(Bloomberg) — Unwavering profit projections. Benign chart patterns. Big hedges in the options market.

All the things that bulls expected to put a brake on the worst equity selloff in 30 months have just summarily failed.

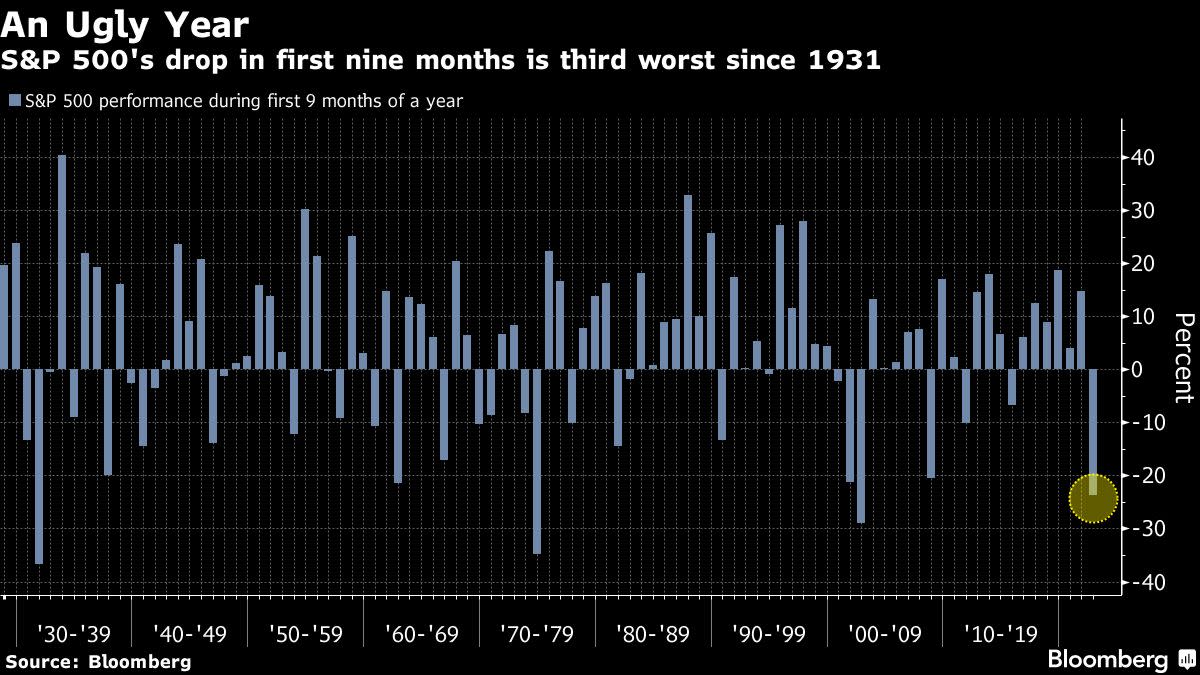

The Federal Reserve, with an assist from UK policy makers, overpowered them all to deliver a week that rocked financial markets around the world and sparked warnings of potential systemic strife. Down for a sixth time in seven weeks, the S&P 500 sank to fresh bear-market lows. Notching a 25% decline in nine months, the benchmark index has now suffered its third-worst performance at this point of a year since 1931.

Bulls still point to signals that the bottom could be nigh, yet the pattern of past market cycles suggests the pain for American equities can easily persist.

Take a simple accounting of prior bear markets, where the average selloff hit 39% over 20 months. That would imply another 19% drop from here. Or look at how past tightenings have coincided with stock moves. While not all Fed hiking cycles spelled doom for equities, those that did typically failed to find a floor until the central bank reversed its course — a prospect no one on Wall Street can take seriously anytime soon until price pressures subside.

“Inflation is a major constraint because any attempt to rescue markets or international financial stability issues are likely to be inflationary,” said Steve Chiavarone, senior portfolio manager at Federated Hermes. “The market is forced to reckon with the possibility that the central-bank put is not in place.”

The S&P 500 sank 2.9% in five days to end the month with a host of terrible superlatives. Stocks fell for a third straight quarter, posting the worst September in two decades. The index is down 12% in the past three weeks alone.

Extreme pessimism, oversold markets, and rock-bottom fund positioning — from a technical perspective, the ingredients for a rebound are in place. Yet with the Fed hellbent on fighting inflation, a goal that it aims to achieve by tightening financial conditions to slow demand, whatever worked in the past as a buffer stops working.

Along the way, the summer rally faltered even after the S&P 500 recouped half its bear-market decline incurred between January and June, defying a 50% indicator that’s touted as a tool with a perfect record of calling the start of a new bull. The June low gave way, as did a series of round numbers and key trendlines such as the 100-day average.

Amid the relentless selling, bulls are yielding one after another. Retail traders, one of the most steadfast dip buyers since the 2020 pandemic crash, are bailing on stocks.

JPMorgan Chase & Co. strategist Marko Kolanovic is the latest to succumb to the gloom, citing the risk of policy errors at central banks and an escalation of war following the destruction of the Nord Stream pipelines in Europe.

“The most recent increase of geopolitical and monetary policy risks puts our 2022 price targets at risk,” Kolanovic wrote in a note Friday. “While we remain above-consensus positive, these targets may not be realized until 2023 or when the above risks ease.”

The firm’s year-end target for the S&P 500 is 4,800, a 34% gain from Friday’s close.

Forecasts for sturdy profit growth in the past offered cushion during times of stress. Not this time. While analyst estimates continued to point to an increase in S&P 500 earnings next year, skeptics say the numbers can’t be trusted when companies from Apple Inc. to CarMax Inc. warned about slowing consumer demand.

Bulls taking cover with protective options also got a comeuppance. The Cboe S&P 500 5% Put Protection Index, tracking a strategy that holds a long position on the index while buying monthly 5% out-of-the-money puts as a hedge, is nursing a 21% loss this year that is almost identical to that of the index, when dividends are taken into account.

“Investors are getting skittish here as we hit some pretty critical support levels,” said Matt Miskin, co-chief investment strategist at John Hancock Investment Management. “What investors are now saying is ‘we’ve got to see this picture change before looking to put capital back to work.’”

While every cycle is different, traders seeking bottom patterns find ominous signals in history. Down 25% over nine months, this bear run is less than half the average duration of the previous 14 down cycles, data compiled by S&P Dow Jones Indices and Bloomberg show.

During the previous six bear markets, all bottoms formed when the Fed was lowering rates. That’s a long way off considering bond traders currently don’t expect Fed rates to peak until April 2023.

The everything-rally that investors were once accustomed to during 13 years of near-zero interest rates is over. Bond losses have snowballed, with Treasury yields spiking to multiyear highs. Right now, cash is the darling asset.

“You’re trying to assess how comfortable you feel about the path that’s laid out on the monetary policy front. If you’re getting comfortable with that, you can certainly talk about some of the bottom fishing,” Marvin Loh, a senior macro strategist at State Street Global Markets, said in an interview on Bloomberg TV. “We, on the other hand, think there is a great deal of uncertainty so you stay defensive.”

©2022 Bloomberg L.P.