Looking for value in the stock market is something that tends to get dismissed by most pundits simply be cause it isn’t very sexy – at least, when the market is going up. When the market turns bearish, however, I get amused by how a lot of those pundits start talking about beaten-down stocks are now “terrific values.”

The caveat to effective value investing, of course is that a stock may experience a significant drop in price for a variety of reasons – but that doesn’t automatically mean that it is a good value. Oversimplifying the value question to what the stock’s price has been doing is a dangerous mistake to make. I’ve learned over all of my years in the market that there is some truth to the idea that whatever the stock’s current may be, or whatever its current direction is, the market is always right.

When a stock is experiencing a significant decline, or a downward trend that covers several months at a time, it is often because there are critical problems – in the economy, the industry, or even in the company itself – that have to be addressed to justify the stock’s current price. That’s why I’ve learned over time to not take any trend – bullish or bearish – at face value, but to dive in to the details. The opportunity for a smart value investor comes when you can find a positive divergence between a stock’s price action and its underlying fundamental and valuation metrics. That implies that the stock should be worth more than its current price, trend, or latest swing may be right now.

If you’ve been following me in this space at all, or participating in my weekly options trading webinar, you already know that CVS Health (CVS) is a good, old friend that I’ve followed for quite some time. The stock was a star performer in 2021 and the early part of this year, rising from about $68 at the beginning of March 2021 to a peak in early February at around $111. From that high, the stock has followed broad market momentum lower and into a clear downward trend – but the last month looks like the stock may be building a new set of bullish momentum, with some potential for a reversal of that downward trend.

I think one of the takeaways investors should think about in CVS’ market space is the role that CVS and other pharmacy companies play in any economic environment. For the largest players in the U.S. like CVS and Walgreen’s Boots Alliance (WBA), it isn’t just about their ability to fill prescriptions – although that is a core business that is resistant to economic downturns. These are also companies that are actively finding ways to evolve and innovate to stay competitive by expanding the scope of their retail locations to do more than just dispense prescriptions and sell consumer goods. They’re also remodeling those locations to provide expanded health care services and solutions. CVS, in particular was already gaining traction in leveraging its acquisition of insurer Aetna in 2018 to spur its broad transformation from just a drugstore/specialty retailer to a health care company providing a variety of services locally and affordably, and as a result it is hard not to take CVS seriously. I believe the company is uniquely positioned for the current environment, not only in the pharmacy space but also with what I think is a big competitive advantage over the rest of its industry from its Aetna merger.

The stock’s current price activity points to the intriguing possibility of a reversal of its intermediate-term downward trend. From its February high, the stock has also held up better than the rest of the broad market, falling only about -13% to its current price while other stocks (including WBA) have fallen into their bear markets. Does that also mean that the stock could offer a good value at its current price? Let’s dig in to find out.

Fundamental and Value Profile

CVS Health Corporation, together with its subsidiaries, is a health services company. The Company operates through four segments: Pharmacy Services, Retail/LTC, Health Care Benefits and Corporate/Other. The Pharmacy Services segment provides a range of pharmacy benefit management (PBM) solutions, including plan design offerings and administration, retail pharmacy network management services, mail order pharmacy, specialty pharmacy, clinical services, disease management services and medical spend management. The Retail/LTC segment sells prescription drugs and a range of health and wellness products and general merchandise. Its Health Care Benefits segment offers a range of traditional, voluntary and consumer-directed health insurance products and related services. It has approximately 9,900 retail locations, over 1,100 walk-in medical clinics, a pharmacy benefits manager with approximately 105 million plan members, specialty pharmacy services and a senior pharmacy care business. CVS has a market cap of $125 billion.

Earnings and Sales Growth: Over the last twelve months, earnings increased by 8.82%, while Revenues rose by 11.19%. In the last quarter, earnings grew by 12.12% while sales were flat, but positive, by 0.29%. The company’s margin profile is historically very narrow; over the last twelve months Net Income was 2.67% of Revenues, and increased to 3.01% in the last quarter.

Free Cash Flow: CVS’s free cash flow is very healthy, at nearly $16.2 billion. That marks an improvement from $11.6 billion a year ago, and $15.7 billion in the quarter prior. The current number translates to an attractive Free Cash Flow Yield of about 13.3%.

