The Technology sector has been a bright spot throughout the past two years, and one of the big reasons that I think the economy has been pretty resilient during the COVID-19 pandemic. One of the reasons the sector has led the market for most of that time is because so much of the shift to remote, work-from-home operations for corporate America, contactless sales and delivery methods now being used by a lot of retail businesses, and many of the safety protocols factories and production facilities were forced to put in place are driven or enabled by technology solutions. That’s driven investors to flock to stocks that specialize in remote networking, conferencing and cloud-based solutions, including digital transaction handling and CRM services. Many of these companies have defied the broader economic trend and managed to post impressive results.

The market, and the Tech sector in general has been challenged to start the year, with persistent pressures on chip production and supply that have yet to fully abate, mixed with broader concerns about the pace of inflation and the potential hawkishness of Fed policy about raising interest rates. The start of February seemed to give the market a chance to think it had a handle on some of those questions, but the last week or so has increased uncertainty yet again as geopolitical pressures between Russia and Ukraine have not too surprisingly rattled global markets. That shouldn’t be too surprising, since the threat of war is something that is usually disruptive to global economic dynamics on multiple fronts. The interesting thing about the Tech sector, however is that while many of the companies whose focus is on providing the kind of remote and cloud-based technology services and solutions that I described to open today’s post haven’t been entirely immune from broad market uncertainty, they also seem to have shown some of the same resilience to current fears as they did during the most disruptive stages of the pandemic in 2020.

Cognizant Technology Solutions (CTSH) is a professional services company that works with companies in a variety of sectors that focuses on software development and digital platform engineering services for its clients. That puts CTSH in the IT Services industry, which is, at least in part, an area that has continued to see healthy demand as more companies have been forced to identify ways to use technology to shift their business focus. Economists are putting a big focus on companies with healthy balance sheets to help ride through any uncertainty that may extend into a longer-term period of time, and CTSH is company that, despite experiencing its own pressures over the course of the last two years, looks to fit that bill as well. From its own bear market low at around $40, the stock rallied to a peak in December 2020 at around $83. After dropping, then retesting its high in May of last year, the stock dropped to a low in mid-July at around $66 per share. From that point, the stock has moved into a new, strong bullish trend that peaked at the start of 2022 at around $92 per share, and then revisited that high early this month.

Uncertainty over the last two weeks has pushed the stock about -7.5% off that low as of this writing, which is consistent with broader market declines that are revisiting correction territory right now. The stock also appears to be hitting a good support level at around $86, which means that a new pivot and move higher off of that level could be a set up for a new buying opportunity for short-term traders. What about value? Are the stock’s latest fundamentals strong enough to suggest it could be a good value at its current price? Let’s find out.

Fundamental and Value Profile

Cognizant Technology Solutions Corporation is a professional services company. The Company operates through four segments: Financial Services, Healthcare, Manufacturing/Retail/Logistics, and Other. The Financial Services segment includes customers providing banking/transaction processing, capital markets and insurance services. The Healthcare segment includes healthcare providers and payers, as well as life sciences customers, including pharmaceutical, biotech and medical device companies. The Manufacturing/Retail/Logistics segment includes manufacturers, retailers, travel and other hospitality customers, as well as customers providing logistics services. The Other segment includes its information, media and entertainment services, communications and high technology operating segments. Its services include consulting and technology services and outsourcing services. Its outsourcing services include application maintenance, IT infrastructure services and business process services. CTSH has a current market cap of $45.1 billion.

Earnings and Sales Growth: Over the last twelve months, earnings increased by a little more than 64%, while sales increased by more than 14%. In the last quarter, earnings improved by 3.77% while Revenues growth was flat, but positive, at 0.7%. CTSH’s Net Income versus Revenue is healthy, at 11.55% over the last twelve months, and strengthening to 12.06% in the last quarter.

Free Cash Flow: CTSH’s Free Cash Flow is healthy, at about $2.22 billion. That number slipped just a bit from the quarter prior, when Free Cash Flow was $2.6 billion, and is below its $2.6 billion mark from a year ago. The current number translates to a Free Cash Flow Yield of 4.95%.

