Contrarian investors and bargain hunters tend to think quite a bit differently about stock price movements and trends than growth-focused investors. When everybody is buying, we tend to get more cautious, and when everybody is running for the exits, we start finding more and more attractive opportunities at great prices.

2022 has been a rough year for just about every investing strategy, no matter whether you focus on growth or value. The truth is that just because a stock may have already dropped significantly off of a previous high, it really says nothing about whether it will continue to fall or when it will reverse. That’s also one of the reasons that contrarians and value investors like myself spend a lot of time thinking about how much a stock should be worth. We have to measure whether the long-term opportunity is great enough to justify the real possibility of buying and holding a stock through a continued, potentially long-term downward trend.

One area that has remained resilient, but certainly not immune to broader pressures throughout the past two and a half years is the Food Products industry. For most of 2021, stocks in this industry not only kept pace with the market, but in many cases outperformed the sexier, growth-driven industries and names. Diving into the fundamentals of many of these companies have shown balance sheets that continue to weather the storm, first from the pandemic and now from increasing inflationary indicators better than most other industries. That increasing fundamental strength was a big driver in stock price performance in 2020 and 2021, but some of the luster has come off of those stocks this year.

In the Food Products industry, those inflationary indicators have begun rippling into consumer prices. With interest rates expected to continue to rising in 2022 and possibly into 2023 to attempt to curb inflation, this looks like a headwind that is unlikely to be resolved any time soon. These are pronounced in many cases by persistent labor shortages that continue to limit capacity and productivity in ways that have begun to limit product availability for consumers. That means that while the Food Products industry is likely to continue to see healthy demand, how much it is able to rise to meet demand remains an open question.

Tyson Foods Inc. (TSN), is a stock I’ve followed for some time. 2020 wasn’t good for the stock; from a peak at around $94 to start that year, the stock began a downward slide that only accelerated as the global coronavirus pandemic took the stock market into bear market territory. TSN did find a bottom at around $44 with the rest of the market, and by the end of 2020, the stock was sitting at around $62.50. 2021 saw the stock extend its long-term upward trend even more, hitting a 52-week high in February of this year at around $100. From that point, however, the stock has followed the rest of the market lower once again and into its own bear market territory, having extended its downward trend to its current price at around $75 per share.

In 2022, the company has experienced a useful tailwind in the form of global increases in protein demand, helped in part of pork shortages in Asia that are expected to persist following the African Swine Flu epidemic that has ravaged that country’s hog population. Even so, inflationary pressures, including rising input costs are something the company is dealing with, like just about every other company in the Food Products industry. Those pressures, however do appear to be manageable, which begs the question: has the stock’s drop in price (-25% from its February as of this writing) put it in a useful position for a value seeker? Let’s find out.

Fundamental and Value Profile

Tyson Foods, Inc. is a food company, which is engaged in offering chicken, beef and pork, as well as prepared foods. The Company offers food products under Tyson, Jimmy Dean, Hillshire Farm, Sara Lee, Ball Park, Wright, Aidells and State Fair brands. The Company operates through four segments: Chicken, Beef, Pork and Prepared Foods. It operates a vertically integrated chicken production process, which consists of breeding stock, contract growers, feed production, processing, further-processing, marketing and transportation of chicken and related allied products, including animal and pet food ingredients. Through its subsidiary, Cobb-Vantress, Inc. (Cobb), the Company is engaged in supplying poultry breeding stock across the world. It produces a range of fresh, frozen and refrigerated food products. Its products are marketed and sold by its sales staff to grocery retailers, grocery wholesalers, meat distributors, warehouse club stores and military commissaries, among others. TSN has a current market cap of $27.2 billion.

Earnings and Sales Growth: Over the last twelve months, earnings declined -28.15%, while sales increased 8.15%. In the last quarter, earnings were a little more than -15.25% lower while sales rose by 2.88%. TSN traditionally operates with a modest margin profile; in the last twelve months, Net Income was 7.75% of Revenues, but decreased to 5.56% in the last quarter.

Free Cash Flow: TSN’s Free Cash Flow is generally healthy, at a little more than $1.4 billion. That number has dropped from about $2.6 billion a year ago, and $2.2 billion in the quarter prior. Its current level translates to a Free Cash Flow yield of 5.21%.

