It seems that every year, economic and market activity finds a way to revolve around one or two primary themes. It’s safe to say that no matter where you start, the primary economic theme for 2022 boils down to inflation.

Economic metrics were clearly starting show that inflation was picking up steam in late 2021, and this year has only confirmed that fact even more, with indicators consistently showing levels from one month to the next that haven’t been seen in four decades. The first, and most obvious impact inflation has on the economy is on interest rates. As the primary tool central banks in market-driven economies have to influence economic growth, rising interest rates are the first lever that usually gets pulled when the Fed decides it needs to slow down the pace of inflation. This year has seen multiple increases in rates, with the size of each increase growing in response to economic data, and most experts expecting another increase this week at the end of the Fed’s September policy meeting.

With consumer prices already high, and the impact of rising interest rates now a functional reality, the normal expectation is that consumer demand for discretionary goods and services should decline. Since the market tends to act in a forward-looking fashion – meaning that it prices in both fear and enthusiasm about what investors think is going to happen, before it actually does – the net result is economic uncertainty that has extended throughout the year, and has kept all of the major market indices at bear market levels. It also has a lot of talking heads speculating not about whether a recession is imminent – that seems to be a foregone conclusion for most of them – but rather how soon it will rear its ugly head.

Economic uncertainty may blunt some of the enthusiasm for industries tied to stocks in industries that are considered “discretionary,” or sensitive to the ebb and flow of economic growth. For contrarians like me, the irony of that gloomy forecast is twofold. First, it comes in contrast to economic data showing healthy consumer spending, even as prices have generally increased, along with continued, healthy employment numbers. Second, the market’s current bear market levels also open up the potential to find stocks in those pockets of the market that could mark the best bargains, since declining stock prices may not directly correlate with a company’s fundamental strength. That’s why, even as others may look to avoid economically sensitive sectors and industries, smart bargain hunters start looking for new “targets of opportunity”.

That brings me to today’s highlight. Levi Strauss & Co. (LEVI) is a name most of us in North America – and even a big part of the world – are familiar with, and a brand that I think speaks as much to Americana as country music and apple pie. This is a stock that has been following a strong downward trend for the past year, falling from a 52-week high at around $29 to its low in July at around $15.50. After staging a failed rally in August that peaked at about $20, the stock is sliding back again to hover a little below $18 as of this writing. With a fundamental profile that points to healthy liquidity, manageable debt, and still-solid profitability even as input costs increase, this is a stock that may also be offering a useful, value-oriented opportunity for a patient investor Let’s dive in.

Fundamental and Value Profile

Levi Strauss & Co. is an apparel company. The Company designs, markets and sells directly or through third parties and licensees products that include jeans, casual and dress pants, tops, shorts, skirts, jackets, footwear and related accessories for men, women and children under the Levi’s, Dockers, Signature by Levi Strauss & Co. and Denizen brands. The Company operates through three segments: the Americas, Europe, and Asia. Its Asia segment includes the Middle East and Africa. The Company’s products are sold in approximately 50,000 retail locations in more than 110 countries, including approximately 3,000 brand-dedicated stores and shop-in-shops. It has approximately 1,039 Company-operated stores located in 36 countries and approximately 500 Company-operated shop-in-shops. The remainder of its brand-dedicated stores and shop-in-shops are operated by franchisees and other partners. LEVI’s market cap is around $7 billion.

Earnings and Sales Growth: Over the last twelve months, earnings increased by 26%, while revenues grew 15.3%. In the last quarter, earnings declined by about -37% while sales declined by -7.57%. LEVI’s operating profile is showing signs of weakness; over the last twelve months, Net Income was 11.28% of Revenues and declined to 3.38% in the last quarter.

Free Cash Flow: LEVI’s free cash flow is healthy, at $41.5.2 million over the last twelve months. That marks a decline from $578.25 million a year ago, and from $550.4 million in the last quarter. The current number translates to a Free Cash Flow Yield of 5.89%.

