2023 is off to a positive start; the S&P 500 is up about 4% so far, which has so far been enough to get people talking about a recovery from last year’s bear market.

That broad, bullish momentum means that a lot of stocks have been rallying off of their own lows as well. If you’re looking for signals to start buying, that means that you’re starting to see more signals emerge right now, which makes for tempting reasons to go “all in” and start picking things up as quickly as you can. I think one of the things this latest rally may be dismissing is the reality that most of the risk factors that kept the market near their bear market lows through the last quarter of 2022 – high inflation, geopolitical uncertainty, rising interest rates – are still in place. To me, that means that seeing an increasing number of bullish signals is nice, but should be counterbalanced with a healthy dose of cautious, conservative optimism that reinforces the need to be selective about taking new positions and deliberate about the risk you take when you do decide the time is right to buy.

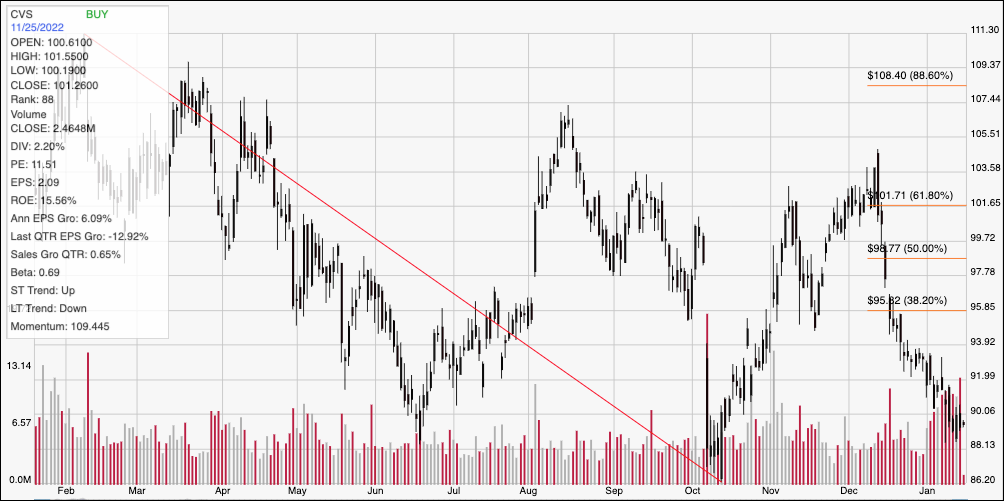

If you’ve been following me in this space at all, or participating in my weekly options trading webinar, you already know that CVS Health (CVS) is a good, old friend that I’ve followed for quite some time. The stock was a star performer in 2021 and the early part of 2022, rising from about $68 at the beginning of March 2021 to a peak in early February 2022 at around $111. From that high, the stock followed broad market momentum lower and into a clear downward trend before finding a low point last October at around $86. It staged a strong enough bullish rally to mark a new short-term upward trend that peaked in the middle of December at around $104 before picking up bearish momentum that now has the stock below $90, with plenty of questions about where the next bottom will be seen.

I think one of the elements longer-term investors should think about in CVS’ market space is the role that CVS and other pharmacy companies play in any economic environment. For the largest players in the U.S. like CVS and Walgreen’s Boots Alliance (WBA), it isn’t just about their ability to fill prescriptions – although that is a core business that is resistant to economic downturns. These are also companies that have spent the last few years actively identifying and investing in ways to evolve and innovate to stay competitive by expanding the scope of their retail locations to do more than just dispense prescriptions and sell consumer goods. Their capital investments include remodeling retail locations to provide expanded health care services and solutions. CVS, in particular was already gaining traction in leveraging its acquisition of insurer Aetna in 2018 to spur its broad transformation from just a drugstore/specialty retailer to a health care company providing a variety of services locally and affordably. Late last year, they doubled down on their commitment to providing primary care solutions by completing an $8 billion acquisition of Signify Health, a tech company that sends care providers directly to patient homes. As a result, I find it hard not to take CVS seriously. I believe the company is uniquely positioned for the current environment, not only in the pharmacy space but also with what I think is a big competitive advantage over the rest of its industry from its Aetna merger. Could the stock also offer a good value at its current price? Let’s dig in to find out.

