There is a pretty significant difference in the way different investors perceive a stock in a long-term upward trend. For growth oriented-investors, the longer the upward trend, the more attractive the stock is, simply because the expectation is that the longer, bullish trend will outlast any near-term, bearish sentiment or momentum the stock may see.

By contrast, for value-oriented investors, a stock in an upward trend – especially a long-term one – is something that should generally be avoided. That is especially true if, like me, they also tend to operate with a bit of a contrarian view of the world.

The challenge for value investors is that sometimes, a stock in a long downward trend has a very good reason for being where it is – sometimes, a cheap stock isn’t really a good bargain, it’s just a cheap stock. Efficient market theory holds that in the broadest sense, the market is very good at pricing a company’s underlying fundamental weakness or strength into a stock’s price. That is often very much the case, which is why it is important to always be careful about considering a stock in a long-term downward trend for any kind of bullish position. It’s why I concentrate not only on a stock’s value proposition, but also make sure to run through a detailed view of the company’s business.

For stocks in long-term upward trends, efficient market theory holds that the most likely reason for the increase is the fundamental strength of the underlying business, which naturally attracts more investors to it. The problem with that notion for value investors is that, more often than not, a stock’s increase in price during a long-term upward trend tends to significantly outpace any increase or growth in the company’s actual business or improvement in the bottom line. If sales and earnings increase 10%, for example, a stock’s comparative increase in price will often be 2.5 to 3 times higher. At some point, the stock is simply too expensive to justify an investment.

The idea that trends tend to follow the direction of their longer trend is a technical idiom that tends to contribute to the “buy the dip” mentality that often comes to play when a stock starts to drop off of a recent high point. The dip comes when growth investors start taking profits; the increase in selling activity puts downward pressure on the price until investors decide the stock is at a good price again, and then start buying the stock again. For a value investor, those dips become more interesting the further away from the last high the stock falls, because it increases the chances the stock’s useful value price will fall into line with its current price.

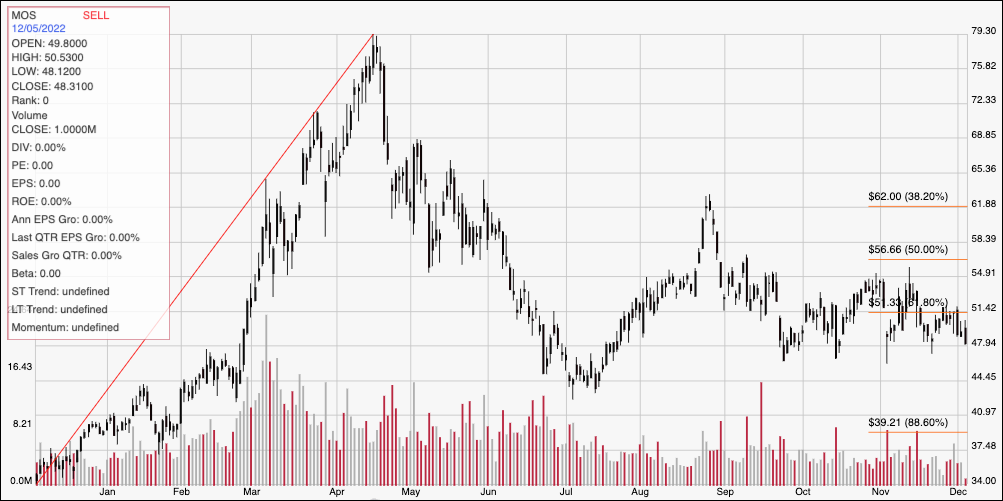

The Mosaic Company (MOS) is a company in the Materials sector I’ve followed for some time that followed the broad market in 2021 and the first quarter of 2022, with an upward trend that saw the stock more than double in value. From its peak at around $79 in April, however, the stock has since dropped into a clear downward trend that has settled into a consolidation range for most of the last two and a half months. A long downward trend can signal potential problems, but it can also often simply reflect the same investor tendency to overreact to news and events – which is why drops like this also tend to pique the interest of bargain hunters like myself. What do the company’s fundamentals say about how much the stock should be worth? Let’s find out.

