Stocks in the Technology sector get a lot of attention and buzz from investors, analysts and talking heads alike no matter the time of year or current status of the economy.

I think that a big reason comes from the reality that progress and evolution in just about every other sector of the economy is, in one form or another, driven by the influence of technology on improving processes, products, and services from one end of the supply chain to the other.

That is also a reason that I think not only the Tech sector, but the Semiconductor industry in particular should always be included as part of an overall view of economic and market health. After all, semiconductors are the backbone of just about any technological tool we use – whether you’re talking about your smartphone, personal computer, and so much more. A lot of the basic functions of any modern car, for example is heavily reliant on software and the microchips and processors that they run on. As the world becomes ever-more connected through wireless Internet communications (think 5G and the Internet of Things, for example), that reliance is a constant force that keeps the Tech sector and Semiconductor companies at the forefront of the current and long-term economic picture.

The caveat, of course is that just because the rest of the market is paying attention to a sector or industry, it doesn’t mean that every stock in that grouping is a good investment. One of the big challenges the Semiconductor industry specifically has had to deal with are disruptions to semiconductor supply that go all the way back to the trade war between the U.S. and China in 2018 and 2019. A lot of U.S. semiconductor companies have historically been heavily dependent on Chinese tech companies to help provide production and fabrication services, particularly in the Tech sector. Trade tensions were heavily focused on Tech demand on Chinese goods and services, increasing costs and restricting chip supply.

Fueled in part by the trade war, as well as a general industry shift to be more locally, self-reliant, a lot of those companies have been working to bring more of those operations to U.S. shores, but the pandemic, not surprisingly, put an additional crimp on supply for everything from basic materials to labor, which makes the job a lot harder for many of the Semiconductor companies that service and supply the rest of the sector, as well as other sectors and industries. Adding even more global economic uncertainty from the ongoing conflict in Ukraine and its impact on energy prices only makes the overall picture look cloudier right now, which is why a lot of stocks in the Tech sector have seen significant drawdowns in price through most of 2022.

Microchip Technology (MCHP) is a good example of a Semiconductor company that fits this description. This is a company that has a long history in, and therefore exposure to China, but that also boasts a global customer base that spreads across multiple sectors of the economy. This is a stock that fell to extreme lows in early 2020 due to the pandemic and the pressures that came with it, but nearly quadrupled by the end of last year. Since then, concerns about inflationary pressure on the entire Tech industry pushed the stock about -24% off of its last high and in its own, clear bear market territory, where it has been hovering since late April. Does that mean the stock could also represent a good value, or is it just a big risk to take right now? Let’s find out.

Fundamental and Value Profile

Microchip Technology Incorporated is engaged in developing, manufacturing and selling specialized semiconductor products used by its customers for a range of embedded control applications. The Company operates through two segments: semiconductor products and technology licensing. In the semiconductor products segment, the Company designs, develops, manufactures and markets microcontrollers, development tools and analog, interface, mixed signal and timing products. Its functional activities include sales, marketing, manufacturing, information technology, human resources, legal and finance. Its product portfolio comprises general purpose and specialized 8-bit, 16-bit, and 32-bit microcontrollers, a spectrum of linear, mixed-signal, power management, thermal management, radio frequency (RF), timing, safety, security, wired connectivity and wireless connectivity devices, as well as serial electrically erasable programmable read-only memories (EEPROMs) and serial flash memories. MCHP has a current market cap of about $38.2 billion.

Earnings and Sales Growth: Over the last twelve months, earnings have grown more than 52.7%, while revenues increased by 25.7%. In the last quarter, earnings increased by 13.5%, while revenues were 4.93% higher. The company’s margin profile over the last twelve months showed Net Income was 18.85% of Revenues over the last twelve months, and strengthened to 23.74% in the last quarter.

