More than two decades of experience as a student of the markets have taught me that while the market is generally resilient, there is one word that always seems to automatically put the market on edge: change.

The COVID-19 pandemic was the start of the most recent example. After a decade of practically uninterrupted growth, the global spread of coronavirus put the entire world into lockdown mode, shuttering economic activity and plunging the stock market into one of the most immediate turns to bear market conditions in history. From a March 2020 low, the market also rebounded quickly as economic activity gradually resumed, and by the end of 2021 most economic experts were wondering how long the latest bullish rally would continue.

2022 shifted the narrative yet again. Extended supply chain issues, combined with increasing consumer demand, and with the Russia-Ukraine war thrown in for extra combustible fuel forced the Fed to begin raising interest rates on an increasingly aggressive basis that isn’t expected to moderate until later this year. If the market abhors change, it fears increasing interest rates, which explains the market’s plunge to bear market conditions in 2022 and the continuing uncertainty that persists right now.

The reality of inflation is that it is an ever-present dynamic with which any and all economies have to contend. The real concern for any market-based economy is inescapably tied to the ebb and flow of inflationary pressures. Lack of inflation implies that costs are being driven down, which sounds good at first blush, but which in an extended, extreme state points to declines in demand that usually signal bigger problems at the extremes. Flip the coin, and increasing inflation does suggest that costs are increasing, but is generally a positive when it is attributed to the rising demand from businesses and consumers that we all generally take as indicative of a healthy, growing economy. The concern is that when inflation has been extended to extreme highs, there are larger issues that prevent suppliers from effectively meeting demand.

One of the areas that has been seeing a strong reaction to these indications of cost inflation is in the Food Products industry – an industry that I usually like to think of as a good way to position a portfolio with conservative, even defensive options to help moderate risk. One specific area that seems to be showing unexpected inflationary conditions is in the cost of goods companies in this industry have been seeing for most of the last two years, with no near-term relief in sight. Conagra Brands, Inc. (CAG) is an example. Management has cited cost increases to explain pressures on its business that have hampered liquidity and increased long-term debt, and which they also used at the beginning of 2022 to taper their own estimates for the company’s financial performance. Despite that grim forecast, the stock followed an upward trend for most of 2022 that peaked at the start of this month at around $41. From that peak, the stock has dropped quickly to its current price at around $37 per share. What is the story that the company’s fundamentals tell now? Are they strong enough to suggest the drop could offer a useful opportunity for value seekers? Let’s dive in and find out.

Fundamental and Value Profile

Conagra Brands, Inc., formerly ConAgra Foods, Inc., operates as a packaged food company. The Company operates through two segments: Consumer Foods and Commercial Foods. The Company sells branded and customized food products, as well as commercially branded foods. It also supplies vegetable, spice and grain products to a range of restaurants, foodservice operators and commercial customers. Conagra Foodservice offers products to restaurants, retailers, commercial customers and other foodservice suppliers. The Company also operates in the countries outside the United States, such as Canada and Mexico. The Company’s brands include Marie Callender’s, Healthy Choice, Slim Jim, Hebrew National, Orville Redenbacher’s, Peter Pan, Reddi-wip, PAM, Snack Pack, Banquet, Chef Boyardee, Egg Beaters, Rosarita, Fleischmann’s and Hunt’s. The Company sells its products in grocery, convenience, mass merchandise and club stores. CAG’s current market cap is $17.6 billion.

Earnings and Sales Growth: Over the last twelve months, earnings increased by 26.56%, while Revenues improved by 8.3%. Earnings increased in the last quarter by a little more than 42%, while sales grew by a little more than 14%. The company’s margin profile over the last twelve months is showing signs of improvement and strength after weakness and deterioration for most of 2022. Net Income was 5.66% of Revenues over the past twelve months and increased to 11.53% in the last quarter.

Free Cash Flow: CAG’s free cash flow is $830.4 million over the last twelve months. That marks a decline from $886.4 million in the quarter prior, but is above the $696.2 million mark from a year ago. The current number also translates to a modest Free Cash Flow Yield of about 5.4%. It also acts as an interesting counter to the weakness indicated by the company’s slip into negative Net Income in the last quarter.

