During the last two years, one of the most interesting sectors of the market to pay attention to has been the Consumer Discretionary sector. This is a sector that is driven by consumer spending, which is generally highest when the economy is healthy. The COVID-19 pandemic shuttered all kinds of economic activity through much of 2020 and pushed unemployment numbers to levels not seen in decades. These are the kinds of factors that typically spell trouble for retail spending, but unprecedented federal stimulus money, including extended unemployment benefits that actually motivated workers to avoid re-entering the workforce actually countered most of the expected, bearish aspects of pandemic-driven restrictions and slowdowns.

I attribute at least a portion of the demand side of the sector’s resilience during that period to a general shift in consumer behavior to exercise outside and engage in more outdoor activities. That gave stocks like Columbia Sportswear Company (COLM) a useful revenue base to weather the pandemic.

The company has seen material improvements in cash and liquid assets as well as free cash flow over the last two years that may have begun to moderate somewhat, but still remain well above pre-pandemic levels.

Over the last year, COLM’s stock price hasn’t seen the same kind of lift that its fundamentals have suggested should be in order; in fact, the stock has been following a long-term downward trend from a high at around $115 a year ago to a low in early March at around $83.50, with the stock now sitting just a little above that price as we move into the Good Friday weekend. That doesn’t sound very encouraging, but if you frame that downward trend against the contrasting view of the company’s fundamental strength, the picture actually becomes pretty attractive for a long-term investor.

From a macroeconomic perspective, I think that even with inflation increasing, and a fair amount of uncertainty about global conditions driven primarily by Russia’s unprovoked aggression in Ukraine, there is a lot to suggest that demand for outdoor lifestyle apparel and other goods is likely to remain healthy. COVID-19 isn’t going away, but appears to be moving to its endemic stage – where it is as much a part of “normal” as the flu, pneumonia, and the vaccinations and boosters that many of us already get on an annual basis against those diseases.

That implies social and other activities will largely remain uninterrupted even as occasional spikes and swells in infections are likely to recur. For the average consumer, that mean vacations, weekend getaways, and other outdoor activities should continue to see healthy levels of consumer engagement, which means that demand for the kinds of products COLM specializes in should remain healthy. Does that mean you should consider COLM as a useful, long-term investment? Let’s find out.

Fundamental and Value Profile

Columbia Sportswear Company is an apparel and footwear company. The Company designs, sources, markets and distributes outdoor lifestyle apparel, footwear, accessories and equipment under the Columbia, Mountain Hardwear, Sorel, prAna and other brands. Its geographic segments are the United States, Latin America and Asia Pacific (LAAP), Europe, Middle East and Africa (EMEA), and Canada. The Company develops and manages its merchandise in categories, including apparel, accessories and equipment, and footwear. It distributes its products through a mix of wholesale distribution channels, its own direct-to-consumer channels (retail stores and e-commerce), independent distributors and licensees. As of December 31, 2016, its products were sold in approximately 90 countries. In 59 of those countries, it sells to independent distributors to whom it has granted distribution rights. Contract manufacturers located outside the United States manufacture all of its products. COLM has a current market cap of $5.7 billion.

Earnings and Sales Growth: Over the last twelve months, earnings increased by almost 66%, while sales were about 23.4% higher. Over the last quarter, earnings increased about 57.25% while sales grew by almost 40.4%. This positive pattern is confirmed by the company’s operating profile; over the last twelve months, Net Income was 11.33% of Revenues, and strengthened to nearly 13.9% in the last quarter.

Free Cash Flow: COLM’s Free Cash Flow is healthy, at $319.66 million. This does mark a decline from a peak at around $434 million in the quarter prior and $351 million a year ago; however it should also be noted that prior to the pandemic, COLM’s Free Cash Flow was around $150 million. The growth seen over the last two years in this metric is notable and useful.

