The word, “uncertainty” has characterized the market for most of the past year, as questions about inflation, interest rates, and the risk of recession have been top of mind for most investors.

Extended periods of uncertainty make it harder for investors to decide to keep their money working for them. Inflation continues to remain high, despite repeated interest rate increases from the Fed, including this week’s most recent increase. Optimists are already pointing to the fact that increase was lower than previous hikes as an indication of the increasing possibility that rates might not only stop increasing this year, but that the Fed could actually start cutting by the end of the year. Given the continued high levels of consumer prices and historically low unemployment, not to mention the fact that inflation is still above 6%, however, I’m inclined to believe Fed chair Jerome Powell’s choice of words in announcing the latest increase, which signaled multiple rate hikes are still in store this year. I think that puts a cap on how much upside the market may be able to see this year, with the continued risk of a recession resulting from restrictive monetary policy still very much a possibility.

While a recession, and the extension of last year’s bear market is a scary thing in and of itself, it also opens the possibility of new buying opportunities in good stocks at much better prices than than they have been in quite some time. The market is an emotional animal, and that is one of the reasons that the mantra “all trends are finite” tend to hold true. That’s also true of downward trends; while bear markets can extend into two or possibly even three-year time periods, they inevitably find their own end. Value-oriented, patient investors who can recognize stocks that offer big discounts along with solid fundamentals during these extended downturns are in a better position than the momentum hunters, that are usually trying to figure out where the bottom of the market might be.

Just as most investors fail to recognize increasing risk at the top of a long bull market and period of economic expansion, they also tend to let their fear drive them away from the markets nearer to the end of a bear market than the beginning. That’s why it takes a bit of a contrarian perspective of things to wrap your mind around the reality that all trends – bullish and bearish – have an end, and that opportunity lies at both extremes. The simple fact is that smart investors can usually find terrific opportunities even when the market is uncertain and sitting near extended bear market lows. Sometimes, you can even find pockets of the economy that are diverging from those scary downward patterns.

The wireless telecommunications industry is an interesting case in point. Shelter-in-place orders, work-at-home arrangements, and the continued need to maintain social distancing measures during 2020 and 2021 have increased just about everybody’s reliance on their mobile devices, which is generally good news for the companies that provide those products and the services that come with them. The economic pressures associated with high interest rates and rising consumer costs, however also means that demand for new devices, including upgraded smartphones, tablets, wearables, and so on, has been a bit muted of late, and could continue. That is likely to keep pressure on those companies to manage their operations as efficiently as possible. That could be a challenge, as leverage in this industry was already very high before the pandemic hit, even among the largest and most established companies, like AT&T and Verizon Communications Inc. (VZ).

That’s the bad news – but I also think that there is quite a bit of good news to consider, as well. Over the last few years, VZ has been one of the biggest investors in acquiring 5G spectrum (bandwidth), and are the first major provider to start rolling out 5G connectivity in their network. This is an area that VZ continues to invest in heavily, and as one of two dominant players in the telecomm industry and in building out the infrastructure for 5G service, it should be expected that in the long run, this is why 5G still represents a long-term growth opportunity. Sooner or later, consumer trends will shift back in favor of the tools that enable faster wireless connectivity, and that means that companies that have been at the front of the pack on the capital investment, development and implementation side will still be the winners in this game.

VZ’s stock price has followed a downward trend, especially over the last year, but also runs counter to an overall strong fundamental profile that includes a bargain proposition that puts its target price about 30% above its current price. VZ has borrowed heavily to finance its capital investments, including its 5G buildout, but that is also countered by healthy free cash flow and operating margins that have held up better than expected in the current economic environment, along with a higher-than-average dividend. Does the combination make VZ a stock worth paying attention to? Let’s find out.

Fundamental and Value Profile

Verizon Communications Inc. is a holding company. The Company, through its subsidiaries, provides communications, information and entertainment products and services to consumers, businesses and governmental agencies. Its reportable segments are Verizon Consumer Group and Verizon Business Group. Its Consumer segment provides wireless and wireline communications services. Its wireless services are provided across wireless networks in the United States under the Verizon Wireless brand. Its wireline services are provided in nine states in the Mid-Atlantic and Northeastern United States, over its 100% fiber-optic network under the Fios brand and via traditional copper-based network. Its Business segment provides wireless and wireline communications services and products, video and data services, corporate networking solutions, security and managed network services, local and long-distance voice services and network access to deliver various Internet of Things (IoT) services and products. VZ has a current market cap of about $175.6 billion.