Debt to Equity: CAG has a debt/equity ratio of .92. That number has declined from 1.58 at the beginning of 2019, but the actual long-term debt number remains high, a reflection of the reality that the company’s liquidity is a significant question mark. In the last quarter Cash and liquid assets were about $39.7 million – a decline from $67.4 million in the prior quarter and $438.2 million in the last quarter of 2020. The company also reported about $8.1 billion in long-term debt. Most of that debt is attributable to CAG’s acquisition of Pinnacle Foods in the last quarter of 2018, and it is true that the company has paid down more than $3.8 billion of that debt over the course of the last two years, which can at least partly explain the steady decline in cash and liquid assets.

Dividend: CAG pays an annual dividend of $1.32 per share – which the company increased from $.85 in its last earnings call of 2020, $1.10 in 2021, and $1.25 in mid-2022, and which translates to an annual yield of about 3.54% at the stock’s current price. An increasing dividend is a strong sign of management’s confidence in their business model and their operating success in the future.

Price/Book Ratio: there are a lot of ways to measure how much a stock should be worth; but I like to work with a combination of Price/Book and Price/Cash Flow analysis. Together, these measurements provide a long-term, fair value target at about $36 per share. That means the stock is somewhat overvalued at its current price, with -3.22% downside and a practical discount price at around $29. It is also worth noting that at the end of 2021, this same analysis put the stock’s fair value target at around $34.50 per share, $45 during the first half of that year, and $31 in 2022.

Technical Profile

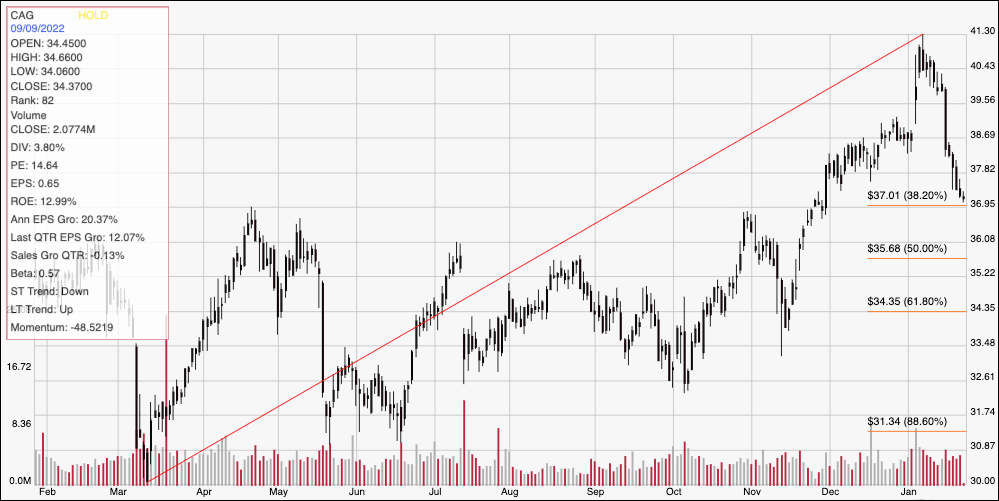

Here’s a look at the stock’s latest technical chart.

Current Price Action/Trends and Pivots: The chart above marks the stock’s price activity over the last year. The red diagonal line marks the stock’s upward trend from its 52-week low at around $30 to to its latest peak at the start of January at around $41.50. It also provides the baseline for the Fibonacci retracement lines shown on the right side of the chart. The stock has dropped sharply from that peak, falling to about $37 right now. It’s momentum is strongly bearish, but it is nearing the 38.2% retracement line, marking expected, current support at that level. If $37 doesn’t hold, it should find next support at around $36. Immediate resistance is around $39, where the stock held a 52-week high level for most of December. A drop below $36 could give the stock room to fall to about $34, where a major pivot low in November 2022 occurred, while a push above $39 should see the stock retest its 52-week high at around $41.50.

Near-term Keys: From a fundamental standpoint, CAG’s profile has lost quite a bit of the luster it showed in 2021, with the last couple of earnings reports doing little to improve the picture. Improving Net Income is useful, but declines in Free Cash Flow and Cash remain big red flags. There is also no practical way right now to suggest the stock offers a useful value to make it an attractive long-term, defensive buying candidate. That means that the best probabilities if you want to work with CAG lie in short-term, momentum-based trading strategies. You could use a push above $39 as a signal to consider buying the stock or working with call options, with an eye on $41.50 as a quick-hit profit target. A drop below $36 could be a useful signal to consider shorting the stock or buying put options, with $34 providing a practical, quick-hit bearish profit target.