Debt to Equity: COLM has a debt/equity ratio of 0; they have little to no long-term debt, and $893.55 million in cash and liquid assets. Along with their best-in-class balance sheet, the company’s operating profiles suggest that COLM has no problem taking care of immediate cash needs, returning value to shareholders, and investing in future growth.

Dividend: COLM suspended its dividend in 2020 to preserve cash during the pandemic, but reinstated it after the first quarter of 2021, and raised it after their most recent earnings report to $1.20 per share. That compares favorably to its pre-pandemic payout, which was $.96 per share. At the stock’s current price, its current payout translates to a modest dividend yield of 1.36%. It is also worth mentioning that their annual dividend payout ratio is conservative, representing less than 25% of their annual earnings per share.

Price/Book Ratio: there are a lot of ways to measure how much a stock should be worth; but I like to work with a combination of Price/Book and Price/Cash Flow analysis. All together, these measurements provide a long-term, fair value target at around $118 per share. That means that the stock is very nicely undervalued right now, with 34% upside from its current price.

Technical Profile

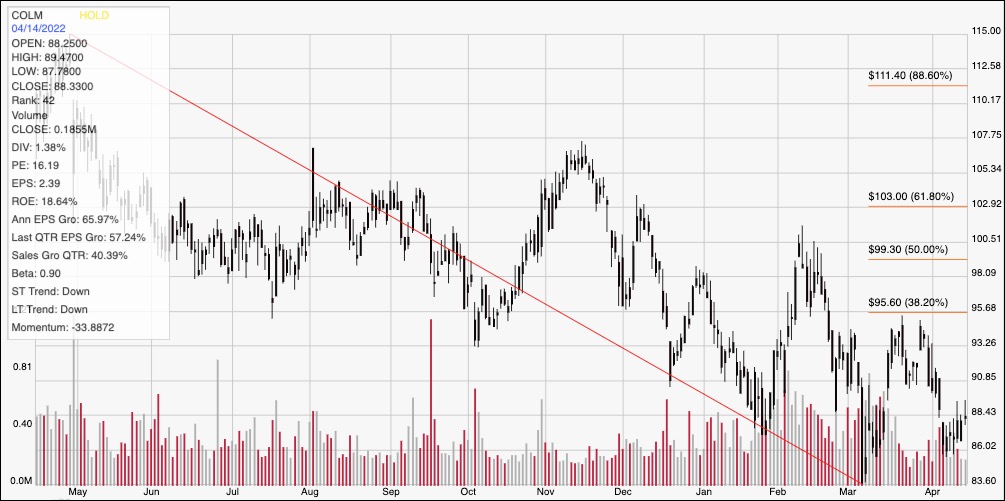

Here’s a look at the stock’s latest technical chart.

Current Price Action/Trends and Pivots: The chart above displays the last year of price activity; the red diagonal line traces the stock’s downward trend from an April 2021 high at around $115 to its low last month at around $83.50. It also provides the baseline for the Fibonacci retracement lines shown on the right side of the chart. After rallying to about the 38.2% retracement line twice before the end of March, the stock dropped back again to start April to find current support at around $86 per share. The stock has been moving higher from that point and appears to be hitting immediate resistance at around $88.50. A push above $88.50 should have near-term upside to about $91, with additional room to about $95 where the 38.2% retracement line sits and marks the most recent pivot high. A drop below $86 should see the stock retest next support around the 52-week low in the $83.50 range.

Near-term Keys: For the stock to resume its longer-term upward trend in the short-term, it would have to break above $95.50 with considerable buying volume to provide momentum and strength; however if the stock pushes above $88.50, and you don’t mind being aggressive, you could think about buying the stock or working with call options, using $91 for a quick hit profit target, and $95 possible if buying momentum remains strong. A drop below support at $86 would be a strong signal to consider shorting the stock or to buy put options, with $83.50 providing a practical profit target on a bearish trade. The stock’s value proposition and solid fundamental strength provide an interesting argument to think about using COLM for a useful long-term buying opportunity.