Free Cash Flow: MCHP’s free cash flow is modest, but has been improving over the last year. Over the last twelve months free cash flow was almost $2.5 billion, and increased from about $1.9 billion a year ago. The current number translates to a Free Cash Flow Yield of 6.49%.

Dividend: MCHP’s annual divided is $1.10 per share and translates to a yield of about 1.6% at the stock’s current price. It should also be noted that management increased the dividend from $.93 at the beginning of this year, and again to its current level after the company’s latest earnings report.

Price/Book Ratio: there are a lot of ways to measure how much a stock should be worth; but I like to work with a combination of Price/Book and Price/Cash Flow analysis. Together, these measurements provide a long-term, fair value target around $66 per share. That means that even with the stock’s current drop, MCHP remains somewhat overvalued, with -4% downside from its current price, and with a practical discount price at around $53 per share. It is also worth mentioning that at the beginning of this year, this same analysis yielded a long-term, fair value target at around $62 per share.

Technical Profile

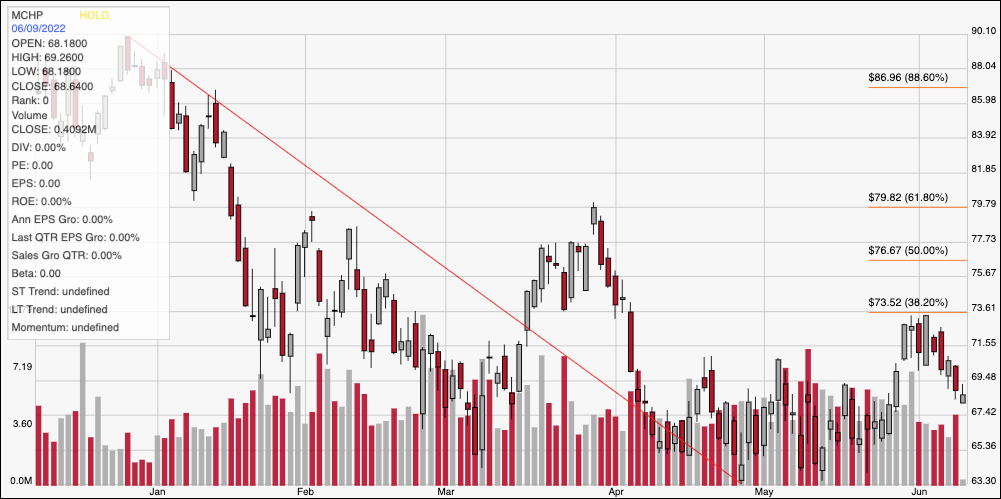

Here’s a look at the stock’s latest technical chart.

Current Price Action/Trends and Pivots: The chart above displays the stock’s price activity over the last six months. The red line traces the stock’s downward trend from a December peak at around $90 to its April low at around $63.50. It also provides the baseline for the Fibonacci retracement lines on the right side of the chart. Pulling a TradersPro chart for a longer period is a bit misleading, owing to a 2-for-1 stock split in October of 2021 that automatically cut the stock price in half. Since finding a trend bottom in April, the stock has been consolidating around that level, with current support sitting at around $67.50 and immediate resistance at the stock’s last pivot high at around $73.50. A push above $73.50 should find next resistance at around $78, while a drop below $67.50 should find next support at around $63.50, near the stock’s 52-week low point.

Near-term Keys: Given the stock’s current bearish momentum, a bullish short-term trade would be considered very aggressive; however, a bounce off of current support at $67.50 could be a good, albeit aggressive signal to think about buying the stock or working with call options, with $73.50 offering a reasonable near-term profit target. A drop below $67.50 could be a good reason to consider shorting the stock or buying put options, with $63.50 providing an attractive bearish profit target. Despite some useful fundamental strengths, MCHP doesn’t offer a useful value right now. Additional improvement in the company’s fundamental strength, or a continuation of the stock’s downward trend in the quarters ahead could shift that perspective, which also means that I think this is a stock that is worth coming back to on a periodic basis.