Debt to Equity: TSN has a debt/equity ratio of .42, which is conservative. Cash and liquid assets were about $437 million at the end of 2019, increased to $2.4 billion at the end of 2020, and fell to a little under $1.05 billion in the last quarter. TSN carries about $8.26 billion in long-term debt. The company’s operating profile indicates there should be no problem servicing debt, however the latest declines in cash and free cash flow, along with deteriorating Net Income are concerns.

Dividend: TSN increased its annual dividend from $1.68 per share to $1.78 per share in 2020, and again to $1.84 per share late last year. The current number translates to a dividend yield of 2.46% at the stock’s current price. TSN’s dividend has also increased from $1.20 per share in late 2018, and $1.52 at the end of 2019. The fact that management not only maintained the higher dividend, but increased it during the pandemic despite the early challenges it had to deal with in adjusting to broad operating conditions is noteworthy since so many other companies were forced to reduce or suspend their dividends during the same period.

Price/Book Ratio: there are a lot of ways to measure how much a stock should be worth; but I like to work with a combination of Price/Book and Price/Cash Flow analysis. Together, these measurements provide a long-term, fair value target around $89 per share. That suggests that the stock offers a tempting bargain proposition, with 34% upside from its current price. It’s also worth noting that one quarter ago, this same analysis yielded a long-term target at around $89 per share

Technical Profile

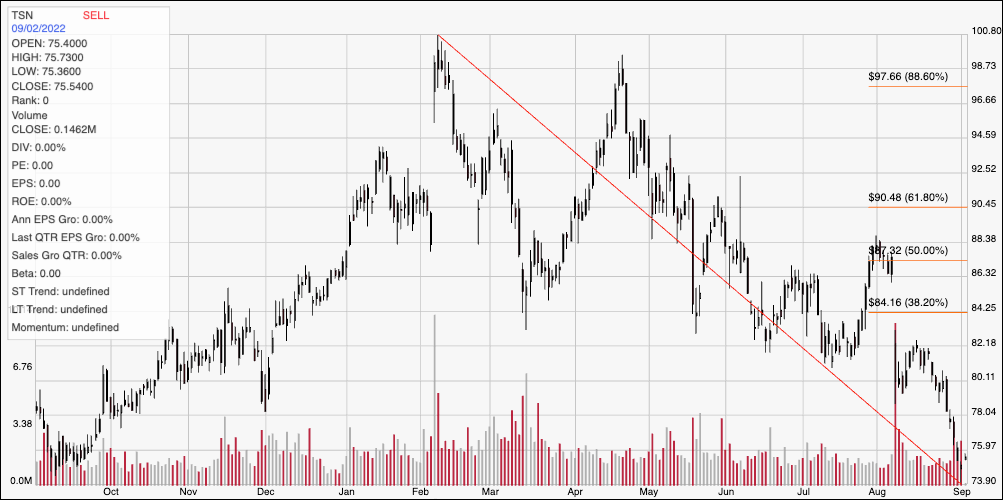

Here’s a look at the stock’s latest technical chart.

Current Price Action/Trends and Pivots: The diagonal red line outlines the stock’s downward trend from its February peak at around $101to its latest low, reached this week at around $74. It also provides the baseline for the Fibonacci retracement lines shown on the right side of the chart. The stock appears to be using $74 as a pivot point, placing current resistance at that level, with immediate resistance at around $78 based in pivot activity seen at the end of 2021. A push above $78 should have upside to about $81 per share to next resistance. The stock would need to push above the 38.2% retracement line at around $84 to mark a useful reversal signal of the current downward trend. A drop below $74 should find next support at around $70, using the current distance between support and resistance as a benchmark.

Near-term Keys: TSN’s current downward trend has pushed the stock into interesting bear market territory, making the stock’s value proposition pretty tempting at this level. I do think that the latest declines in Net Income, Cash, and Free Cash Flow are significant enough to suggest that the smarter approach right now is to wait for these numbers to see signs of improvement before thinking about TSN as a useful long-term bargain. If you prefer to work with short-term term trading strategies, you could use a push above $78 as a signal to buy the stock or work with call options, with a useful, initial profit target at around $81 and $84 if bullish momentum accelerates. A drop below $74 could offer a signal to consider shorting the stock or buying put options, using $70 as a practical profit target on a bearish trade.