Growth investing leans heavily on the principle that “a stock tends to follow the direction of its previous trend,” which may just be a nerdy way to say that the longer a stock has been going up, the more likely it is to keep going up. It is also why growth investors shun stocks that are at or near historical lows resulting from downward trends.

Value investing, on the other hand holds that all trends are finite; every upward trend is doomed to fail at some point, and every downward trend is destined to recover. The idea makes logical sense, but it’s actually is a contrarian, counter-intuitive idea for many to apply in making investment decisions because it means that value investors aren’t afraid to buy a stock when the rest of the market has sold it and is staying away. Sometimes, it means buying a stock at what the bargain hunter has decided is a useful, “good enough” price, and then watching the stock drop even more. That is also a hard thing for a lot of investors to endure, and it is why being a successful value investor requires discipline as well as patience. It also means that stocks that have been going up, and that are attractive to growth investors usually draw no more than a shrug from value seekers.

Over the last three and a half years, I’ve used economic uncertainty – first from a year-long trade war through 2019, and then of course the COVID-19 pandemic starting in 2020, and certainly all of this year’s focus on inflation, interest rates, and war in Ukraine – as the basis for a defensive approach to a lot of the analysis I’ve done. I think that when economic conditions become more difficult, positioning defensively by focusing on industries that are traditionally less sensitive to the cyclicality of economic health makes sense. It’s a strategy that has helped me make a number of conservative, useful investments since 2018. I also believe that, with global inflation still high, and interest rates expected to remain high, the need to remain conservative and defensive will continue to be a smart approach for the rest of the year. I also think it means that stocks in the Food Products industry will also be a useful way to keep your money working for you.

The caveat to looking for investments in Food Products stocks is that not all stocks are created equal. Not only do not all companies share the same kind of fundamental strength, it’s also true that not all Food Products stocks might offer a good value. That’s an important distinction to make, because just as a stock in a new, long-term upward trend typically outpaces the underlying company’s fundamental strength, stocks in downward trends aren’t categorically driven by fundamental weakness.

Kroger Company (KR) is the largest traditional food retailer in the United States, and a company that I’ve kept an eye on for some time. This is a stock that followed a strong upward trend through 2021 to a peak in April of this year at almost $63 per share. The stock is down about -23% from that high, putting the stock with a lot of the rest of the market and in its own respective bear market. The last month, however has seen the stock rally about 15% from its latest low point, with enough bullish momentum in place to suggest the stock could be setting up to reverse that longer, bearish trend.

KR has been among the most proactive innovators in the entire Consumer Staples industry over the past few years, investing heavily in alternative revenues streams like Kroger Personal Finance and Kroger Precision Marketing, building localized, automated warehouse facilities throughout the U.S. and online shopping and curbside delivery that is now in place in 95% of its coverage area. Many of these initiatives have yielded positive results on the company’s earnings reports, and have enhanced the company’s ability to compete against larger rivals like Wal-Mart and Target Stores, but also represent significant capital investments that have only just begun and are expected to continue for at least the next couple of years. I think the stock’s fundamentals could give a bullish investor good reason to add KR to a diversified portfolio; but that begs the question, is it also a good value? Let’s dive in and take a look.

Fundamental and Value Profile

The Kroger Co. (KR) manufactures and processes food for sale in its supermarkets. The Company operates supermarkets, multi-department stores, jewelry stores and convenience stores throughout the United States. As of February 3, 2018, it had operated approximately 3,900 owned or leased supermarkets, convenience stores, fine jewelry stores, distribution warehouses and food production plants through divisions, subsidiaries or affiliates. These facilities are located throughout the United States. As of February 3, 2018, Kroger operated, either directly or through its subsidiaries, 2,782 supermarkets under a range of local banner names, of which 2,268 had pharmacies and 1,489 had fuel centers. As of February 3, 2018, the Company offered ClickList and Harris Teeter ExpressLane, personalized, order online, pick up at the store services at 1,056 of its supermarkets. P$$T, Check This Out and Heritage Farm are the three brands. Its other brands include Simple Truth and Simple Truth Organic. KR has a market cap of $34.4 billion.

Earnings and Sales Growth: Over the last twelve months, earnings increased by 12.5%, while sales improved by 9.33%. In the last quarter, earnings declined almost -38% while revenues also declined, by about -22.3%. Like most Food retailers, KR operates with razor-thin margins, as Net Income was about 1.69% of Revenues for the last twelve months, and strengthened slightly in the most recent quarter to 2.11%. The improvement in Net Income in the last quarter is an interesting counter to the negative earnings pattern.