Fundamental and Value Profile

The Mosaic Company is a producer and marketer of concentrated phosphate and potash crop nutrients. The Company operates through three segments: Phosphates, Potash and International Distribution. The Company is a supplier of phosphate- and potash-based crop nutrients and animal feed ingredients. The Phosphates segment owns and operates mines and production facilities in Florida, which produce concentrated phosphate crop nutrients and phosphate-based animal feed ingredients, and processing plants in Louisiana, which produce concentrated phosphate crop nutrients. The Potash segment mines and processes potash in Canada and the United States, and sells potash in North America and internationally. The International Distribution segment markets phosphate-, potash- and nitrogen-based crop nutrients and animal feed ingredients, and provides other ancillary services to wholesalers, cooperatives, independent retailers and farmers in South America and the Asia-Pacific regions. MOS has a current market cap of about $16.4 billion.

Earnings and Sales Growth: Over the last twelve months, earnings increased 138.5% (not a typo), while revenues improved by 54.45%. In the last quarter, earnings decreased by about -11.5%, while revenue growth was flat, but slightly negative, at -0.46%. The company’s margin profile has been healthy over the past year, but has shown the impact of rising costs over the last quarter; over the last twelve months, Net Income was 20.15% of Revenues, and declined to 15.74% in the last quarter.

Free Cash Flow: MOS’s free cash flow over the last twelve months is $2.17 billion. That’s a significant improvement over the last two quarters; this number was $1.1 billion six months ago and $1.7 billion in the quarter prior. The current number also translates to a healthy Free Cash Flow Yield of 12.92%.

Debt to Equity: MOS has a debt/equity ratio of .28. This is a conservative number. MOS currently has $702.8 million in cash and liquid assets against about $3.3 billion in long-term debt. The company’s balance sheet, along with their increasing cash flow and still-healthy margin profile all indicate that the company has no problem servicing the debt they have.

Dividend: MOS’s annual divided is minimal, at $.60 per share; that translates to a yield of 1.22% at the stock’s current price. It is worth noting that the dividend increased from $.30 per share, per annum at the end of 2021 to $.44 per share, and then to its current level earlier this year. An increasing dividend is a strong sign of fundamental strength.

Price/Book Ratio: there are a lot of ways to measure how much a stock should be worth; but I like to work with a combination of Price/Book and Price/Cash Flow analysis. Together, these measurements provide a long-term, fair value target around $56.50 per share. That means that MOS is nicely undervalued, with about 17% upside from its current price. It’s also worth nothing that earlier this year, this same analysis yielded a fair value target price of $47 per share.

Technical Profile

Here’s a look at the stock’s latest technical chart.

Current Price Action/Trends and Pivots: The red line on the chart above outlines the stock’s upward trend from December of last year to its peak in mid-April at around $79; it also informs the Fibonacci retracement levels on the right side of the chart. After dropping to a low at around $44.50 in July, the stock staged a temporary rally to about $62 before dropping back into a consolidation range that has held current support at around $48, and immediate resistance now at around $51.50 per share, which is where the 61.8% retracement line sits. A push above $51.50 should have near-term upside to about $55 to $56, a little below the 50% retracement line, while a drop below $48 should find next support at around $44.50.

Near-term Keys: MOS’ consolidation range sets up some interesting signals for short-term, directional trading strategies. A push above $51.50, for example, would be an interesting signal to think about buying the stock or working with call options, with $55 providing a useful profit target on a bullish trade, while a drop below $48 would act as a useful bearish signal to consider shorting the stock or buying put options. That range is also offering an interesting opportunity, along with the company’s underlying fundamental strength and value proposition, to think seriously about using MOS as a useful, long-term, value-oriented opportunity right now.