As a conservative-minded, value and fundamental-driven investor, my natural tendency is to shy away from stocks that market experts and popular market media analysts tend to talk to the most about.

Another way to describe this mindset uses the word “contrarian,” and it’s a mindset that I think has even more importance the longer market uncertainty lasts.

Being a contrarian with a purposely conservative approach means that my investments rarely look very sexy – but I’m far more interested in being able to keep my money working for me in any market condition than I am in “chasing the herd.” That’s one of the biggest reasons that throughout the course of the last few years I’ve found the Consumer Staples sector, and specifically the Food Products industry a good place to find useful investing opportunities.

Consumer Staples are products and goods that you and I need everyday – food, household goods, and the things that we aren’t going to stop buying even when economic conditions prompt us to reign in personal spending budgets and tighten our belts. In 2018 and 2019, international trade concerns increased uncertainty in the marketplace, which made this industry a smart place to incorporate into a diversified investment portfolio. 2020 reaffirmed the industry’s usefulness as the pandemic prompted a massive, albeit unexpected consumer shift back towards value-based packaged foods. 2022 has added new elements of uncertainty with high geopolitical uncertainty between Russia and the rest of the West that stands behind Ukraine, inflation and rising interest rates, to highlight the biggest themes that have driven economic and market momentum this year. Those are having a direct impact on Food Products, where prices have been rising at grocery stores across the country, putting an even heavier emphasis on value when it comes to stocking your pantry.

Economic and industry analysts all predicted that the consumer trends I just described would show “stickiness” in 2021, but begin to fade into 2022 and 2023. While a number of companies in this industry can continue to boast healthy balance sheets, the fact is the rising input costs as a result of supply pressures and rising interest are also having an effect, raising consumer prices across the board to levels not seen in roughly thirty years. That means that Consumer Staples stocks could still offer good value while continuing to be resilient the longer inflation remains high. I think there is an important caveat to keep in mind, which is that it is also increasingly important to be very selective, and conservative about when you take a position as well as which stocks represent the best targets of opportunity.

It’s pretty easy to gravitate to well-known, established names like GIS, CPB, and KR, to name just a few, but just because a company has a great name and brand, it doesn’t mean the stock is a good opportunity right now. It is still important to pay attention to a company’s underlying business – in fact, I would argue that it may be more important than ever, because this year’s overall bearish condition means that there a lot Food Products stocks that reflect very attractive valuation levels – but not all of them pass muster when you drill down into the details.

Kraft-Heinz Co. (KHC) is an example of what I mean. Look in your pantry or fridge, and you’ll probably find a lot of this company’s products on your shelves. In terms of recognizability, there aren’t too many food brands that can claim the brand recognition this company has. Heinz condiments including ketchup, mustard, and mayonnaise have been a mainstay of my fridge for years, and Kraft brands like Oscar Meyer are regulars as well. Despite that easy, name-brand recognition, one of the big struggles a lot of traditional names in the Food Products business have been fighting is the trend away from pre-packaged products and into healthier, organic options. While some, like CPB and GIS, seem to finding ways to stay relevant, KHC has struggled. They’re in the midst of a multiyear, long-term transformation strategy, and the pandemic prompted a stock-your-pantry mindset that gave a lot of companies in this industry, including KHC an opportunity to recapture lost customers and gain new ones. The question that remains, however is whether those positives have translated as expected to the company’s bottom line, and what has been the impact so far of broad, rising input costs that are in part attributable to increasing interest rates? Let’s dive in to the numbers so you can decide if this is a company that is worth putting to work for you.

Fundamental and Value Profile

The Kraft Heinz Company is a food and beverage company. The Company is engaged in the manufacturing and marketing of food and beverage products, including condiments and sauces, cheese and dairy, meals, meats, refreshment beverages, coffee and other grocery products. The Company’s segments include the United States, Canada and Europe. The Company’s remaining businesses are combined as Rest of World. The Rest of World consists of Latin America and Asia, Middle East and Africa (AMEA). The Company provides products for various occasions whether at home, in restaurants or on the go. The Company’s brands include Heinz, Kraft, Oscar Mayer, Philadelphia, Planters, Velveeta, Lunchables, Maxwell House, Capri Sun, and Ore-Ida. The Company’s products are sold through its own sales organizations and through independent brokers, agents and distributors to chain, wholesale, cooperative and independent grocery accounts, convenience stores, drug stores, value stores, bakeries and pharmacies. KHC’s market cap is about $51.9 billion.

