(Bloomberg) — No fuel is more essential to the global economy than diesel. It powers trucks, buses, ships and trains. It drives machinery for construction, manufacturing and farming. It’s burned for heating homes. And with the high price of natural gas, in some places it’s also being used to generate power.

Within the next few months, almost every region on the planet will face the danger of a diesel shortage at a time when supply crunches in nearly all the world’s energy markets have worsened inflation and stifled growth.

The toll could be enormous, feeding through into everything from the price of a Thanksgiving turkey to consumer bills for heating homes this winter. In the US alone, the surging diesel cost will mean a $100 billion hit to the economy, according to Mark Finley, an energy fellow at Rice University’s Baker Institute of Public Policy.

“Anything and everything that gets moved in our economy, diesel is there,” Finley said. “Moving stuff around is one thing. People potentially freezing to death is another.”

In the US, stockpiles of diesel and heating oil are at their lowest point ever for this time of year in data going back four decades. Northwest Europe is also facing a low buffer — inventories are forecast to hit a low this month and then tumble even more by March, shortly after sanctions come into play that will cut the region off from Russian seaborne supplies. Global export markets have gotten so tight that poorer countries like Pakistan are getting shut out, with suppliers failing to book enough cargoes to meet the nation’s domestic needs.

“It’s certainly the biggest diesel crisis that I have ever seen,” said Dario Scaffardi, the former chief executive officer of the Italian oil refiner Saras SpA who’s spent almost 40 years in the industry.

Diesel in the spot market of New York harbor, a key benchmark, is up roughly 50% this year. The price reached $4.90 a gallon in early November, about double year-ago levels.

Even more telling is the premium that diesel is commanding. Spreads for the fuel are widening both against crude oil, a sign of how tight refining capacity is, and in relation to supplies that are for later delivery, underscoring that traders are desperate to get their hands on the stuff now. In northwest Europe, diesel futures cost about $40 a barrel more than Brent, versus a five-year seasonal norm of just $12. New York diesel futures for December delivery are trading about 12 cents higher than those for January. That compares with a premium of less than a cent at this time last year.

What’s Causing the Shortage?

There are major constraints globally on refining capacity. Supplies of crude oil are already fairly tight. But the bottleneck is much more acute when it comes to turning that raw commodity into fuels like diesel and gasoline. That’s partly a function of the pandemic, after lockdowns destroyed demand and forced refiners to close some of their least profitable plants. But the looming transition away from fossil fuels has also dented investments in the sector. Since 2020, US refining capacity has shrunk by more than 1 million barrels per day. Meanwhile in Europe, shipping disruptions and worker strikes have also eaten into refinery production.

