(Bloomberg) — One big force at the center of the two-month equity rally is showing signs of fatigue.

It’s the behavior of short sellers, whose frantic efforts to unwind bearish wagers created buying that added fuel to the $7 trillion share advance. Evidence is arising now that the process is petering out.

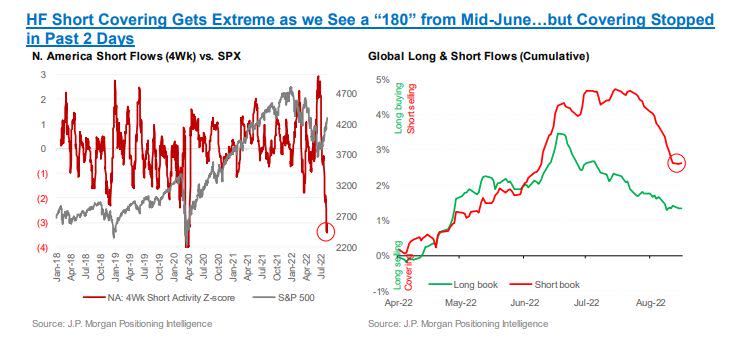

Hedge funds that make both bullish and bearish equity bets pretty much stopped purchasing shares to return to lenders this week after previously doing it at the fastest pace in more than two years, data from JPMorgan Chase & Co.’s prime broker unit show.

Meanwhile, Goldman Sachs Group Inc.’s hedge-fund clients boosted short positions Wednesday, with bets against exchange-traded funds rising the most in more than two months.

The shift makes sense from certain technical perspectives. The S&P 500 this week failed to surpass a key long-term trendline, its 200-day average. A bunch of potentially bearish events are coming up, from central bankers’ annual retreat in Jackson Hole, Wyoming, to the release of government data on consumer prices and employment.

“Hedge funds may view the June-to-August rally as too far, too fast, and now are licking their chops for another round of downside,” said Mike Bailey, director of research at wealth management firm FBB Capital Partners. “Tactically, markets look a bit feeble at the moment, as investors price in good inflation and Fed news.”

Since the market’s trough in June, computer-driven traders such as trend followers that are mostly active in the futures market have snapped up about $100 billion of equities, Morgan Stanley’s trading unit estimated, as many went short during the first-half rout and were caught off guard by the subsequent rebound.

There are still a lot of bearish positions outstanding, Morgan Stanley’s data show. In the cash market, while $50 billion has been covered since June, the net amount of added shorts remains elevated, sitting at $165 billion this year. Short interest among single stocks stands in the 84th percentile of a one-year range.

“The short base in US equities is still not cleaned up though,” Morgan Stanley wrote in a note. “With short leverage still high, there is more potential for hedge fund short covering.”

For now, however, hedge funds are taking a breather. After spending the past month unwinding bearish trades at a pace last seen at the start of the pandemic bull market, JPMorgan’s hedge-fund clients stopped covering this week.

At Goldman, hedge funds increased short sales while added longs on Wednesday, leading to the biggest jump in gross trading activity since the market’s low in mid-June. Though with shorts sales outpacing long buys by a ratio of 3-to-1, net selling hit a three-week high.

Shorts unwinding amplified the market upside during the summer lull, but all the caution suggests that the downside risk is likely limited, and it potentially sets the stage for further gains should things start to improve, according to Benjamin Dunn, president of Alpha Theory Advisors.

“Nobody trusts the rally,” Dunn said. “We could be in for a period of weakness, but by the same token, a lot of people who want to sell have already sold,” he added. “That’s been the problem the last several months in this market. It’s nothing but positioning, almost nothing fundamental.”

©2022 Bloomberg L.P.