Earnings and Sales Growth: Over the last twelve months, earnings declined by -3.1%, while sales increased by a little under 3%. In the last quarter, earnings were -10% lower while sales growth was flat, but negative at -0.75%. KHC’s margin profile is improving, which is an interesting contrast to their earnings picture. Net Income as a percentage of Revenues was 4.71% over the last twelve months, and increased in the last quarter to 6.64%.

Free Cash Flow: KHC’s free cash flow was more than $3.5 billion (a sizable improvement from $560 million in mid-2019) over the past twelve months and translates to a Free Cash Flow Yield of 6.83%. It is worth noting that this number declined from almost $6.2 billion in the last quarter of 2020, $3.2 billion in the quarter prior, and $4.45 billion a year ago. That more recent, downward sloping trend in Free Cash Flow, is a confirmation of the weakness being shown by the company earnings pattern.

Dividend Yield: KHC’s dividend is $1.60 per share, and translate to a yield of 3.77% at its current price.

Debt to Equity: KHC has a debt/equity ratio of .40. This is a low number that I think is a bit misleading given a high proportional level of debt versus cash and liquid assets. Their balance sheet shows about $997 billion in cash and liquid assets (down from $3.4 billion a year ago, and $1.5 billion in the quarter prior) against about $19.3 billion in long-term debt. While debt is below the $31 billion mark it saw in mid-2020, cash has also declined from about $5.4 billion at the beginning of 2020.

Price/Book Ratio: there are a lot of ways to measure how much a stock should be worth; but I like to work with a combination of Price/Book and Price/Cash Flow analysis. Together, these measurements provide a long-term, fair value target at around $43.50 per share. That means the stock is pretty fairly valued, with about 2.7% upside from the stock’s current price, and a practical discount price at around $35 per share.

Technical Profile

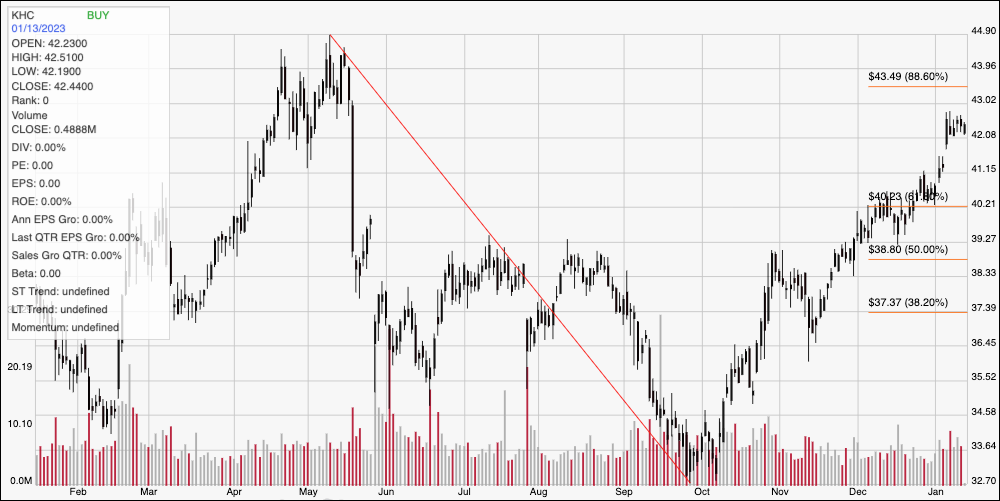

Here’s a look at the stock’s latest technical chart.

Current Price Action/Trends and Pivots: This chart displays the stock’s movement over the last year. The diagonal red line traces the stock’s downward trend from a May high at around $45 to its low, reached in late September at about $33 per share. It also provides the baseline for the Fibonacci retracement lines shown on the right side of the chart. The stock has rallied strongly off of that low, pushing above all of its major retracement lines and peaking in the last week at around $42.50 to mark immediate resistance at that level. Current support is at around $42, where the stock has been hovering this week. A push above $42.50 should have room to retest the stock’s yearly high at around $45, while a drop below $42 should have limited downside, with next support waiting somewhere between $41 (inline with the 61.8% retracement line) and $42.

Near-term Keys: KHC’s rally since October is impressive, and the company has some interesting fundamental strengths working for it, including improving profit margins and an attractive dividend. Unfortunately, the stock can’t be called a good value right now, and there are still enough concerns in the form of declining liquidity and free cash flow that I think make it hard to take this stock seriously as a long-term opportunity. If you prefer to focus on short-term trading strategies, the best probabilities lie on the bullish side; take a push above $42.50 as an opportunity to buy the stock or to work with call options, using the stock’s 52-week high at around $45 as a good exit price.