Debt to Equity: CTSH has a debt/equity ratio of .05, which is extremely low and a good reflection of the company’s very conservative approach to leverage. Their balance sheet shows about $2.7 billion in cash and liquid assets (up from $2.4 billion a quarter ago, and $1.8 billion in the quarter prior) against about $626 million in long-term debt. Their operating profile and high liquidity are good indications CTSH has the financial flexibility to adapt to ongoing changes in the markets it operates in. They are also using that flexibility to expand their digital services both organically, through in-house research and development, and inorganically via acquisition.

Dividend: CTSH pays an annual dividend of $1.08 per share, which at its current price translates to a dividend yield of about 1.27%. That is modest, but it is also much less than 50% of the stock’s earnings per share over the last twelve months – a conservative payout ratio that actually helps bolster the company’s balance sheet strength. It is also noteworthy that in the early part of 2021, CTSH’s dividend was $.88 per share, and $.96 per share prior to the last quarter when management announced the last dividend increase.

Price/Book Ratio: there are a lot of ways to measure how much a stock should be worth; but I like to work with a combination of Price/Book and Price/Cash Flow analysis. Together, these measurements provide a long-term, fair value target at about $75 per share. That means that the stock is overvalued, with -12% downside from the stock’s current price. It also puts its “bargain price” at around $60 per share.

Technical Profile

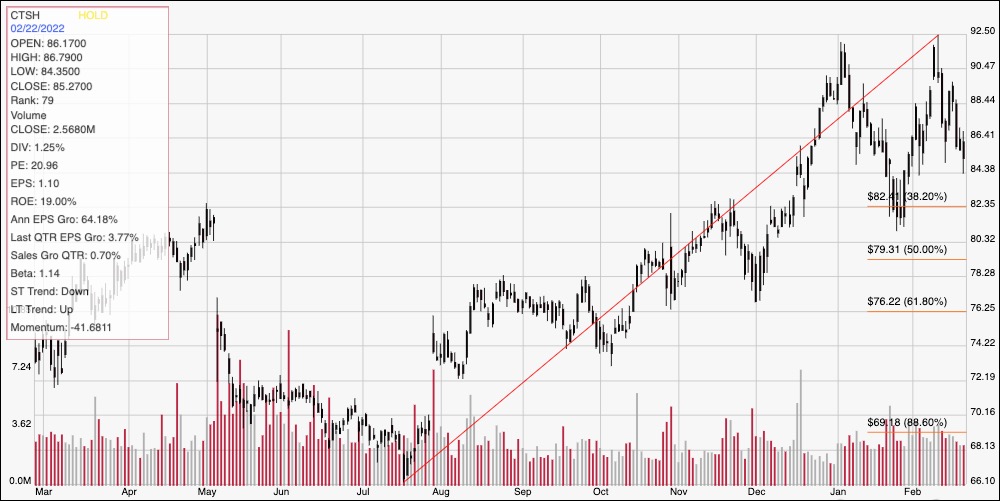

Here’s a look at the stock’s latest technical chart.

Current Price Action/Trends and Pivots: The chart above covers the last year of price activity; the diagonal red line traces the stock’s upward trend from its July 2021 low around $66 to its peak at the start of 2022 at around $92. It also provides the baseline for the Fibonacci retracement lines shown on the right side of the chart. The stock dropped off of that high, and then revisited it earlier this month, forming what many technicians like to call a “double top” formation that can be an early indicator for a reversal of the current, bullish trend. That puts a big focus on the stock’s next expected support point, which is around $82 based on the stock late January low, and support by pivot highs in November and early May of 2021. A drop below that level would provide clear confirmation that the stock’s trend has turned bearish, and should extend to somewhere between $79 and $78 before its next support level. I also have immediate resistance at around $88.50, with upside to retest the $92 high again if that level is broken. I frankly expect that level to provide a new, lower high at some point in the near future to further strengthen the argument the stock could be reversing its trend.

Near-term Keys: The stock’s fundamentals are very strong, showing that CTSH has weathered the difficulties of the past two years well; even so, the stock is overvalued right now, which means that there isn’t a strong argument for the stock as a useful, value-oriented investment. I also think that current market conditions make any kind of bullish short-term bet right very speculative. If you prefer to work with short-term strategies, a bounce off support at $82 could offer an interesting, albeit aggressive signal to buy the stock or to work with call options, with $88 providing a practical, quick-hit profit target on a bullish trade within the confines of current price activity. A drop below $82 would offer a strong signal to consider shorting the stock or buying put options; in that case, next support at around $79 to $78 offers a useful profit target for a bearish trade, with additional room at around $76 if selling pressure accelerates.