Free Cash Flow: KR’s free cash flow is healthy, at $2.8 billion over the last twelve months. That marks a decline from $3.1 billion a year ago, but an improvement from about $2.65 billion in the quarter prior. The current number translates to a free cash flow yield of 8.28%.

Debt to Equity: KR has a debt/equity ratio of 1.3. This is higher than I usually prefer to see, but also isn’t unusual for Food Retailing stocks. The company’s balance sheet indicates that operating profits are more than adequate to repay their debt, and is a sign of strength, with about $2.2 billion in cash and liquid assets (versus $2.5 billion in the quarter prior), against $12.5 billion in long-term debt. Their long-term debt is a reflection of the capital-intensive investments in itself the company has made to streamline its operations, modernize and automate its own supply chain, and to stay competitive in its market. I take the decline in Free Cash Flow and cash over the past year as a reflection of cost increases that KR has actively chosen not to fully pass to their customers, and that some analysts are pointing at as a potential headwind to profitability into 2023.

Dividend: KR pays an annual dividend of $1.04, which marks an increase from $.64 per share in early 2020, $.72 per share at the beginning of 2021 and $.84 earlier this year. The current payout translates to a yield of about 2.16% at the stock’s current price. The increasing dividend over the last two years should be taken as a sign of management’s confidence in their operating model and ability to keep the business growing in the long term.

Price/Book Ratio: there are a lot of ways to measure how much a stock should be worth; but I like to work with a combination of Price/Book and Price/Cash Flow analysis. Together, these measurements provide a long-term, fair value target around $61 per share. That means that KR is nicely undervalued, with 25% upside from its current price.

Technical Profile

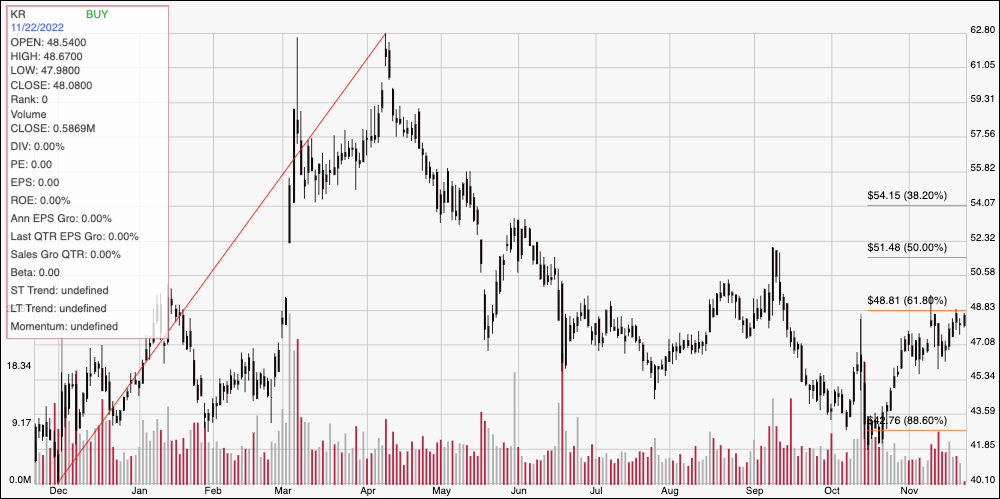

Here’s a look at the stock’s latest technical chart.

Current Price Action/Trends and Pivots: The chart above displays the last year of price movement for KR. The red diagonal line marks the stock’s upward trend from a low point at around $40 in October of last year to its April peak at around $63; it also provides the baseline for the Fibonacci retracement lines shown on the right side of the chart. From a trend low at around $42 in October, the stock has rallied to its current price at around $48, and is nearing immediate resistance at around $49 where the 38.2% retracement line sits. Current support is around $47, based on pivot activity at the end of October and early November. A push above $49 should have near-term upside to about $52, based on a pivot high seen in September, while a drop below $47 should have limited downside to about about $45 per share.

Near-term Keys: KR’s bounce off of its downward trend low, and rally in the last month is an interesting set up for bullish-focused investors. It’s also nice that even with the latest rally, the stock is offering an interesting value proposition that I think is worth taking seriously. If you prefer to focus on short-term trading opportunities, a push above $49 could provide a signal to think about buying the stock or working with call options, with a useful, near-term profit target at around $52 per share. If the stock drops below $47, you could also consider shorting the stock or buying put options, using $45 as a practical profit target on a bearish trade.