Debt to Equity: LEVI’s debt/equity ratio 0.58. This is a low number that speaks to management’s conservative approach to leverage. As of the last quarter, the company reported about $698.3 million in cash and liquid assets against about $1 billion in long-term debt. While the company’s operating profile indicates that debt service isn’t a concern, the fact is that liquidity has decreased, from $901.82 million three quarters ago and $777 million in the quarter prior.

Dividend: LEVI’s annual divided is $.48 per share, which translates to a yield of 2.7% at the stock’s current price. Management increased the dividend after the most recent earnings announcement, from $.40 per share, per annum. An increasing dividend is a strong sign of management’s confidence in their long-term road ahead.

Price/Book Ratio: there are a lot of ways to measure how much a stock should be worth; but I like to worth with a combination of Price/Book and Price/Cash Flow analysis. Together, these measurements provide a long-term target at about $22.50 per share. That suggests that the stock is nicely undervalued, with about 26% upside from its current price.

Technical Profile

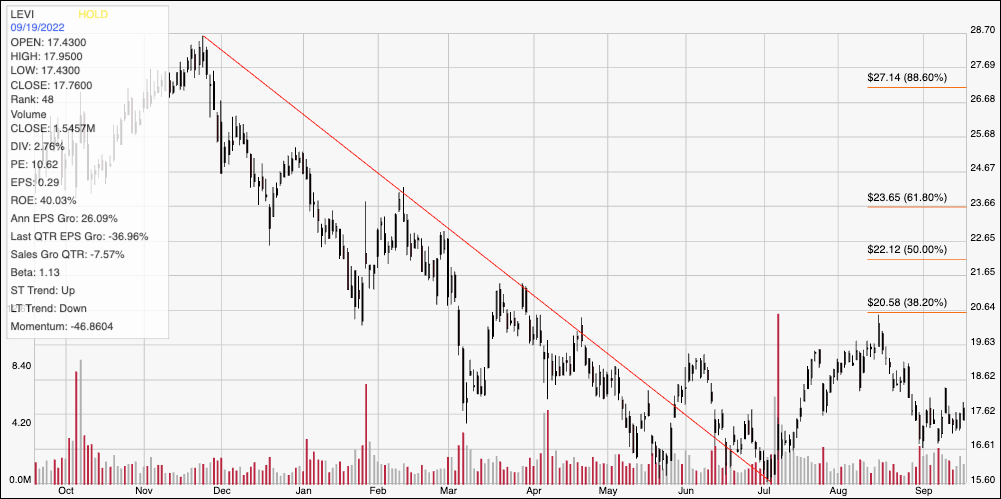

Here’s a look at the stock’s latest technical chart.

Current Price Action/Trends and Pivots: The red diagonal line traces the stock’s downward trend from a peak at around $29 in November of last year to its recent low at the start of July at around $15.50. It also provides the baseline for the Fibonacci retracement lines shown on the right side of the chart. After rallying to about $20 in mid-August where the 38.2% offered strong resistance, the stock has fallen back to find current support at around $17, with immediate resistance a little above $18. A push to $18.50 could have short-term upside to the top of the last rally at around $20.50. A drop below $17 could see the stock retest its 52-week low at around $15.50.

Near-term Keys: I think LEVI’s fundamental profile offers an interesting value proposition at its current price. Declining liquidity and Net Income is a concern, and could be a reflection of both long-term debt reduction as well as rising material and other input costs. The quarters ahead will provide a better indication as to whether these are cyclical concerns or longer-term in nature. The stock’s current activity could offer some interesting signals to work with short-term trades. A drop below $17 could offer a useful signal to consider shorting the stock or buying put options, with a practical, nimble bearish profit target at around $15.50 per share. A push to $18.50 could offer a an interesting signal to think about buying the stock or working with call options, with a practical bullish target at around $20.50. In a practical sense, the stock would need to push above $20.50 with momentum to offer the first legitimate signal of a bullish trend reversal.