Debt to Equity: CVS has a debt/equity ratio of .70. That is a generally conservative number that has dropped steadily from 1 at the beginning of 2021. In the last quarter, cash and liquid assets were about $15.7 billion versus $52 billion in long-term debt. The vast majority of that debt comes from the acquisition of health insurer Aetna, however the fact that long-term debt has dropped from about $65 billion since the beginning of 2020 is a good reflection of the company’s success so far (with plenty of work still to go) in transitioning these disparate organizations into a larger, productive company.

Dividend: CVS pays an annual dividend of $2.20 per share, and which translates to an annual yield that of about 2.34% at the stock’s current price. It is also noteworthy that, while dividend increases had been suspended (not because of COVID, but to give the company flexibility to reduce debt gradually from the Aetna merger) beginning in 2020, management maintained the dividend throughout the pandemic and announced the first increase, along with the implementation of a new stock buyback program at the beginning of this year.

Value Proposition: there are a lot of ways to measure how much a stock should be worth; but I like to work with a combination of Price/Book and Price/Cash Flow analysis. Together, these measurements provide a long-term, fair value target at about $93.50 per share. That suggests the stock is fairly valued at its current price, with a practical discount at about $75.

Technical Profile

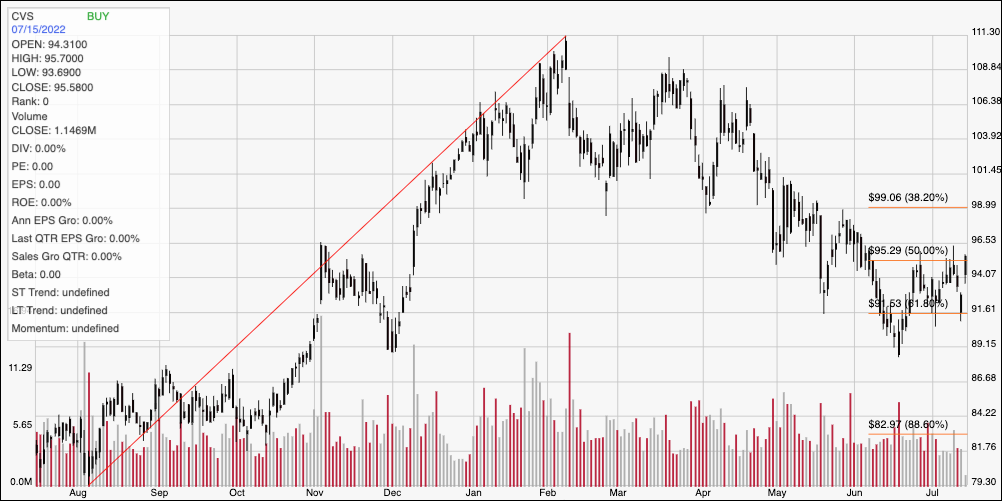

Here’s a look at CVS’ latest technical chart.

Current Price Action/Trends and Pivots: The diagonal red line marks the stock’s upward trend from an August 2021 low at around $79 to its peak in February at around $111. It also provides the baseline for the Fibonacci retracement lines shown on the right side of the chart. After finding its latest low at around $89 in June, the stock has been building gradual bullish momentum, and appears to be breaking its latest resistance level at around $95 with today’s price activity. That marks current support at $95 (previous resistance becomes new support) with new, immediate resistance expected at $99, about inline with the 38.2% retracement line. A drop below $95 should find next support at around $91.50 where the 61.8% retracement line sits.

Near-term Keys: If you prefer to work with short-term trading strategies, the current break above resistance at $95 could offer an attractive signal to buy the stock or work with call options with an eye on $99 as a useful exit point. A bearish signal would come from a drop below $95, with $91 providing a useful target no matter whether you choose to short the stock or buy put options. From the standpoint of value and long-term opportunity, the stock’s recent drop, while steep has only brought the stock to its fair value pricee, so it can’t be called a useful value-driven opportunity yet. For practical purposes, the stock would need to fall to around $75 before I think a compelling, value-based argument can be made.