provide a long-term target at about $64.25 per share. That suggests that despite the company’s fundamental strengths and the stock’s current, accelerating bearish momentum, the stock remains somewhat overvalued by about -3%, with a bargain price around $51.50 per share. It is also worth noting that in the last quarter of 2020, my analysis offered a fair value target of $46.50, and about $67 a quarter ago. While this doesn’t change the stock’s immediate overvalued status, I do take the overall increase as another sign of increasing fundamental strength.

Technical Profile

Here’s a look at the stock’s latest technical chart.

Current Price Action/Trends and Pivots: The red diagonal line traces the stock’s downward trend from a peak at around $91 in April of this year to its September low at around $65. It also provides the baseline for the Fibonacci retracement lines shown on the right side of the chart. The stock attempted to reverse its downward trend by rallying to about $79 in November, but dropped back and began to consolidate through the rest of 2021. Since the start of the new year, bearish momentum has picked up again and pushed the stock below that consolidation range, and just a few dollars from its 52-week low, putting current support at around $65 and immediate resistance at around $68. A push above $68 could have short-term upside to between $71 and $72 before finding next resistance, while a break below $65 could have downside to about $60.

Near-term Keys: I think VFC’s fundamental profile in the face of the past two year’s pandemic-induced economic conditions is a very interesting story – but unfortunately it doesn’t translate to a useful value as well. If you prefer to work with short-term strategies, a push above $68 could offer an interesting, if speculative signal to think about buying the stock or working with call options, using $71 as a practical bullish profit target. A drop below $65 would be a useful signal to consider shorting the stock or buying put options, with a practical profit target at around $60 on a bearish trade.