Fundamental and Value Profile

CVS Health Corporation, together with its subsidiaries, is a health services company. The Company operates through four segments: Pharmacy Services, Retail/LTC, Health Care Benefits and Corporate/Other. The Pharmacy Services segment provides a range of pharmacy benefit management (PBM) solutions, including plan design offerings and administration, retail pharmacy network management services, mail order pharmacy, specialty pharmacy, clinical services, disease management services and medical spend management. The Retail/LTC segment sells prescription drugs and a range of health and wellness products and general merchandise. Its Health Care Benefits segment offers a range of traditional, voluntary and consumer-directed health insurance products and related services. It has approximately 9,900 retail locations, over 1,100 walk-in medical clinics, a pharmacy benefits manager with approximately 105 million plan members, specialty pharmacy services and a senior pharmacy care business. CVS has a market cap of $11.7 billion.

Earnings and Sales Growth: Over the last twelve months, earnings grew by a little over 6%, while Revenues rose by almost 10%. In the last quarter, earnings shrank by -13% while sales were flat, but positive, by 0.65%. The company’s margin profile is historically very narrow, and currently reflects the reality of rising costs as well as the company’s intensive investments in expanding into primary care; over the last twelve months Net Income was 1% of Revenues, and declined sharply to -4.21% in the last quarter. I think it is also worth noting that their trailing twelve-month Net Income number was around $8 billion two quarters ago, and plunged to $3.1 billion in the last quarter, while the quarterly Net Income dipped to -$3.4 billion. I take these as red flags that should be considered very carefully.

Free Cash Flow: CVS’s free cash flow is very healthy, at nearly $19.5 billion. That marks an improvement from $15.8 billion in the quarter prior. The current number translates to an attractive Free Cash Flow Yield of about 16.6%.

Debt to Equity: CVS has a debt/equity ratio of .72. That is a generally conservative number that has dropped steadily from 1 at the beginning of 2021 as management has successfully managed to pay down a significant portion of the debt incurred to complete its merger with Aetna. In the last quarter, cash and liquid assets were about $20 billion versus $50.8 billion in long-term debt. The fact that long-term debt has dropped from about $65 billion since the beginning of 2020 is a good reflection of the company’s success so far in transitioning these disparate organizations into a larger, productive company.

Dividend: CVS pays an annual dividend of $2.42 per share, and which translates to an annual yield of about 2.71% at the stock’s current price. It is also noteworthy that, while dividend increases had been suspended to give the company flexibility to reduce debt gradually from the Aetna merger beginning in 2020, management maintained the dividend throughout 2020 and 2021. They also announced the first increase, along with the implementation of a new stock buyback program at the beginning of 2022, and increased the dividend again after the last earnings announcement from $2.20 per share. An increasing dividend is a strong confirmation of management’s confidence.

Value Proposition: there are a lot of ways to measure how much a stock should be worth; but I like to work with a combination of Price/Book and Price/Cash Flow analysis. Together, these measurements provide a long-term, fair value target at about $103 per share. That suggests the stock is undervalued, with about 15% upside from its current price. It’s also worth noting that before the end of 2022, this same analysis yielded a fair value target price at around $123.50 per share.

Technical Profile

Here’s a look at CVS’ latest technical chart.

Current Price Action/Trends and Pivots: The diagonal red line marks the stock’s downward trend from a January peak at around $111 to its low in October at around $86. It also provides the baseline for the Fibonacci retracement lines shown on the right side of the chart. After rallying to about $105 in December, the stock has picked up new, strong bearish momentum, most recently falling below expected support at around $90 to mark immediate resistance there. Current support is around $89, where the stock has hovered for most of this week. A drop below $89 should retest the stock’s 52-week low at around $86, while a push above $90 should find next resistance at around $92 per share.

Near-term Keys: If you prefer to work with short-term trading strategies, a break above resistance at $90 could offer an attractive signal to buy the stock or work with call options with an eye on $92 as a useful exit point. A bearish signal would come from a drop below $89, with $86 providing a quick exit target no matter whether you choose to short the stock or buy put options. From the standpoint of value and long-term opportunity, the stock offers a useful opportunity to consider the stock as a long-term, value-driven investment, however I think that the latest downturn in Net Income, along with the stock’s current bearish momentum make waiting for signs of improvement in Net Income, along with a stabilization of the stock’s current price drop before taking on a new position.