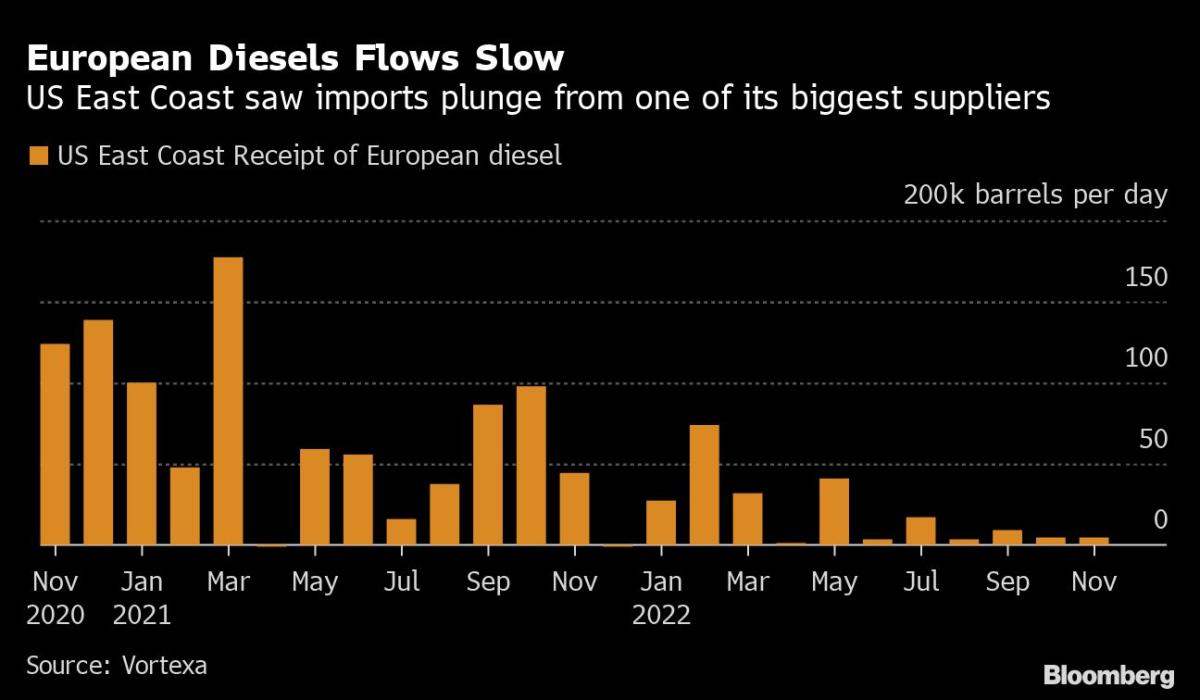

Things could get much more dramatic with the European Union’s looming pivot away from Russian supply. Europe relies more heavily on diesel than any other in the world. Roughly 500 million barrels a year get delivered by ship, with around half of that typically loaded at Russian ports, according to data from Vortexa Ltd. The US also has halted imports from Russia, which was a big supplier to the East Coast last winter.

Also churning in the background is a market structure known as backwardation, when premiums are higher for supplies with prompt deliveries than for longer-term ones. Not only has that spread been unusually large, but the backwardation has lasted unusually long. This backwardated market structure incentivizes suppliers to sell now instead of holding onto the product to build inventories.

Emergency Protocols

In the US, shortages along the East Coast already had suppliers rationing and initiating emergency protocols, and winter hasn’t even begun.

The Northeast, the most densely populated corner of the US where temperatures are often below freezing during a bitter winter, is also the most reliant on heating oil for keeping homes warm. (Diesel and heating oil are the same product in the US, just taxed differently.) Even in a best-case scenario, consumers there will be saddled with the highest energy bills in decades this winter. Already, the government has nearly doubled its estimate for the increase, projecting that families who rely on heating oil can expect to pay 45% more than last winter, up from an October estimate of 27%.

To be sure, prolonged, diesel shortages throughout the US are improbable since the country is a net exporter of the fuel. But localized outages and price spikes are likely to become more frequent, especially on the East Coast, where a dearth of pipelines creates huge bottlenecks. The region is heavily reliant on the Colonial pipeline that’s often full. A century-old shipping law, known as the Jones Act, further complicates the movement of domestic fuel and encourages producers on the Gulf Coast to favor exports over supplying the domestic market.

‘Big Dent’

From early February, EU sanctions will ban Russian seaborne deliveries. Those Russian barrels must somehow be replaced if the region’s economy is to keep running as it is today. How and whether that will happen is, so far, unclear.

Winter cold will also exacerbate problems in Europe. Across the northwest, inventories are expected to sink to 211.9 million barrels in March, the month after the EU sanctions kick in, according to consultancy Wood Mackenzie Ltd. That would be lowest level in records going back to 2011.

As the sanctions deadline rapidly approaches, Europe is still importing a huge amount of diesel from Russia. It is also pulling in vast quantities from Saudi Arabia, India and others. As a result, October waterborne imports hit their highest since at least the start of 2016, according to data from Vortexa compiled by Bloomberg.

Germany has already seen tightness, as low Rhine levels hampered deliveries and curbed production, while refineries in neighboring Hungary and Austria have also suffered significant disruption. French output was stifled by a spate of worker strikes over pay.

“If Russia is not a supplier anymore, that puts a big, big dent into the system, which is going to be really difficult to fix,” said Scaffardi, the former Saras CEO.

Poorer Countries Suffer

The global fuel squeeze has made it more profitable for exporters like China and India to send cargoes to countries in Europe that can pay big premiums. Overall fuel exports from China are expected to rise by 500,000 barrels a day to near 1.2 million barrels by year-end, according to industry consultant FGE.

It remains to be seen whether that will be enough to plug the global supply gap, and meanwhile poorer countries that can’t afford sky-rocketing prices are suffering.

Cash-strapped Sri Lanka is struggling to afford international fuel prices and is unable to secure enough supply, the country’s energy minister has said. Thailand has extended a tax cut on diesel in a bid to shield consumers from rising prices, with the government forecasting that the move will cost about $551 million in lost revenue. Vietnam is looking to enact emergency measures, including using its central bank to open up more loans for domestic fuel producers in order to boost supply.

The diesel crunch has been “damaging to the global economy,” said Amrita Sen, the head of research at Energy Aspects Ltd. “Resolving the diesel tightness ultimately needs new refining capacity.”

©2022 Bloomberg L.P.