Earnings and Sales Growth: Over the last twelve months, earnings shrank by -9.16%, while revenues increased by about 3.5%. In the last quarter, earnings growth fell -9.85, while revenues where 2.95% higher. VZ operates with a healthy operating profile. Over the last twelve months, Net Income was 15.53% of Revenues, and increased to 18.66% in the last quarter.

Free Cash Flow: VZ’s free cash flow is healthy, at more than $14 billion, and translates to a useful Free Cash Flow Yield of about 8%. Compared to the last year, Free Cash Flow is lower, from around $15 billion, as well as from the quarter prior, at $14.3 billion.

Dividend: VZ’s annual divided is $2.61 per share (increased from $2.46 in the middle of 2020, $2.51 in 2021, and $2.56 late last year), and which translates to an impressive yield of 6.26% at the stock’s current price. An interesting note I picked up from an economic report not long ago recognized the general fundamental strength of the Telecom Services sector, T and VZ in particular, with dividend payout levels well above bond yields, and limited currency or global macroeconomic risks. That supports the notion that, to a point, this sector could be viewed as an “equity bond” for investors looking for productive, passive income.

Debt/Equity: VZ carries a Debt/Equity ratio of 1.52, which is generally considered a high number that isn’t unusual for stocks in this industry. Their balance sheet shows about $2.6 billion in cash and liquid assets versus about $140.6 billion in long-term debt. It should be noted that in the quarter prior, cash and liquid assets were about $2.1 billion, marking a useful increase. Their operating profile indicates that servicing their debt, even though it is high, shouldn’t be a problem.

Price/Book Ratio: there are a lot of ways to measure how much a stock should be worth; but I like to work with a combination of Price/Book and Price/Cash Flow analysis. Together, these measurements provide a long-term, fair value target around $54 per share, which suggests that the stock is significantly undervalued right now, with about 30% upside from its current price.

Technical Profile

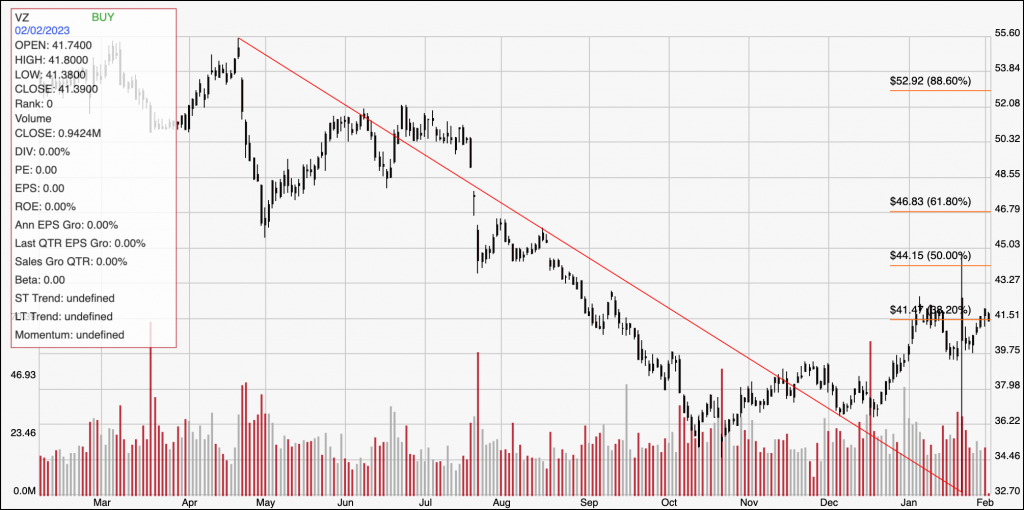

Here’s a look at the stock’s latest technical chart.

Current Price Action/Trends and Pivots: The red diagonal line measures the length of the stock’s downward trend from high at around $55.50 in April to its low at around $33, reached earlier this month; it also informs the Fibonacci retracement lines shown on the right side of the chart. For most of the past month, the stock has been holding in a narrow range between immediate resistance at around $42, where the 38.2% retracement line sits, and current support at about $40. A drop below $40 should find next support at around $38, while a push above $42 could see bullish momentum to about $45 before finding next resistance.

Near-term Keys: VZ offers a very useful value proposition, with a higher-than-average dividend that should make for tempting bait for both value and fundamental-oriented investors. The stock’s fundamentals support that idea, which is why I think VZ is a stock that is worth taking very seriously at its current price as a long-term opportunity. If you prefer to focus on short-term trades, you could use a push above $42 as a signal to buy the stock or work with call options, with an eye on $45 as a practical, short-term, bullish profit target. A drop below $40 should be taken as a signal to consider shorting the stock or buying put options, with $38 providing a useful profit target on a bearish trade.